Mish's Global Economic Trend Analysis |

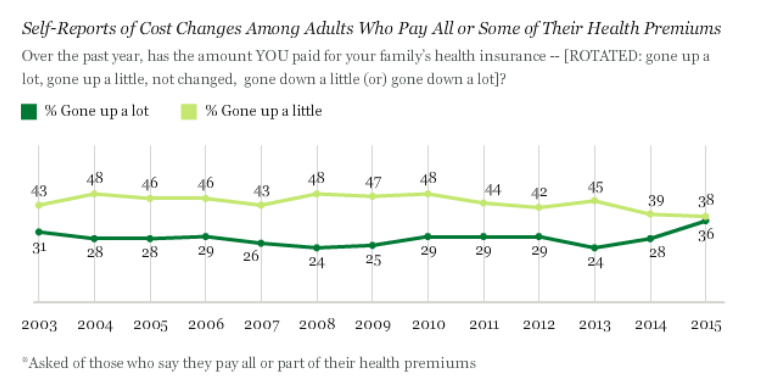

- Obamacare in Action: 74% Say Insurance Costs Went Up, Record 36% Say "By a Lot"; Plan for Still More Hikes

- Trade Deficit Widens as US Exports Dip

- New Home Sales vs. Labor Force and Civilian Population; Factors Behind Decreasing Sales

- Second Strong Payroll Number +211,000; December Rate Hike Assured

| Posted: 04 Dec 2015 12:37 PM PST Obamacare was supposed to lower costs by pooling everyone together, by creating other efficiencies, and by admittedly overcharging millennials for healthcare. Actual results continue to pour in, nearly all of them negative. Today Gallup reports More Americans Say Health Premiums Went Up Over Past Year. Nearly three in four American adults (74%) who pay all or some of their health insurance premiums say the amount they pay has gone up over the past year. This percentage is up marginally from the 67% who last year said their costs increased, but it is generally in line with what Gallup has found in yearly updates since 2003.Mike "Mish" Shedlock |

| Trade Deficit Widens as US Exports Dip Posted: 04 Dec 2015 09:50 AM PST Exports and imports are both down again this month. Exports decreased more so the result is a widening of the trade deficit. The Bloomberg Econoday Consensus was for a balance of -40.6 billion. The actual number was -43.9 billion, at the top end of the range of expectations. The nation's trade deficit came in at the high end of expectations in October, at $43.9 billion with details reflecting oil-price effects but also soft foreign demand. Exports fell 1.4 percent in the month while imports, pulled down by oil, fell 0.6 percent. The decline for goods exports, at 2.5 percent, is in line with last week's advance data but not for imports where goods declined 0.6 percent, vs the advance reading of minus 2.1 percent. Exports of services are once again solid at plus 0.7 percent.Not Mixed Given that imports subtract from GDP, the report is not "mixed". Nor does a chart of imports and exports appear to be "mixed". Nor can anyone look at the following and see "signs of life".  Commerce Details Let's dive into the Commerce Release on U.S. International Trade for October 2015 for additional details. The U.S. Census Bureau and the U.S. Bureau of Economic Analysis, through the Department of Commerce, announced today that the goods and services deficit was $ 43.9 billion in October, up $ 1.4 billion from $ 42.5 billion in September, revised. October exports were $184.1 billion, $ 2.7 billion less than September exports. October imports were $ 228.0 billion, $1.3 billion less than September imports.International Trade Balance October 2013 - October 2015  International Trade Balance Moving Average  Signs of life in a "mixed" report are imaginary. Mike "Mish" Shedlock |

| New Home Sales vs. Labor Force and Civilian Population; Factors Behind Decreasing Sales Posted: 04 Dec 2015 07:56 AM PST Reader Tim Wallace pinged me with a couple interesting charts on new home sales. The charts compare new home sales to the labor force and also to the civilian non-institutional population. The numbers compare November 2015 to November in prior years. The numbers are not seasonally adjusted. New home sales are at an annualized rate. New Home Sales vs. Labor Force and Civilian Non-Institutional Population  For the above chart the labor force and population are in 1000's but new home sales are in 10's. Sales peaked in 2005. New Home Sales as Percentage of Labor Force and Civilian Non-Institutional Population  For the above chart all numbers have the same scale so the percentages are accurate. Labor Force Comparison

Population Comparison

These dramatically lower percentages are a function of numerous variables. Factors Behind Decreasing Sales

Mike "Mish" Shedlock |

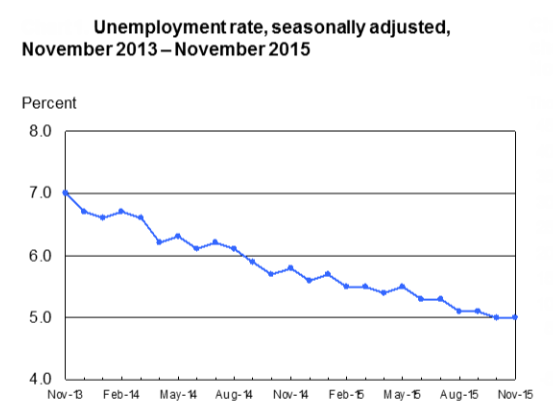

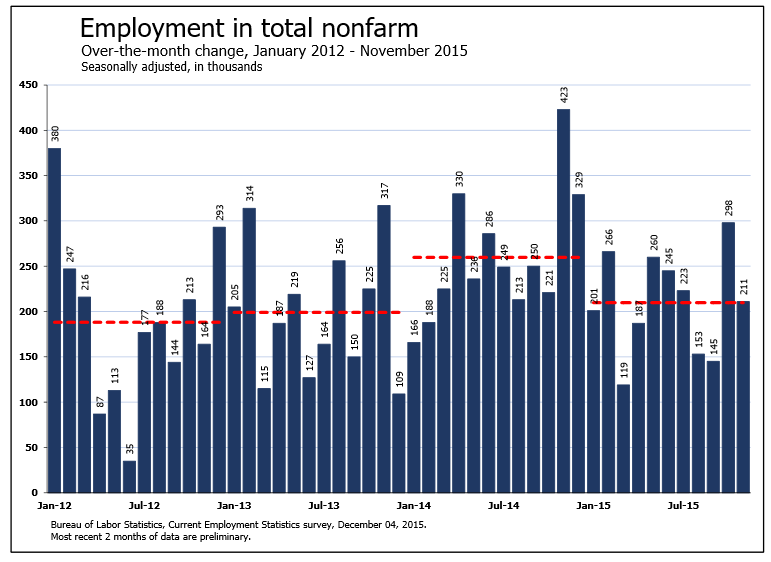

| Second Strong Payroll Number +211,000; December Rate Hike Assured Posted: 04 Dec 2015 07:42 AM PST Initial Reaction Following last month's payroll surge comes a second strong month. The Bloomberg Consensus estimate was 190,000 jobs and the headline total was 211,000. The unemployment rate was steady to 5.0%, the lowest since April 2008. A rate hike in December is now assured. BLS Jobs Statistics at a Glance

Employment Report Please consider the Bureau of Labor Statistics (BLS) Current Employment Report. Total nonfarm payroll employment increased by 211,000 in November, and the unemployment rate was unchanged at 5.0 percent, the U.S. Bureau of Labor Statistics reported today. Job gains occurred in construction, professional and technical services, and health care. Mining and information lost jobs. Unemployment Rate - Seasonally Adjusted  Nonfarm Employment  Click on Any Chart in this Report to See a Sharper Image Nonfarm Employment Change from Previous Month by Job Type  Hours and Wages Average weekly hours of all private employees was down 0.1 hours to at 34.5 hours. Average weekly hours of all private service-providing employees was unchanged at 33.4 hours. Average hourly earnings of private workers rose $0.01 to $21.19. Average hourly earnings of private service-providing employees rose $0.01 to $20.99. For discussion of income distribution, please see What's "Really" Behind Gross Inequalities In Income Distribution? Birth Death Model Starting January 2014, I dropped the Birth/Death Model charts from this report. For those who follow the numbers, I retain this caution: Do not subtract the reported Birth-Death number from the reported headline number. That approach is statistically invalid. Should anything interesting arise in the Birth/Death numbers, I will add the charts back. Table 15 BLS Alternate Measures of Unemployment  click on chart for sharper image Table A-15 is where one can find a better approximation of what the unemployment rate really is. Notice I said "better" approximation not to be confused with "good" approximation. The official unemployment rate is 5.0%. However, if you start counting all the people who want a job but gave up, all the people with part-time jobs that want a full-time job, all the people who dropped off the unemployment rolls because their unemployment benefits ran out, etc., you get a closer picture of what the unemployment rate is. That number is in the last row labeled U-6. U-6 is much higher at 9.9%. Both numbers would be way higher still, were it not for millions dropping out of the labor force over the past few years. Some of those dropping out of the labor force retired because they wanted to retire. The rest is disability fraud, forced retirement, discouraged workers, and kids moving back home because they cannot find a job. Mike "Mish" Shedlock |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment