| Illegal Public Seizure of Mortgages Via Eminent Domain in the Spotlight Posted: 30 Jul 2013 05:42 PM PDT Bloomberg reports Richmond Escalates Eminent Domain Plan With Loan Offers. Richmond, California, is backing a plan to buy mortgages in low-income areas for as little as 25 cents on the dollar and may force the sales under eminent domain laws, moving forward with a controversial program that would potentially seize control of home loans from investors.

Richmond is the farthest along in a plan advocated by Steven Gluckstern's Mortgage Resolution Partners LLC for U.S. cities to confiscate mortgages and write them down in an effort to help homeowners escape oversized debt burdens. The idea has drawn opposition from bondholders such as Pacific Investment Management Co. and DoubleLine Capital LP and at least 18 trade groups representing the finance industry, homebuilders and real estate firms.

None of the 32 servicer and bond trustees that oversee the loans will likely sell willingly, Chris Killian, head of the securitization group for the Securities Industry and Financial Markets Association, Wall Street's largest lobbying group, said in a phone interview.

"You just can't really sell performing loans out of securitizations," Killian said. "Additionally, everybody we talk to in the industry thinks this is a bad idea that will be bad for the mortgage markets." Eminent Domain Eminent domain (confiscation of private property for the public good), have been upheld time and time again, most recently in the infamous US Supreme Court decision Kelo v. City of New London. Kelo v. City of New London, 545 U.S. 469 (2005) was a case decided by the Supreme Court of the United States involving the use of eminent domain to transfer land from one private owner to another private owner to further economic development. In a 5–4 decision, the Court held that the general benefits a community enjoyed from economic growth qualified private redevelopment plans as a permissible "public use" under the Takings Clause of the Fifth Amendment.

The case arose in the context of condemnation by the city of New London, Connecticut, of privately owned real property, so that it could be used as part of a "comprehensive redevelopment plan." However, the private developer was unable to obtain financing and abandoned the redevelopment project, leaving the land as an empty lot, which was eventually turned into a temporary dump.

Public reaction to the decision was highly unfavorable. Much of the public viewed the outcome as a gross violation of property rights and as a misinterpretation of the Fifth Amendment, the consequence of which would be to benefit large corporations at the expense of individual homeowners and local communities. Some in the legal profession construed the public's outrage as being directed not at the interpretation of legal principles involved in the case, but at the broad moral principles of the general outcome. Federal appeals court judge Richard Posner wrote that the political response to Kelo is "evidence of [the decision's] pragmatic soundness." Judicial action would be unnecessary, Posner suggested, because the political process could take care of the problem."

Prior to Kelo, seven states specifically prohibited the use of eminent domain for economic development except to eliminate blight: Arkansas, Florida, Kansas, Kentucky, Maine, New Hampshire, South Carolina and Washington. As of June 2012, 44 states had enacted some type of reform legislation in response to the Kelo decision. Of those states, 22 enacted laws that severely inhibited the takings allowed by the Kelo decision, while the rest enacted laws that place some limits on the power of municipalities to invoke eminent domain for economic development. The remaining eight states have not passed laws to limit the power of eminent domain for economic development. End Result of Seizure: A Dump There you have it. The result of the seizure (whose intent was a mall), turned useful tax-payer property into a vacant lot, then a dump when the developer could not get financing. 44 states passed laws restricting eminent domain as a response to that poor US supreme court decision. One of those states was California. Proposition 99 California passed Proposition 99 in 2008. Summary Prepared by the Attorney General

- Bars state and local governments from using eminent domain to acquire an owner-occupied residence, as defined, for conveyance to a private person or business entity.

- Creates exceptions for public work or improvement, public health and safety protection, and crime prevention.

Ridiculously Broad Interpretations What constitutes "public work or improvement, public health and safety protection, and crime prevention"? The statement is so broad as to be 100% meaningless. Was that the intent of Prop 99 all along? Non-Fair Value Seizures The law requires the owner to receive "fair value" for the seizure. Of course it is the state that gets to define "fair value". Richmond does not even want to pay fair value for the mortgages. Please consider these additional details in the New York Times article A City Invokes Seizure Laws to Save Homes. On Monday, the city sent a round of letters to the owners and servicers of the loans, offering to buy 626 underwater loans. In some cases, the homeowner is already behind on the payments. Others are considered to be at risk of default, mainly because home values have fallen so much that the homeowner has little incentive to keep paying.

Many cities, particularly those where minority residents were steered into predatory loans, face a situation similar to that in Richmond, which is largely black and Hispanic. About two dozen other local and state governments, including Newark, Seattle and a handful of cities in California, are looking at the eminent domain strategy, according to a count by Robert Hockett, a Cornell University law professor and one of the plan's chief proponents. Irvington, N.J., passed a resolution supporting its use in July. North Las Vegas will consider an eminent domain proposal in August, and El Monte, Calif., is poised to act after hearing out the opposition this week.

The city is offering to buy the loans at what it considers the fair market value. In a hypothetical example, a home mortgaged for $400,000 is now worth $200,000. The city plans to buy the loan for $160,000, or about 80 percent of the value of the home, a discount that factors in the risk of default.

Then, the city would write down the debt to $190,000 and allow the homeowner to refinance at the new amount, probably through a government program. The $30,000 difference goes to the city, the investors who put up the money to buy the loan, closing costs and M.R.P. The homeowner would go from owing twice what the home is worth to having $10,000 in equity.

All of the loans in question are tied up in what are called private label securities, meaning they were bundled and sold to private investors. Such loans are generally the most unfavorable to borrowers and the most likely to default, Mr. Gluckstern said. But they are also the most difficult to modify because they are controlled by loan servicers and trustees for the investors, not the investors themselves. Sappy Details The Times article disclosed the sappy details of a person who paid $420,000 for a home now worth $125,000. To what extent should government intervene in such affairs? The obvious answer is "none". The homeowner can walk away is he wants, and if he doesn't want, then he can keep paying the mortgage. Questionable Details As long as someone is willing to keep paying the mortgage, then the value of the loan is more than the alleged "fair value" offered by the city. And note the $30,000 difference to the city and the new investors in the proposed scheme. In essence, the city wants to confiscate private property not for the "public good" but for the good of its own finances, for the good of new lenders, for the good of one set of private persons, at the expense of another set of private persons, at a very questionable "fair value" price. I contend this is not only morally wrong, but blatantly illegal. Should this socialist wealth redistribution scheme actually be upheld by the courts, it will unleash a torrent of increasingly ridiculous schemes, while further undermining property ownership rights, the very thing governments ought to protect. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

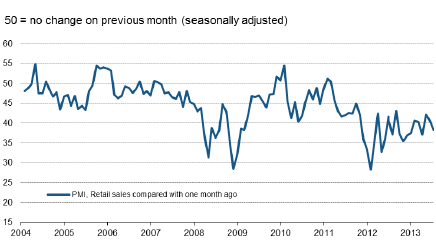

| Retail Sales Rise in Germany and France, Decline in Italy; Margin Squeeze in Germany and France Posted: 30 Jul 2013 09:17 AM PDT It's a mixed bag of retail PMI news in Europe today (assuming of course one believes that spending is good). Italy: Sharpest drop in retail sales since April In Italy, Markit reports Sharpest drop in retail sales since April Key points

- Rate of decline in retail sales accelerates for second straight month

- Stocks levels fall amid sharp drop in retailers' purchasing activity

- Purchase price inflation dips to modest rate

Summary

The downturn in Italy's retail sector gained further momentum in July. The level of trade fell at a faster rate, leading to an accelerated decline in retailers' purchasing activity and contributing to a deterioration in business sentiment. There were also further notable reductions in profitability, employment and inventory levels on the month.

July saw an acceleration in the month-on-month rate of decline in Italian retail sales, as highlighted by a drop in the headline Markit Italy Retail PMI® from 40.7 in June to 38.2. This was its lowest reading since April, and one that was indicative of a sharp pace of contraction overall. The level of trade has fallen continuously on a monthly basis for almost two-and-a-half years.

The gap between actual and planned sales was the widest for four months in July, as almost half of businesses missed their targets. Firms attributed their underperformance to a combination of uncertainty and pessimism among consumers. Germany: strongest sales growth for two-and-a-half years In Germany, Retail PMI indicates strongest sales growth for two-and-a-half years. Key points

- Retail PMI hits highest level since January 2011

- New job creation maintained in July

- Wholesale price inflation eases since June

Summary

The seasonally adjusted Germany Retail PMI – which measures month-on-month sales on a like-for-like basis – registered above the 50.0 nochange mark for the third consecutive month in July. At 56.0, up from 55.3 in June, the latest reading signalled the strongest month-on-month increase in sales since the start of 2011.

Margins decrease again in July

German retailers pointed to a reduction in their gross operating margins for the thirty-second consecutive month, with the rate of decline little changed since June. Survey respondents widely suggested that higher cost burdens had offset the boost to margins from increased sales during July.

Latest data signalled a steep rate of input price inflation, although it was the second-slowest since September 2012. Some retailers commented on higher food costs, especially for fresh fruit and vegetables.

Comments

Commenting on the Markit Germany Retail PMI® survey data, Tim Moore, senior economist at Markit and author of the report said:

"July data shows a continuing improvement in German retail sector performance, as month-on-month sales growth hit a two-and-a-half year high. More favourable weather conditions and signs of rising consumer confidence helped underpin the acceleration in retail sales. Margins nonetheless remain under pressure as retailers indicated that they were forced to absorb sharp increases in their cost burdens during the latest survey period." France: Retail Sales Rise for First Time in 16 Months In France, the Markit PMI shows Retail Sales Rise for First Time in 16 Months Key Points

- Slight expansion of sales recorded in July

- Slowest fall in employment for over a year

- Further reduction in purchasing activity

Summary

French retailers signalled a return to growth in sales during July. Although modest, the month-on-month increase was the first recorded since March 2012. Sales were also marginally higher on an annual basis. Employment continued to fall, but the rate of job shedding eased to a marginal pace. Retailers' margins remained under considerable pressure, despite a weaker rise in purchasing costs.

The headline Retail PMI registered 51.0 in July, up from 48.9 in June and above the 50.0 threshold for the first time in 16 months. Anecdotal evidence suggested that sales growth was supported by improved demand conditions and promotional offers.

When compared with previously set plans, actual like-for-like sales once again fell short in July. However, the degree to which sales disappointed was the least marked since January.

Comment

Jack Kennedy, Senior Economist at Markit and author of the France Retail PMI, said:

"The French retail sector finally snapped out of its extended downturn in July. Although sales were up only slightly, it was the first growth in 16 months, amid reports of firmer demand conditions. However, retailers were again faced with a considerable squeeze on their margins, as they competed to offer discounts in a bid to stimulate sales. Meanwhile, the slowest drop in employment for over a year points to an easing of the gloom that has enveloped the retail sector in recent times." Europe Synopsis - The economic depression lingers in Italy.

- Germany is back in growth mode but with strong inflation and inability of retailers to pass on input cost increases.

- France, is barely back in expansion, but only after strong discount promotions. French retailers also suffer from a margin squeeze. Employment is still shrinking, albeit at a slow pace.

These imbalances highlight the structural problem of one centrally-planned Euro-interest rate across widely varying economic conditions. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |