| Encrypt Everything, Store Nothing, Leave No Trace! (Dissolving Messages, Wickr, Snapchat) Posted: 25 Nov 2013 01:14 PM PST US corporations like Google, Facebook, and Microsoft benefit from "safe harbor" treaties with the US that allow those companies exemption from European privacy rules. Then the NSA and FBI came along and forced those companies to put in "back doors" so that nothing is private. In the latest 100% believable accusation, EU accuses US of improperly trawling citizens' online data. In response, Europe is threatening to end the safe harbor laws. Brussels is to warn Washington that US tech companies risk losing their exemption from privacy rules unless the US changes the way it treats EU citizens' online data.

A European Commission review of the "safe harbour" pact that allows US technology groups such as Google, Facebook and Microsoft to operate in Europe without EU oversight will conclude that Washington has improperly forced US companies to hand over European customers' data. It also says that breaches of the data deal have given US tech companies a competitive advantage over European rivals.

Although the review, which will be unveiled on Wednesday, stops short of calling for the safe harbour agreement to be scrapped, its wording signals that the EU will move in that direction unless the US changes the way that it uses data held by companies on EU citizens.

A scrapping of the safe harbour deal is one of the most formidable weapons the EU has in its arsenal to punish the Obama administration after claims of snooping on Europeans by the National Security Agency.

Such a move would wreak havoc for any US tech company doing business in Europe – especially Google, Facebook and Microsoft, which rely on the agreement to transfer customers' data seamlessly between countries.

Ending safe harbour and subjecting US companies to European privacy laws would put them in a legal bind over NSA requests for information about European citizens. Under US law they would still be forced to hand over the information, provided the request was backed by an order from the secret foreign intelligence surveillance court but doing so would breach their extra responsibilities in Europe.

Internet companies say the conflict would force them to ringfence EU operations and hold data about the bloc's citizens in new legal entities there, creating separate islands of data that would lessen the efficiency of their operations and risk balkanizing the internet into separate regional networks. You've Got "Unsecure" MailIn an attempt to circumvent NSA spying, a fast growing Russian internet company, Mail.Ru seeks US expansion. Russia's largest internet company is expanding into the US, trying to lure customers by keeping the data from its services offshore.

Mail.ru, which has more monthly users than any other Russian website, is targeting the US with a suite of mail and messaging apps under the My.com brand as it tries to crack what its chief executive Dmitry Grishin calls "the most competitive and most difficult market that has ever existed".

Mr Grishin said the data centres for its US services would be based in the Netherlands, which he said was a "good neutral place" outside of the US and Russia that was "very liberal" and "respected globally".

The Netherlands has robust data protection laws and a broad definition of what constitutes personal data, as well as some large data centres. However, some privacy experts say keeping the data offshore would not be enough to stop the NSA accessing it.

Jeff Chester, executive director of the Center for Digital Democracy in the US, said the data may be more secure in Europe but the problem was it had to be shipped from the US.

"I don't think it keeps it from the NSA at all because the data are collected here and shipped to the cloud, it doesn't make a difference where it goes," he said. "The NSA can access it during the transportation process."

James Lewis, a security expert at the Center for Strategic and International Studies in Washington, said: "The location of the server makes absolutely no difference, particularly for Russian companies that have very close relations with their security services. Ask Snowden if he feels like his email is safer." Encrypt Everything, Store Nothing!Mail.Ru is not the answer. At some point the data is unencrypted, and accessible to NSA snoops. Enter Wickr, a secure messaging app, that stores nothing and at no point in routing is there an unencrypted message. Wickr, has already received a request from the FBI for a back door. Thankfully, the company cannot provide one because it stores no data. The Financial Times reports US spying fuels popularity of secure messaging app Wickr. Wickr, the secure messaging app that positions itself "halfway between Snapchat and Snowden", is set to raise more funds and launch a major update on Monday after its popularity soared following revelations of a US mass surveillance programme.

The Silicon Valley start-up enables encrypted peer-to-peer communications from email to instant messaging while keeping no data whatsoever. It plans to rival Skype by rolling out secure and private international video calling next year.

Nico Sell, co-founder and chief executive of Wickr, said the year-and-a-half-old company had seen an extreme spike in interest after revelations about the National Security Agency's surveillance programme were published earlier this year.

Wickr works by providing connections between message senders, which are not stored on any central server. Ms Sell said the FBI had already asked for a back door to get information for law enforcement but because the company holds no data, there was not even a way of co-operating.

"I didn't want to be responsible for securing everyone's gold – because that's impossible," she said. As a hacker who helps organise one of the most important hacker conventions of the year, she knew nothing was foolproof. The sender can set how long he or she wants the message to stay on the recipient's computer before deleting itself.

Wickr, which has been downloaded 1m times, is free but will begin to offer advanced subscriptions and in-app purchases next year. Wickr vs. SnapchatSnapchat is a messaging service that provides text and photo messages that dissolve in a few seconds. The Wall Street Journal reports Snapchat Spurned $3 Billion Acquisition Offer from Facebook. Snapchat, a rapidly growing messaging service, recently spurned an all-cash acquisition offer from Facebook for close to $3 billion or more, according to people briefed on the matter. Evan Spiegel, Snapchat's 23-year-old co-founder and CEO, will not likely consider an acquisition or an investment at least until early next year, the people briefed on the matter said. They said Spiegel is hoping Snapchat's numbers – of users and messages – will grow enough by then to justify an even larger valuation, the people said.

Snapchat specializes in ephemeral mobile messages, including text or photographs, that disappear after a few seconds. The service has not generated any revenue, but is especially popular among teenagers and young adults, who use the app to send messages to friends.

Facebook is interested in Snapchat because more of its users are tapping the service via smartphones, where messaging is a core function. Facebook has rapidly increased the share of its revenue coming from mobile advertising, but said last month that fewer young teens were using the service on a daily basis.

Tencent, a diverse Internet company, owns WeChat, a major messaging service in China, and has a stake in KaKao, a popular South Korean app. It was vying to lead a group of investors that had offered to invest $200 million in Snapchat at a valuation of roughly $4 billion. Meaning of $3 BillionSnapchat has no profit and no revenues. Last year it was reportedly worth $100 million. Now it is worth $3 billion. I cannot fathom turning down an all cash offer of that amount. Isn't $3 billion enough to do whatever you want for the rest of your life? Would $10 billion make one happier? Is the race on to see what deal gets valued at $100 billion? $1 trillion? Wickr Business ModelLeaving philosophical questions aside, Let's take a closer look at the model of Wickr straight from its website. The Internet is forever.

Your private communications don´t need to be.

Wickr is a free app that provides:

- Military-grade encryption of text, picture, audio and video messages

- Sender-based control over who can read messages, where and for how long

- Best available privacy, anonymity and secure file shredding features

- Security that is simple to use

"Wickr - an iPhone encryption app a 3-year-old can use."

New York Times: "There is no reason your pictures, videos and communications should be available on some server, where it can easily be accessed by who-knows-who, or what service, without any control over what people do with it." Wickr vs. Silk RoadThe government shut down " Silk Road", but that model had a fatal problem. It stored data. From the Wickr privacy policy... - We use military-grade encryption. Our encryption is based on 256-bit symmetric AES encryption, RSA 4096 encryption, ECDH521 encryption, transport layer security, and our proprietary algorithm.

- We canʼt see information you give us. Your information is always disguised with multiple rounds of salted, cryptographic hashing before (if) it is transmitted to our servers. Because of this we donʼt know — and canʼt reveal — anything about you or how you use the Wickr App.

- Deletion is forever. When you delete a message, or when a message expires, our "secure file shredder" technology uses forensic deletion techniques to ensure that your data can never be recovered by us or anyone else.

- You own your data. We do not share or sell any data about our users. Period.

What Information Does Wickr Collect, and How Is It Used?

We are committed to limiting our collection of your information to what is necessary to provide you with our Services.

We only collect information from users who create Wickr Accounts. You must create a Wickr Account to use the Wickr App.

What We Donʼt Collect:

Equally important to us is the information we donʼt collect. We will NEVER collect any location information or have access to the contents of the communications you send using the Wickr App. After messages are deleted (or after they expire), they are forensically deleted and are not retrievable by us or anyone else. (Remember, however, that if you send a Wickr message to another Wickr user, that message might remain on their device even after you delete it from yours, depending on the value you set for the self-destruct time of that message.) Leave No Trace!I commend any app or any service that stops NSA spying in its tracks. But don't blame me or Snowden if such services become used by crooks, or worse. Were it not for the massive, unwarranted spying, people would not be so paranoid as to demand these services in the first place. The end result is as expected: Governmental spying, back doors, denials, and loss of the constitutional right to privacy has made us less secure than before. That is precisely what the loss of freedom always does! Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

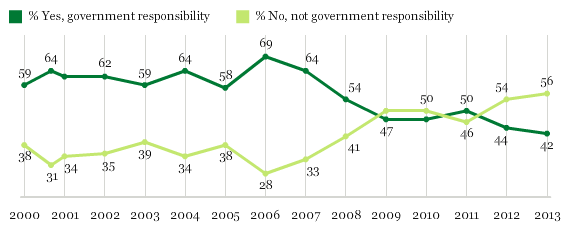

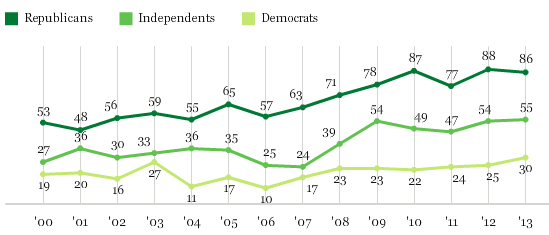

| Majority in U.S. Say Healthcare Not Government's Responsibility Posted: 25 Nov 2013 10:30 AM PST By a 56 to 42 margin, Gallup reports Majority in U.S. Say Healthcare Not Government Responsibility. Question: Do you think it is the responsibility of the federal government to make sure all Americans have healthcare coverage, or is that not the responsibility of the federal government? No Responsibility by Political Party No Responsibility by Political Party Percentage Point Change Since 2000 Percentage Point Change Since 2000- Since 2000, the share of republicans who say healthcare is not the responsibility has increased from 53% to 86%, a rise of 33 percentage points.

- Since 2000, the share of independents who say healthcare is not the responsibility has increased from 27% to 55%, a rise of 28 percentage points.

- Since 2000, the share of democrats who say healthcare is not the responsibility has increased from 19% to 30%, a rise of 11 percentage points.

Percentage Point Change Since 2006- Since 2006, the share of republicans who say healthcare is not the responsibility has increased from 57% to 86%, a rise of 29 percentage points.

- Since 2006, the share of independents who say healthcare is not the responsibility has increased from 25% to 55%, a rise of 30 percentage points.

- Since 2006, the share of democrats who say healthcare is not the responsibility has increased from 10% to 30%, a rise of 20 percentage points.

In 2006, the overall share was 69% to 28% in favor of the view that healthcare was the responsibility! Now it is 56% to 46% against. This is a startling change in sentiment in 7 years, especially among independents. Gallp comments " It is possible that this sharp change has been caused by a politicization of the issue as it became a major part of Obama's campaign platform, and as he and other Democratic leaders pressed for and passed the ACA, sometimes called Obamacare, in 2010." However, a close look at the timeline suggests Obamacare cannot be the blame for the bulk of the move. Between 2006 and 2009 the percentage changed from 69% to 28% in favor to 50% to 47% against. Since 2009, the sentiment change has been in the same direction (against the healthcare mandate), but the percentage point move was much smaller. Something happened between 2006 and 2009. What was it? Housing collapse? Demographics? Boomer retirement? Medicare seen as "I got mine. I waited. You can wait too?" The latter would require an illogical disassociation between Medicare and government sponsored healthcare. Regardless of what happened, politically speaking, Obamacare came at a last-chance now-or-never point with public opinion split nearly 50-50. For now, it's waiting time. The next presidential election will determine what major changes in healthcare are coming. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

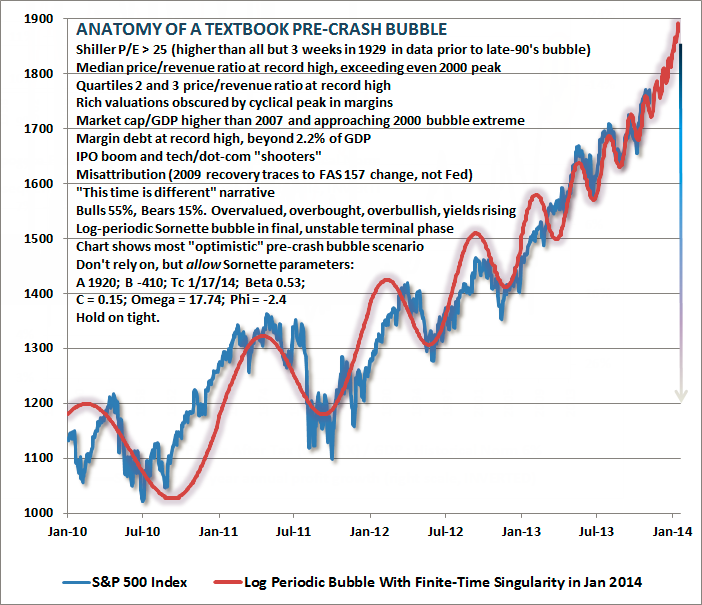

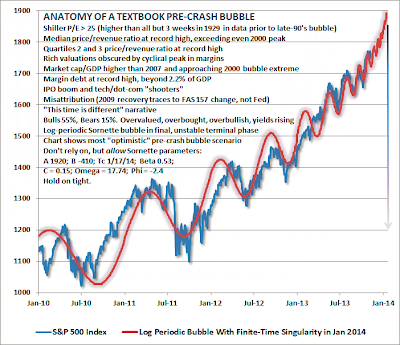

| Hussman's Open Letter to the Fed; The Problem with Bubbles; Textbook Pre-Crash Bubble; Reflections on Not Chasing Bubbles; Integrity vs. Respect Posted: 25 Nov 2013 01:22 AM PST John Hussman's last three weekly emails have been outstanding. Let's take a look at a couple short snips from the first two articles and then a longer snip from his letter to the Fed. Textbook Pre-Crash BubbleNovember 11: Textbook Pre-Crash Bubble by John Hussman Hussman: " The problem with bubbles is that they force one to decide whether to look like an idiot before the peak, or an idiot after the peak." This is exactly how I have felt for two years running. It reminds me of 1999-2000 when tech stocks put on that last big rally. Avoiding a bubble is incredibly hard to do, and this one has been exceptional. Here is a chart from the article with Hussman's comments. Though I don't believe that markets follow math, it's striking how closely market action in recent years has followed a "log-periodic bubble" as described by Didier Sornette (see Increasingly Immediate Impulses to Buy the Dip).

A log periodic pattern is essentially one where troughs occur at increasingly frequent and increasingly shallow intervals. Frankly, I thought that this pattern was nearly exhausted in April or May of this year. But here we are. What's important here is that the only way to extend that finite-time singularity is for the advance to become even more vertical and for periodic fluctuations to become even more closely spaced. That's exactly what has happened, and the fidelity to the log-periodic pattern is almost creepy. At this point, the only way to extend the singularity beyond the present date is to envision a nearly vertical pre-crash blowoff.

At this horizon, even "buy-and-hold" strategies in stocks are inappropriate except for a small fraction of assets. In general, the appropriate rule for setting investment exposure for passive investors is to align the duration of the asset portfolio with the duration of expected liabilities. At a 2% dividend yield on the S&P 500, equities are effectively instruments with 50-year duration. That means that even stock holdings amounting to 10% of assets exhaust a 5-year duration. For most investors, a material exposure to equities requires a very long investment horizon and a wholly passive view about market prospects. Hugh Hendry Throws In TowelOn November 22, InvestmentWeek reported long-time bear Hugh Hendry threw in the towel. 'I can't look at myself in the mirror': Hendry reveals why he has turned bullishSpeaking at Harrington Cooper's 2013 conference, Hendry said he is no longer fighting the "two-way feedback loop" which is continuing to boost risk assets.

"I can no longer say I am bearish. When markets become parabolic, the people who exist within them are trend followers, because the guys who are qualitative have got taken out. I have been prepared to underperform for the fun of being proved right when markets crash. But that could be in three-and-a-half-years' time."

"I cannot look at myself in the mirror; everything I have believed in I have had to reject. This environment only makes sense through the prism of trends." Trend Is Your Friend Until It ChangesHendry is now looking for 'auto-correlations' that benefit from this feedback loop. " You have got to be in things that are trending," says Hendry. Why Now? The market has been trending ever since March 2009. There were a few pullbacks along the way, but every one was bought with vigor. Does that mean the next one will be bought? Hardly. And why should it? My friend Pater Tenebrarum at the Acting Man blog commented via email ... " Hendry's change in stance is akin to Druckenmiller covering all his shorts in Internet stocks in November of 1999 and going long tech. The internet stock shorts he covered topped out two weeks later (they topped well before the Nasdaq did), the Nasdaq's final high came in early March, about 3 months later. Thereafter, an 85% decline in the index - and 3/4 of the internet stocks in which Druckenmiller covered shorts eventually went to ZERO, while the remainder fell between 90% to 99%." Hendry is aware, but unconcerned about that possibility. Said Hendry ... " I may be providing a public utility here, as the last bear to capitulate. You are well within your rights to say 'sell'. The S&P 500 is up 30% over the past year: I wish I had thought this last year. Crashing is the least of my concerns. I can deal with that, but I cannot risk my reputation because we are in this virtuous loop where the market is trending." Wow. Given valuations, crashing should be everyone's big concern. But if it was, prices would not have gotten this ridiculous in the first place. Reflections on Not Chasing BubblesNovember 18: Chumps, Champs, and Bamboo by John Hussman "The seed of a bamboo tree is planted, fertilized and watered. Nothing happens for the first year. There´s no sign of growth. Not even a hint. The same thing happens – or doesn´t happen – the second year. And then the third year. The tree is carefully watered and fertilized each year, but nothing shows. No growth. No anything. Then the bamboo tree suddenly sprouts and grows thirty feet in three months." ― Zig Ziglar

This story is more than a quote about persistence – it's actually a reasonable description of risk-managed investing.

At bull market peaks, it often seems that the market is simply headed higher with no end in sight, and "buy-and-hold" appears superior to every alternative. Meanwhile, the reputation of value-conscious investors and risk-managers goes from "champ" to "chump." Then, the bamboo tree suddenly sprouts, and the entire lag is often replaced by outperformance in less than a year. Only after the fact does the reputation of risk-managed strategies surge from "chump" to "champ." By then, it's unfortunately too late to be of help to many investors who capitulated in frustration at the peak.

As Jeremy Grantham at GMO has observed, "we often arrive at the winning post with good long-term results and less absolute volatility than most, but not necessarily with the same clients that we started out with." Hussman's Open Letter to the FedNovember 25: An Open Letter to the FOMC: Recognizing the Valuation Bubble In Equities by John Hussman

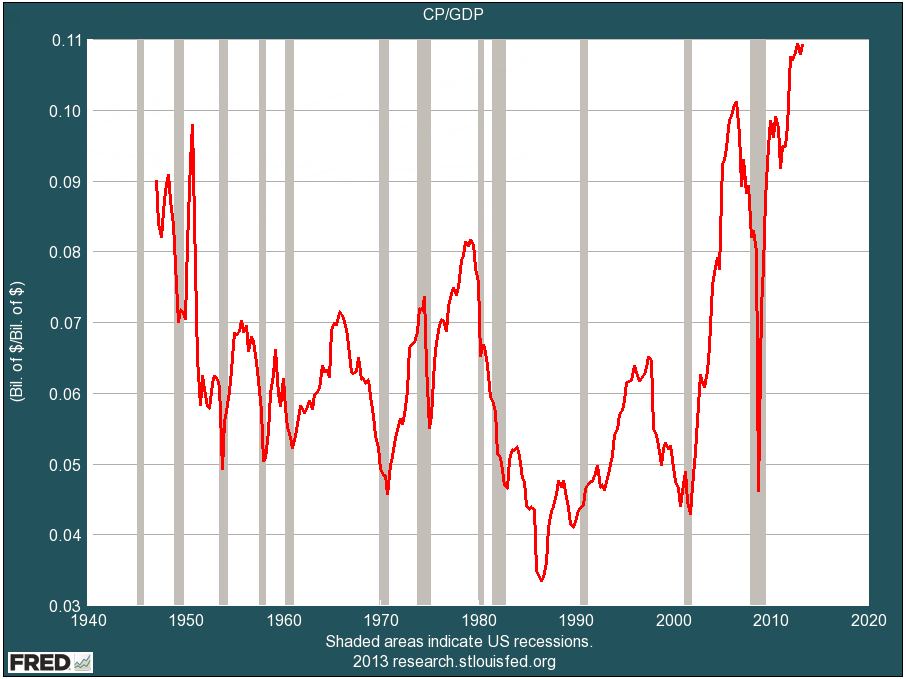

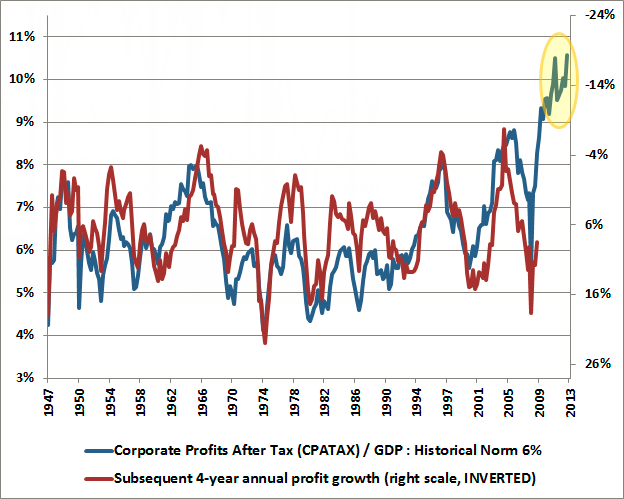

The chart below is from one of the best tools that the Fed offers the public, the Federal Reserve Economic Database (FRED). The chart shows the ratio of corporate profits to GDP, which is presently at a record. The fact that profits as a share of GDP are more than 70% above their historical norm should immediately raise a question as to whether current year earnings or next year's projected "forward earnings" should be used as a sufficient statistic for long-term cash flows and equity market valuation without any further reflection. Then again, more work is required to demonstrate that such an approach would be misleading. We're just getting warmed up.

A simple way to see the implications of the present elevation of the profit share is to relate the level of profit margins to subsequent growth in profits over a reasonably "cyclical" horizon of several years. Remember, when one values equities, one is valuing a long-term stream, not just next year's earnings. Investors taking current-year or forward-year profits as a sufficient statistic should be aware that high margins are reliably associated with weak profit growth over subsequent years.

The next relevant question is to ask why profit margins are presently so high. One might argue that the profitability of companies has achieved a permanently high plateau. Despite historical mean-reversion in profit margins (which tend to collapse over the full course of the business cycle), maybe this time is different. As it happens, we can relate the surfeit of corporate profits in recent years rather precisely to the extraordinary combined deficits of the household and government sectors during the same period. ....

Corporate profits as a share of GDP are nearly the mirror image of deficits in the household and government sectors. A simple way to think about this is that dissaving in both sectors helps to support corporate revenues and limit the need for competition, even when wages and salaries are depressed. It follows that most of the variability in corporate profits over time is driven by mirror image variations in the household and government sectors. ....

The fact is that valuation measures driven by single-period earnings (whether trailing earnings or forward operating earnings) are poorly correlated with subsequent market returns, mainly because they impose the counterfactual assumption that profit margins can be held constant over time.

Though Fed officials including Alan Greenspan and Janet Yellen seem attracted to the seemingly elegant simplicity of these "equity risk premium" models, they seem somehow oblivious to the fact that they don't actually work.

Why is the historical record of these simple "equity risk premium" estimates such a cacophony of noise? The answer should be immediately apparent. It turns out that the error between these estimates and actual subsequent 10-year S&P 500 total returns (in excess of 10-year Treasury yields) has a correlation of 0.86 with – you guessed it – profit margins. With profit margins at the highest level in history, the record suggests that these models are grossly overestimating prospective equity returns at today's all-time stock market highs. Unfortunately, this evidence also suggests that the faith expressed in these "equity risk premium" estimates by Janet Yellen and others is likely to coincide with their most epic failure in history.

My strong disagreement should not be confused with disrespect, and none is intended, but wasn't it Janet Yellen who in October 2005, at the height of the housing bubble, delivered a speech effectively proposing that monetary policy could mitigate any negative economic consequences of a housing collapse, and arguing that the Fed had no role in preventing further housing distortions? Given the lack of concern with the present elevation of the equity markets, these remarks from 2005 have a rather ominous ring in hindsight:

"First, if the bubble were to deflate on its own, would the effect on the economy be exceedingly large? Second, is it unlikely that the Fed could mitigate the consequences? Third, is monetary policy the best tool to use to deflate a house-price bubble? My answers to these questions in the shortest possible form are, 'no,' 'no,' and 'no.'"

The reason that the Fed does not see an "obvious" stock market bubble (to use a word regularly used by Governor Bullard, as if to imply that misvaluations cannot exist unless they smack their observers with a two-by-four) is because while price/earnings multiples appear only moderately elevated, those multiples themselves reflect earnings that embed record profit margins that stand about 70% above their historical norms.

We can demonstrate in a century of evidence that a) profit margins are mean-reverting and inversely related to subsequent earnings growth, b) margin fluctuations are largely driven by cyclical variations in the combined savings of households and government, and importantly, c) valuation measures that normalize or otherwise dampen cyclical variation in profit margins are dramatically better correlated with actual subsequent outcomes in the equity markets.

If one examines the stocks in the S&P 500 individually, the median price/revenue multiple is actually higher today than it was in 2000 (smaller stocks were more reasonably valued in 2000, compared with the present). This is a dangerous situation. In this context, the dismissive view of FOMC officials regarding equity overvaluation appears misplaced, and seems likely to be followed by disruptive financial adjustments.

One obtains a similar view, with equal historical reliability, from the ratio of nonfinancial equity capitalization to nominal GDP, using Federal Reserve Z.1 Flow of Funds data. On this measure, equities are already beyond their 2007 peak valuations, and are approaching the 2000 extreme. The associated 10-year expected nominal total return for the S&P 500 is negative.

Fed PolicyHussman concludes with a discussion on Fed policy ... The policy of quantitative easing has run its course. It undermines planning, as every economic decision must be made in the context of what the Federal Reserve may or may not do next. It starves risk-averse savers, the elderly, and the disabled from interest income. It lowers the bar for speculative, unproductive, low-covenant lending (as it did during the housing bubble). It relaxes a constraint that is not binding – as there are already trillions of dollars in idle reserves at U.S. banks, on which the Federal Reserve pays interest both to keep them idle and to avoid disruptions in short-term money markets. It undermines price signals and misallocates scarce savings to speculative pursuits. It further skews the distribution of wealth, and while the extent of this skew has a scarce chance of persisting, the benefits of any spending from transiently elevated stock market wealth will accrue to primarily to higher-income individuals who are not as constrained as the millions of lower-income, low-asset families hoping for some "trickle-down" effect. We have seen numerous variants of this movie before, and we should have learned the ending by now.

Importantly, the magnitude of the "wealth effect" on employment is dismally small. Even if the entire relationship between stock market fluctuations and employment fluctuations was causal and one-directional, it would still take a roughly 40% advance in the stock market to draw the unemployment rate down by 1%. Unfortunately, price advances do not create the underlying cash flows to support them, so the strategy of manipulating stock prices higher also involves a piper that must be paid.

The intent of this letter is not to criticize, but hopefully to increase the mindfulness of the FOMC as to historical evidence, the strength of various financial and economic relationships, and the potentially grave consequences of further relaxing constraints that are not binding in the first place. Integrity vs. RespectIn the opening paragraph, Hussman, stated (to the Fed) " I don't question your motives or integrity." I side solidly with Hussman on this point although many believe this is all part of some "grand plan" for the Fed or big banks to take over the world. Yet, I cannot offer Hussman's same sense of "no disrespect". We are in this mess, precisely because the Fed blows bubbles of increasing magnitude over time. It happens time and time again, and every time banks are bailed out at the expense of the poor and middle class. The Fed deserves no respect for what they have done and the problems they have caused. They deserve no respect for missing the dotcom bubble, for missing the housing bubble, and for missing this bubble. John and Aretha can sing " Respect", but I sure can't. Respect One Hell of a Time To Become a Trend FollowerEveryone who believes in valuation metrics would do themselves a favor to click on the three links by Hussman that I presented, and read the articles in entirety. As I stated upfront, avoiding bubbles is incredibly hard to do, and this one has been exceptional. But that is precisely the problem with bubbles. Hussman points out (and I agree) " The associated 10-year expected nominal total return for the S&P 500 is negative." Read that sentence again and again until it sinks in. Here is another way of putting it. " 10 years from now, the S&P is likely to be lower than it is today". That is how over-valued equities now are. Yes, Hussman sounds like a broken record. And so do I. But this is one hell of a time to become a trend follower. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |