Mish's Global Economic Trend Analysis |

- China Manufacturing PMI Plunges to 32-Month Low of 47.7; Reflections on Stocks Rallying on "Bad News"

- China to Protect Iran Even if Result Starts World War III; What's the Best Way to Deal with Iran?

- Maximum Intervention Moves Into Overdrive; Foreign Banks can Fund themselves Cheaper in US Dollars than US Banks; Discount Rate Cut Coming Up?

- China Cuts Bank Reserve Ratios by .5 Percentage Points; Central Banks Cut Rates on Dollar Swap Lines; German 1-Year Bond Yield Negative First Time Ever; Futures Soar

- German Finance Minister says "Big Bazooka" Not Ready, Would Not Stem Crisis, Even IF it Was; Plans Too “Intricate and Complex” for Investors to Understand.

| Posted: 30 Nov 2011 10:56 PM PST Equity markets soared on central bank manipulations and various rumors the past few days. However, neither rumors nor trivial actions (which is all that happened) can save the global economy. Yesterday stocks rallied on news China Cuts Bank Reserve Ratios by .5 Percentage Points and Central Banks Cut Rates on Dollar Swap Lines. However, the reason Chinese central bank reacted is hugely deteriorating conditions in China. The reason the Fed reacted is hugely deteriorating conditions in Europe. Equities have rallied on reported "good news". However the first irony is the global economic picture outside the US is horrendous. The second irony is bottoms are formed on bad news (and tops on good news), but central banks intervention is really bad news widely recognized as good news. With that in mind, please consider the HSBC China Manufacturing PMI for November 2011. November data showed Chinese manufacturing sector operating conditions deteriorating at the sharpest rate since March 2009. Behind the renewed contraction of the sector were marked reductions in both production and incoming new business. The latest survey findings also showed a marked easing in price pressures, with average input costs falling for the first time in 16 months. In response, manufacturers reduced their output charges at a marked rate.China Manufacturing PMI  Stocks ignoring bad news is normally a very good sign. Stocks rallying on government intervention as bad news is presented as good is a different story indeed. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| China to Protect Iran Even if Result Starts World War III; What's the Best Way to Deal with Iran? Posted: 30 Nov 2011 06:31 PM PST Does the US have the right to defend itself? If so why doesn't any nation have the right to defend itself? What is the best way for the US to deal with Iran? Here is a video in Chinese, with English subtitles, in which China says it will defend Iran. Link if video does not play: "China will not hesitate to protect Iran even with a third World War" Here are a few panels about 2 minutes 15 seconds into the video in which China states an intent to protect Iran, if Iran is attacked, even if it means World War III.   I support the position (a few moments later and shown in the screen shot below) that suggests the Iranian people have little trust in their leaders and the best way to deal with Iran is to let the people rise up against the government as happened in Egypt and Libya.  With the US threatening Iran at every turn, and with the needless war in which the US destroyed Iraq killing or ruining the lives of hundreds-of-thousands of Iraqis, it is no wonder Iran wants to protect itself. Any country would want to do the same. The US has no business instigating another war, yet that is exactly what economic sanctions are. The downright scary policies of Mitt Romney and Newt Gingrich go even further, and would have the US marching off to World War III before we know it. The best way for the US to deal with Iran is to support the Iranian people (not the leaders). Nearly all the private citizens of Iran would have no grudge against the US if we would simply stop our policies of aggression in the region. We do not need another war and certainly cannot afford one. Ron Paul offers the best hope of stopping yet another disastrous, and needless march to war. In case you missed it, please consider President Obama and Mitt Romney are Nearly One and the Same! Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 30 Nov 2011 08:54 AM PST Steen Jakobsen, chief economist for Saxo Bank offers his take on the liquidity moves by global central bankers. Please consider Steen's Chronicle, Maximum Intervention Moves Into Overdrive Our theme for Q4 was 'Maximum Intervention' and today was a new high for this exact concept. The day after the European Union Finance Ministers (ECO-FIN) meeting (which once again failed to produce any progress on the EU debt crisis) the Chinese cut the RRR-ratio - the minimum reserves each commercial bank must hold of customer deposits and notes - from 21.5 percent to 21.0 percent. (The RRR started the year in 18.5 percent and this is the first cut since 2008. Back in 2006 the RRR ratio was just below 8.0 percent for a number of years.) This is an indication that China's help to the growing outlook of a 'Perfect Storm' will be monetary easing despite relatively stubborn inflation numbers.Discount Rate Discussion The Federal Reserve website has this discussion of the Discount Rate. The discount rate is the interest rate charged to commercial banks and other depository institutions on loans they receive from their regional Federal Reserve Bank's lending facility--the discount window. The Federal Reserve Banks offer three discount window programs to depository institutions: primary credit, secondary credit, and seasonal credit, each with its own interest rate. All discount window loans are fully secured.Discount Window  Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

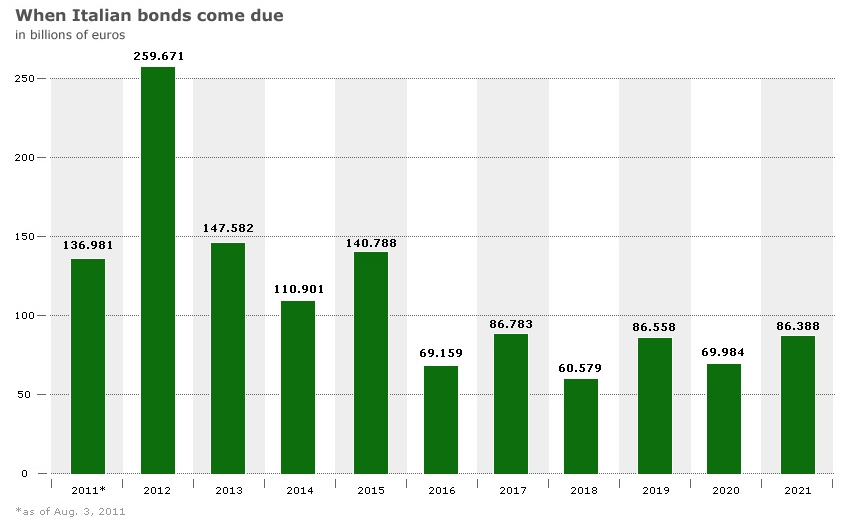

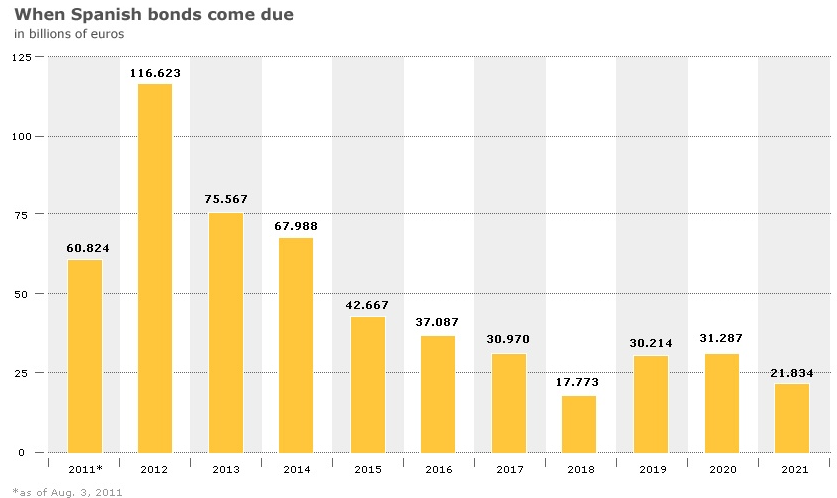

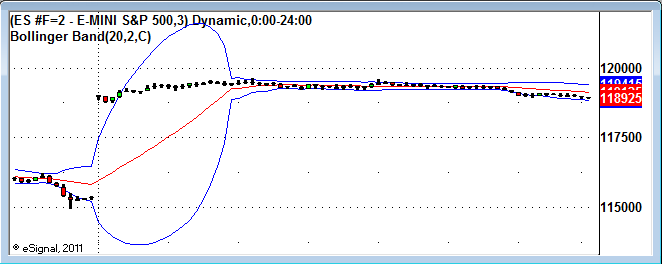

| Posted: 30 Nov 2011 07:09 AM PST Equity futures sharply reversed an overnight pullback on a pair of central bank actions, one in China, the other an agreement between the US and Europe. China Cuts Bank Reserve Ratios by .5 Percentage Points The Wall Street Journal reports China Cuts Reserve-Requirement Ratio The People's Bank of China, China's central bank, said Wednesday it will cut the reserve-requirement ratio for banks by half of a percentage point, the first such cut since December 2008. The cut essentially frees up banks to lend additional money.Central Banks Cut Rates on Dollar Swap Lines Bloomberg reports European Stocks Rally After Central Banks Cut Rates on Dollar Swap Lines European stocks rallied for their longest stretch of gains in seven weeks as the Federal Reserve and five other central banks lowered the cost of dollar funding and China cut its reserve ratio for banks.German 1-Year Bond Yield Negative First Time Ever Investment Week reports German 1-year bunds move to negative yield for first time ever The yield on 1-year German bunds turned negative today for the first time ever, according to Bloomberg data, as the European Central Bank looks set to ramp up measures to fight the debt crisis.S&P Equity Futures are up another 3 Percent, Bond Market Yawns Global equities are sharply higher with this global coordinated action. S&P 500 futures are up another 3 percent and will gap higher. Meanwhile Spanish 10-year bonds rallied (yields fell) a mere 7 basis points to 6.32%, Spanish 2-year bonds rallied a mere 8 basis points to 5.51%, Italian 10-year bonds rallied 10 basis points to 7.13%, and Italian 10-year bonds rallied 9 basis points to 7.00%. Whatever the equity markets see, the bond market doesn't. A flight to safety of German bonds is back on, that China needs to cut reserve requirements is a huge sign of weakness (and no it will not stop a hard Chinese landing). Also bear in mind that on September 15, there was coordinated swap-line action that did nothing. Bloomberg reports ECB Coordinated Policy Action Is 'Big Deal,' Blanchflower Says September 15, 2011 11:35 AM EDTHere is an interesting chart on ZeroHedge that shows what happened the last time there was coordinated swap-line action.  What's Changed? Nothing much that I can see. China cut the reserve-requirement rate to 21% from 21.5% and the Fed and ECB renewed swap lines at a slightly lower rate. Yields on Italian bonds are still at or above 7%, and nothing has been done to solve any long-term structural issues. Nonetheless it's party time for equities, crude, and metals, particularly gold and copper. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 30 Nov 2011 12:39 AM PST In a huge non-surprise to the bond markets (but not to bullish equity buffoons), Wolfgang Schauble admits euro bail-out fund won't halt crisis Europe's "big bazooka" bail-out fund is not ready and won't stem the debt crisis that on Tuesday pounded Italy and the European Central Bank (ECB), admitted Wolfgang Schauble, Germany's finance minister.Necessary Conditions Met?! The only way "necessary conditions" can possibly have been met is if "necessary conditions" have changed. Germany, the Netherlands, and the IMF have all insisted that all Greek coalition leaders sign off on agreement to IMF and EU demands. However, the leader of the Greek New Democracy party still refuses to sign as noted on November 22 in Showdown in Greece; EU Gives Deadline on Signatures; Samaras Won't Sign, Sends Letter Instead, Seeks Policy Changes. Either the EU has blinked or I missed a "signing party". Regardless, Greece is going to default anyway, signing party or not. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |