Mish's Global Economic Trend Analysis |

- Armageddon Delayed; All Quiet on the European Bond Front; Italy and Spain Bond Schedule through 2021; Belief in Fairy Tales

- OECD Global Economic Outlook: "Muddling Through" with Slow US Growth, Europe Entering a "Minor Recession"

- Treasury Secretary Henry Paulson Tipped Off Prominent Hedge Funds Regarding Fannie Mae While Telling the US Senate and General Public a Different Story

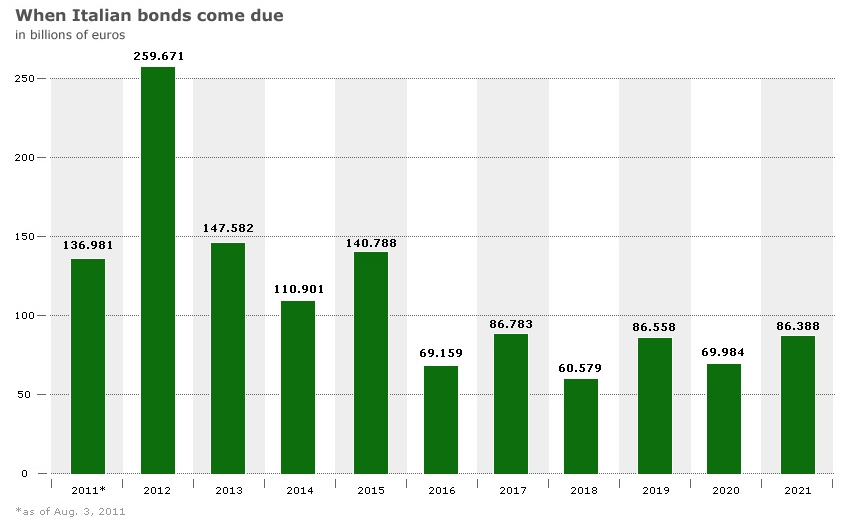

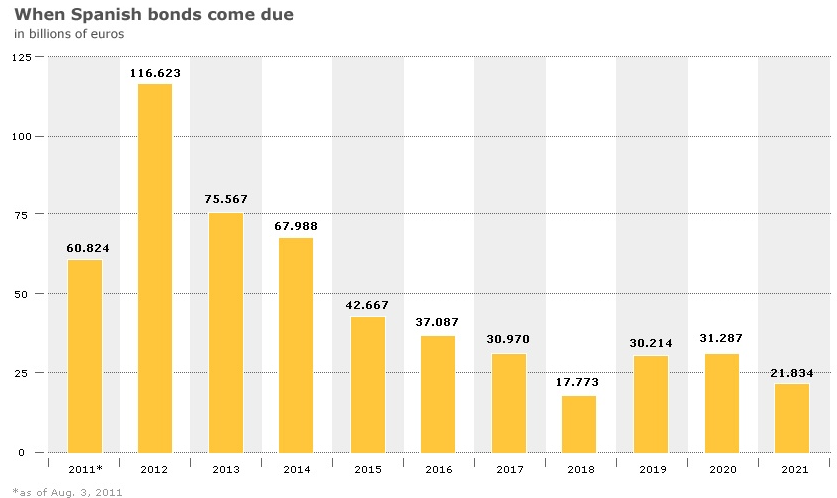

| Posted: 29 Nov 2011 11:10 AM PST European bonds had a good day today. A good day is when nothing blows up. Italy 10-Year Government Bonds  Italy 2-Year Government Bonds  Germany 10-Year Government Bonds  Germany 2-Year Government Bonds  After a brief spurt higher, which sent S&P futures down a percent last evening, Italian bonds settled flat as did German bonds. In spite of the fact that Italian debt yields are above 7%, this was a "good" day. Belief in Fairy Tales Steen Jakobsen, chief economist from Saxo Bank in Copenhagen notes a huge belief in fairy tales. Steen writes via email .... There is HUGE believe in the ECOFIN meeting producing news, good news on the fiscal union. Some commentator speculate we will be in EU Heaven.Italy and Spain Bond Schedule through 2021 Here are bond schedule charts from Bloomberg that highlight the difficulty for Italy and Spain for the next few years. Italian Debt Schedule  Spanish Debt Schedule  Armageddon Delayed I picked up those charts from Pater Tenebrarum who writes Apocalypse Postponed – For Now Apocalyptic Unanimity Yesterday, we were struck by the increasing convergence of the views of various market observers as to the outcome of the ongoing crisis. It seems now widely accepted as almost a fait accompli that the euro will disintegrate within weeks. Even Jim Cramer (euro bears please take note…) is now on 'Defcon 3', predicting imminent 'financial collapse'. The Economist writes 'Unless Germany and the ECB act quickly, the single currency's collapse is looming'.The boat was too one-sided for now. However, a relief rally and a global recovery are two different things. The euro-boat is filling up with water and will eventually sink, only the timing of when and how is unknown. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 29 Nov 2011 10:29 AM PST Inquiring minds are watching a short video on the OECD Global Economic Outlook. Video Synopsis

The central OECD forecast is "muddling through" with US growth recovering slowly. Europe allegedly will enter a "minor recession" Let me opine, that global "muddling through" is the absolute best one could conceivably expect and even that would take a near-miracle. Is "muddling through" what the stock market is priced for? I think not. The idea Europe will have a "minor recession" is nonsense in and of itself. Reflective of the Keynesian clowns they are, the OECD jumps on the fiscal stimulus idea, ignoring the fact we are in this mess precisely because of inane monetary stimulus by the Greenspan Fed accompanied by inane fiscal stimulus policies globally. The Keynesian clown prescription is always more-more-more until and even after things blow sky high. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 29 Nov 2011 01:52 AM PST I have on numerous occasions made the claim that Henry Paulson is guilty of coercion and fraud. For those actions, he should be arrested and criminally tried. However, the latest disclosure in which hedge funds say they were tipped off by Paulson while he told Congress and reporters blatant lies is allegedly not even criminal behavior. Bloomberg reports Paulson Gave Hedge Funds Advance Word Treasury Secretary Henry Paulson stepped off the elevator into the Third Avenue offices of hedge fund Eton Park Capital Management LP in Manhattan. It was July 21, 2008, and market fears were mounting. Four months earlier, Bear Stearns Cos. had sold itself for just $10 a share to JPMorgan Chase & Co. (JPM)Who Was at the Meeting?

Tipping Hands Brosens and Rattner both confirmed in e-mails that they had attended and said they couldn't recall details. They didn't respond when asked whether they traded in Fannie Mae- or Freddie Mac-related instruments after the meeting. Chanos declined to comment.What did PIMCO know and When? Anyone who says they do not remember a meeting like that is a liar. Anyone who says "no comment" is indeed commenting and the possible interpretation is not pretty. So what else did Paulson say? I would like to know who Paulson talked to outside the meeting. Bill Gross at PIMCO put on a huge bet, buying not equity shares but Fannie and Freddie bonds in the belief their debt would be guaranteed by the government. Gross bet the firm and won his bet as shareholders were wiped out. So, what did Gross know and when? Was it a guess, or a known deal? Sadly, there is no way to avoid questions of this nature when treasury secretaries and other high-ranking public officials have routine conversations with former colleagues giving them valuable inside information while telling blatant lies to the public. How many people were suckered into buying Fannie and Freddie while hedge funds were told in advance to dump shares? What Paulson did may not have been illegal (acting on the information would have been), which makes the comment by William Poole, a former president of the Federal Reserve Bank of St. Louis seem downright bizarre. Said Poole ... "It seems to me, you've got to cut the guy some slack, even if he tipped his hand. How do you prepare the market for the fact that policy has changed without triggering the very crisis that you're trying to avoid? What is he supposed to say without misleading these people?" On second thought, Poole's comments are not bizarre, they are 100% inane, well beyond the inane idea that the market needs to be prepared for anything, even IF there was a legal way to do it. Poole's idea of preparing the market means telling the big boys how to make billions, while screwing the little guy. Poole is another player deserving your contempt and scorn. Rolling List of High Profile Fraud Targets This list is incomplete. I have stopped updating it, it got so long.

Please note that last item on the list, the first chronologically (as well as the two right above it), all involving Paulson. His actions are a disgusting tribute to the failed ethics of a man truly deserving of being spit in the face by every citizen in the country. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment