Mish's Global Economic Trend Analysis |

- "Crash Tax" Ripoff Expands in California and New York

- Credit Default Swaps PIIGS vs CINN Group (California, Illinois, New York, New Jersey)

- Housing Bubble in Norway

- European Sovereign Debt Crisis in Pictures; PIIGS Spreads to Germany at or Near Record Levels

| "Crash Tax" Ripoff Expands in California and New York Posted: 31 Dec 2010 04:46 PM PST You pay taxes for services. At least you think you do. Fifty cities in California think you don't. They tax the hell out of you, then bill you if you need services. Drivers who cause accidents in at least 50 cities can be billed for the police and firefighters who show up. Please consider 'Crash taxes' are growing in popularity among cash-strapped California cities At least 50 cities in the state have adopted so-called crash-tax laws allowing local governments to seek reimbursement from insurance companies for the costs of sending public emergency crews to accident scenes. The fees can amount to hundreds or even thousands of dollars. If insurers don't pay, cities can hire collection agents to seek payment from the motorists involved.The gall of Rick Benner of Fire Recovery USA and Costa Mesa Fire Battalion Chief Bill Kershaw infuriates me. Firefighters together with police unions they have bankrupted most cities in the nation. Public union firefighters and police (in general) are the most overpaid undeserving ungrateful ingrates the country has ever known. Those statements will annoy many, but it is the truth, in general, especially for the larger cities. If you are a small town police officer or firefighter with few benefits then what I said may not apply to you. I would gladly support collection measures if tax dollars did not already go to overbloated, untenable public union pension contracts. Spare me the sap about how dangerous the jobs are. Please consider the 8 Most Dangerous Jobs in the World 1. Fishermen 2. Pilots and airline employees 3. Loggers 4. Structural construction workers 5. Waste management employees 6. Farmers and ranchers 7. Power-line technicians 8. Roofers The true heroes deserving of respect and appreciation are volunteer fire departments. The problem is expenses not lack of revenues. Cities ought to outsource both police and firefighters, the latter to volunteer departments in return for reduced or eliminated property taxes. How many people do you think would volunteer for a few days a month in return for elimination of property taxes? I bet enough to get rid of nearly every public union fire department in the country. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||||||||||||||||||||||||||

| Credit Default Swaps PIIGS vs CINN Group (California, Illinois, New York, New Jersey) Posted: 31 Dec 2010 12:04 PM PST In response to European Sovereign Debt Crisis in Pictures; PIIGS Spreads to Germany at or Near Record Levels I received this chart from Chris Puplava at Financial Sense.  click on chart for sharper image Chris writes "In addition to foreign credit risk (Greece, PIIGS), I'm seeing my CINN STATE (CA, IL, NY, NJ) Credit Default Swap (CDS) composite moving higher again." Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||||||||||||||||||||||||||

| Posted: 31 Dec 2010 09:40 AM PST Here is a quick post under the theme "Housing Bubbles Around The World". This one is from Norway, courtesy of reader Espen Johansen. Dear MishInflation Adjusted Housing Prices In Norway  Norway Homes Prices In Gold  Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||||||||||||||||||||||||||

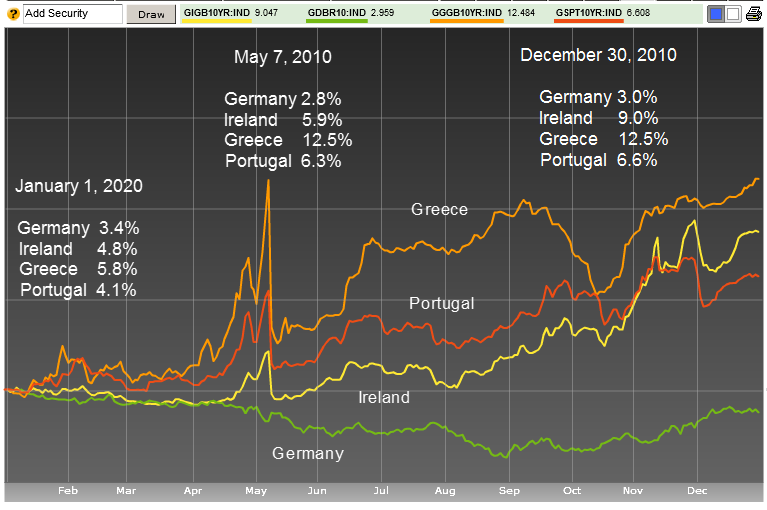

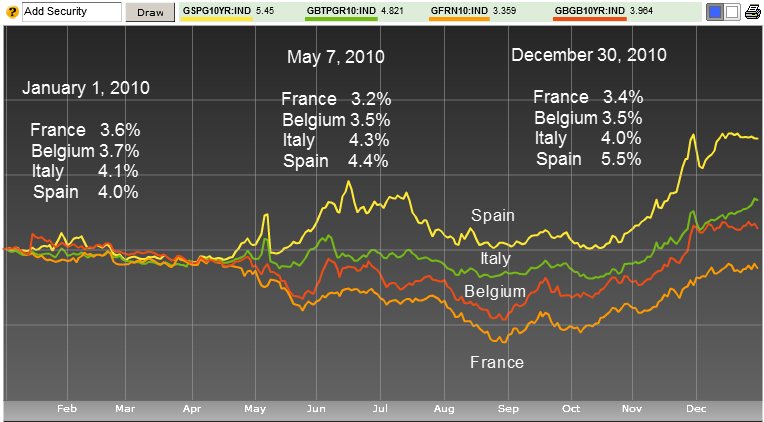

| European Sovereign Debt Crisis in Pictures; PIIGS Spreads to Germany at or Near Record Levels Posted: 31 Dec 2010 02:14 AM PST The sovereign debt crisis in Europe is still simmering. Country by country, spreads to German debt are at or near record levels. Chart follow snips from German Bonds Climb in 2010 as Fiscal Crisis Roils Euro Area German bunds climbed this year, the best performance since 2008, as the fiscal crisis that roiled the euro area's most-indebted nations drove investors to the safest fixed-income assets in the region.Germany, Ireland, Portugal, Greece Sovereign Debt Yields  click on chart for sharper image France, Spain, Belgium, Italy Sovereign Debt Yields  click on chart for sharper image

The bailouts to Greece and Ireland solved nothing. Spain and Portugal are up next. The country to keep an eye on is Italy. It is off nearly everyone's radar right now. Not mine. Italy is simply too big to bail and its spreads are creeping up. Correction: Second chart as originally posted contained a line for Spain that was actually Portugal a second time. Now corrected. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||||||||||||||||||||||||||

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |