Mish's Global Economic Trend Analysis |

- Oregon Tax Revenue from Measure 66 is 50% Short of Predictions; Oregon Grants Unions 4.75% Pay Hike

- 26 of Last 88 Trading Days have been 90% Days (Either Up or Down); 7 More Lean Years in Stock Market?

- Movie Attendance Drops to 1997 Level; Case-Shiller Home Prices Rise; Last Hurrah for Housing

- How Many New Home Sales Was That?

| Oregon Tax Revenue from Measure 66 is 50% Short of Predictions; Oregon Grants Unions 4.75% Pay Hike Posted: 31 Aug 2010 09:15 PM PDT From the dysfunctional state of Oregon comes news that Measure 66 fell about 50% short of its revenue predictions. Balance that with 4.75% pay hikes and it adds up with a continuing refusal by Oregon to address its problems. Oregon Grants Unions 4.75% Pay Hike 5 percent pay increase for Oregon state union employees begins Wednesday A step pay increase of nearly 5 percent for Oregon state workers represented by unions goes into effect Wednesday. The 4.75 percent increase will cost the state as much as $16 million through the end of the two-year budget period.Measure 66 Falls Short Oregon tax revenues from Measure 66 coming up short of predictions Early indicators suggest the state won't receive nearly as much as officials expected from a tax increase on wealthy Oregonians -- raising questions of whether January's bitterly fought election was worth it.Here's the deal. Oregon raised taxes for the benefit of unions and now they have to raise taxes again because the state only got half as much revenue from the tax hike as expected. When does the madness stop? I have written about Oregon a lot recently. Dysfunctional Oregon August 22, 2010: Dysfunctional Oregon Sight unseen, I am willing to state that Oregon should get rid of all 64 state boards, no matter what they are supposed to do. Sight seen, it's time Oregonian voters relegate Gov. Ted Kulongoski to the ash heap of history.Overoptimism Oregon Style August 18, 2010: Oregon Wins Blue Ribbon for Unfounded Optimism; Everything "Weaker than Expected" In July of 2009 state revenue projections were $222.8 million to the plus side. Now just one year later, smack in the midst of a "recovery", a $577.2 million June 2010 deficit is too optimistic by as much as another $500 million.We can now add Measure 66 to the list of overoptimistic misses in Oregon. Edge of the Financial Chasm July 25, 2010: Edge of Financial Chasm Four Problems Oregon Faces.Oregon Taxpayers at Huge Risk over PERS July 24, 2010: Oregon's Public Employee Retirement System (PERS) in Deep Trouble, Taxpayers on the Hook If we finish the year here the system will only be 70% funded. Pray tell what happens if the stock market finished the year down a modest 15% and is flat next year?Oregon Faces Decade of Budget Deficits May 23, 2010: Governor's Study Shows Oregon Faces Decade of Budget Deficits; Support for Unions Wanes in Illinois A study conducted by Oregon Governor Ted Kulongoski shows that Oregon will not be bailed out by a rebounding economy, assuming of course the economy rebounds at all.Business Owners Move Out January 27, 2010: Oregon's Death Spiral; Business Owners Say "I'm moving out" On Tuesday, unions in Oregon won a charred earth victory that will drive already troubled Oregon, straight off the cliff.Look's like that was a decent call on Measure 66. Increased taxes will drive away business. For whose benefit are these tax hikes? Unions that need to be eliminated. Oregon's problems cannot and will not go away as long as political pandering to unions continues. Public union salaries and benefits are Oregon's biggest problem. A tip of the hat to Oregon Live for excellent articles on the economic plight of Oregon. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

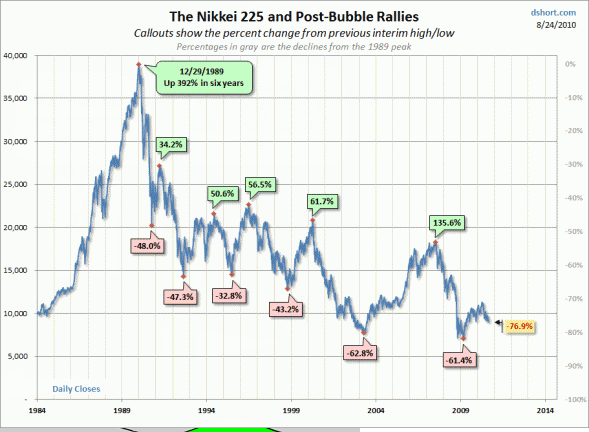

| Posted: 31 Aug 2010 12:20 PM PDT Here is an interesting snip from August 31 Market Commentary by Art Cashin for UBS. Sorry, no link. Monday's market evaporated nearly all the gains from Friday's rally. Despite lighter volume, it was a 90% down day. That means the bears got a lopsided advantage in negative breadth and negative volume. In Friday's rally, the bulls had had a similar 90% advantage. Robert McHugh of Main Line Investors says 26 of the last 88 trading days have been 90% days – one way or another. Any wonder the public is wary.Are these 90% Days a Good Thing? While the big boys push the market around, small investors have thrown in the towel and are not coming back. Market volume now consists of black boxes pushing all stocks one way or the other on 30% of the days. Is this a good thing? For who? Investors or Goldman Sachs? Holding the Line Today, the 1040 level on the S&P held for about the 8th time on "fabulous" news consumer confidence rose to 53. Bear in mind number in the 70's are typical of recession lows. How long the 1040 level can hold is a mystery, but each bounce seems to be weaker and weaker. Last Friday, I noted Market Cheers 1.6% Growth; Treasuries Hammered; while asking "what's next?" We have a partial answer already. Treasuries have regained the entire selloff that started (and ended) on the "great news" that 2nd quarter GDP was +1.6% instead of the expected +1.4%. Nevermind that growth was revised down twice from above +2.5% to +1.6%. Looking ahead, I expect GDP to be negative in the 3rd quarter. Art Cashin's 17.6 Year Cycles A little over a year ago Art Cashin commented Dow Trapped in 17-Year Cycle Art Cashin, director of floor operations at UBS Financial Services, offered CNBC his stock-market insights. Cashin decried the idea of a second stimulus, in light of the "infamous" first attempt.Barry Ritholtz described the 17.6 year cycle in Art Cashin on Secular Cycles "Back On The Cycle – David Rosenberg, formerly chief economist at Merrill Lynch and now at Gluskin Sheff was a guest host on CNBC's Squawkbox this morning. During the discussion he alluded to an 18 year cycle in the market. Not to quibble but many traders have thought of it as the 17.6 year cycle. Here's how I outlined it back in May 2002: Yesterday, as the elders were being asked about the hiding place of the great Bull Market one of the fogeys mentioned the "near 18 year cycle." Like the fat and lean years, it refers to so-called "easy" times to make money in the market versus times requiring much harder work. The fogeys suggested it was near 18 years because it was approximately 17 years, 7 months. For ease of explanation to the juniors, one of the fogeys decimalized the number as 17.6 years so they could use their calculators. He then postulated this example – Let's say the markets topped out in about February 2000. Let's call that 2000.2. Subtract 17.6 and your back in about July 1982 (1982.60). The Dow was around 900. So you could see why those were a fat (easy) 17 years. Take away 17.6 again and you are back around January of 1965 and the Dow is around 900. (Yup – just like 1982.) Many twists and turns in those 17 years. Lots of chances to make money. But you had to work for every penny. Take away 17.6 again and you are back around May of 1947. The war is over. The Dow is around 170. Lots of prosperity ahead. Take away 17.6 and you are back around Sept of 1929 and the Dow is around 350. He began to go on. The juniors had had enough. Folks don't like to hear that you can do well only if you do your homework everyday. Having lived through two of those cycles, we can attest to the work cycle."From where the market is today, Cashin is essentially describing the Japanese scenario of two lost decades. That has been my preferred scenario for quite a long time. Japan's Lost Decades Rallies  If Cashin is correct, and I believe he is, it's another 7 years of nowhere at best for the stock market. Nonetheless, there will be trading opportunities in both directions as the above chart from Business Insider shows. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Movie Attendance Drops to 1997 Level; Case-Shiller Home Prices Rise; Last Hurrah for Housing Posted: 31 Aug 2010 09:42 AM PDT Movie attendance is down but increased prices made up the difference for now. Bloomberg reports Summer Movie Box-Office Attendance Falls to Lowest Since 1997 Summer movie attendance fell to the lowest level since 1997, while soaring ticket prices produced record revenue for Hollywood studios and theater owners.The price-conscious majority appears to be overwhelmed by the price-insensitive wealthy, at least for the time being. How much longer this lasts with cheap movie rentals and another downturn in the economy remains to be seen. Regardless, the results portray an increasing dichotomy between the "haves" and the "have-nots". As long as Hollywood can get away with inceasing prices, they will do just that, even if it means an increasing percentage of customers are "priced out". Last Hurrah for Housing Case-Shiller Home Prices in 20 U.S. Cities Rise More Than Forecast Home prices in 20 U.S. cities rose more than forecast in June from a year earlier, reflecting the influence of a government tax incentive and a sign the market was stabilizing before sales plunged in July.Last Hurrah for Housing Case-Shiller is a backward looking index. The increasing number of foreclosures, the complete collapse in new home sales, a massive increase in inventory, and the end of tax credits all suggest we are near the end of the line for this bounce in home prices. Interestingly, even the home builders are against another home tax credit. Is that reflective of the massive distortions caused by the credit, the realization the tax credit was useless, or the fact that homebuilders recognize there is little chance Congress will back another tax credit? Regardless, here's the deal: New Home Sales Consensus 330K, Actual 276K, a Record Low. As a followup please see How Many New Home Sales Was That? Expect to see new all time low prices in some cities later this year or next year as pent-up demand dries up along with incentives that merely brought that demand forward. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| How Many New Home Sales Was That? Posted: 31 Aug 2010 12:08 AM PDT People are still emailing me, making a mountain out of a molehill of a Rosenberg statement I quoted in Burning Down the House; New Home Sales Consensus 330K, Actual 276K, a Record Low; Nationwide, Zero New Homes Sold Above 750K I failed to comment yesterday on the huge miss by economists on consensus new home sales, but Rosenberg has some nice comments today in Breakfast with Dave.How Many is Zero?The high-end market, in particular, is under tremendous pressure. In fact, it is becoming non-existent. Guess how many homes prices above $750k managed to sell in July. Answer — zero, nada, rien; and for the second month in a row. Only 1,000 units priced above 500,000 moved last month. That's it! Over 80% of the homes that the builders managed to sell were priced for under $300,000. Just another sign of how this remains a full-fledged buyers' market — at least for the ones that can either afford to put down a downpayment or are creditworthy enough to secure a mortgage loan (keeping in mind that 25% of the household sector does have a sub-600 FICO score). There are a couple of issues here. 1. New home sales are recorded at contract signing. So recent closings at a higher rate do not count. Nor do existing home sales. Many of those complaining were looking at closing data or existing home sales. 2. The other factor is rounding error. Rosenberg should not have been so emphatic. From the Census Bureau New Home Sales Spreadsheet Table 2 - $750K home sold "(Z) Less than 500 units or less than 0.5 percent." Anyone targeting Rosenberg's statement is making a mountain out of a molehill. Let me put it this way "There was a statistically irrelevant number of new home sales above $750K, somewhere between zero and 500". This is not worth the amount of attention it has received. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |