Mish's Global Economic Trend Analysis |

- Epidemic of Thrift vs. Leap of Faith; Housing Slide Will Seal Recession Fate

- Commercial Real Estate Foreclosures to Hit Chicago "Loop", First Since 1999; Big Wave of Commercial Foreclosures, Bank Failures Coming

- Benevolence by JPMorgan? "JPMorgan Offers us a Chance to Refinance at 4% with No Closing Costs" What's Going On?

- 3rd Quarter GDP Likely Negative, Recession Never Ended

| Epidemic of Thrift vs. Leap of Faith; Housing Slide Will Seal Recession Fate Posted: 23 Aug 2010 07:13 PM PDT I am reasonably certain that the economy is still in recession. If not (and this is ultimately up to the NBER to decide), the pending disaster in housing and commercial real estate will seal the double-dip deal. Either way, the prognosis is not good, as economic conditions are deteriorating rapidly. With that thought in mind, please consider Housing Slide in U.S. May Drag Economy Into Recession "If foreclosures continue to mount and depress home prices, that could send the economy back into a recession," said Celia Chen, an economist who tracks the industry for Moody's Analytics Inc. "The housing market and the broader economy are closely intertwined."Epidemic of Thrift vs. Leap of Faith Nariman Behravesh, chief economist at IHS Inc. in Lexington, Massachusetts correctly says there "There is an epidemic of thrift". Indeed there is, and actually it is a good thing! Consumers need to deleverage and they are. Unfortunately Behravesh blows it with "Sometime in the next 6 to 12 months, we'll start to see more movement on home and car purchases and greater willingness on the part of businesses to hire." Excuse me for asking but ... Small Businesses are Not Hiring - Why Should They? As is typical of most economists, Behravesh displays an amazing and unwarranted leap of faith. Structurally High Unemployment for a Decade Guy Lebas, chief fixed-income strategist at Janney Montgomery Scott LLC has it correct: It will take a "very, very long-term process" to fix this mess. Consumer demand is dead. That demand is not coming back anytime soon, and there is no driver for jobs if it doesn't. Unemployment and GDP will both be extremely weak for the duration. Harsh Reality From Bernanke In the Incredible Shrinking Boomer Economy I noted a harsh reality quote of Bernanke: "It takes GDP growth of about 2.5 percent to keep the jobless rate constant. But the Fed expects growth of only about 1 percent in the last six months of the year. So that's not enough to bring down the unemployment rate." I wrote that in July of 2009. Nothing has changed. Indeed, 3rd Quarter GDP Likely Negative, Recession Never Ended Pray tell what happens if GDP can't exceed 2.5% for a couple of years? What about a decade (or on and off for a decade)? If you have come to the conclusion that we are going to have structurally high unemployment for a decade, you have come to the right conclusion. Ask yourself: Is that what the stock market is priced for? Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 23 Aug 2010 12:31 PM PDT With office space selling 30% below the 2007 high in the top-10 US office markets, and with lease rates still falling, one should expect to see more foreclosures in major cities. Chicago is about to be hit says Crain's Chicago Business in Office tower at 500 W. Monroe flirts with foreclosure — again A Georgia firm that holds two junior mortgages on the 46-story tower at 500 W. Monroe St. says the building's loans went unpaid when they came due this month and that the company may foreclose and take control of the property.Big Wave of Commercial Foreclosures Coming Bernanke's stimulus efforts did next to nothing for residential housing, and absolutely nothing for commercial real estate. With a wave of maturities coming due, and with lease prices still dropping, pressures on commercial real estate are enormous. Moreover, it is crystal clear that the economy is headed back towards recession, assuming of course one believes the recession that started in 2007 ever ended. I suggest the recession never ended in light of the fact 3rd Quarter GDP Likely Negative. How much patience lenders have in a weakening economic environment to restructure loans remains to be seen, but surely it isn't infinite. Big Wave of Bank Failures Coming Given that regional banks are in general the ones with the most commercial real estate exposure, it should not be too difficult to look one step ahead and see the effects of another economic downturn on mid-sized banks. Recovery a "Statistical Mirage" Brace yourself because the recovery of 2009 was nothing but a statistical mirage fueled by unsustainable government spending and bank bailouts. That mirage is rapidly fading off into the sunset. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 23 Aug 2010 09:08 AM PDT Reader "Michele" received a notice from JPMorgan Chase out of the blue, offering to lower her 4.75% mortgage to 4.00%. Chase will waive closing costs. Michele Writes ... Hi Mish,Benevolence by JPMorgan? Hello Michele In spite of the wording of that letter rest assured that JPMorgan Chase has its best interest at heart not yours. However, it just so happens it is quite possible its best interest and yours are aligned. What's Happenin'?

While it may be a good deal for you, the offer has nothing to do with their McDonald's like statement implying "you deserve a break today". The driving force is what is in the best interest of JPMorgan. Low Mortgage Rates Spur Refinance Boom FreeRateUpdate reports Mortgage Rates Spurring Refinance, but Some Banks are Underwriting Too Slow With the current mortgage rates at 4.00% for a 30 year fixed, 3.50% for a 15 year fixed and 3.25% for a 5/1 ARM, home owners are now taking the plunge to refinance. Many have been just watching the market to see what was going to happen and are now making their move. Since rates have reached historical lows not seen since the 1950s, the refinance door has opened up for everyone. Even those who already enjoy low rate mortgages are eager to apply for a refinance. Mortgage rates may be spurring refinance, but some banks are underwriting too slow to get loans closed.It's highly likely JPMorgan Chase knows Michele has no "glitches" and that it is a matter of time before she refinances. To keep the loan, JPMorhan sends a "Benevolent Letter". How Credit Scores Affect Refinancing Jim Gallagher at the St. Louis Post Dispatch writes Refinancing mortgage now may be timely idea Mortgage rates hit yet another new low this week — 4.42 percent on a 30-year loan. That's the lowest since Freddie Mac began keeping track in 1971.I do not know where mortgage rates are going, but the consensus the economy is going to pick up steam is foolish. The odds are we will not see a double-dip recession for the simple reason we are still in one. Nearly every economic indicator is headed lower.

Moreover Small Businesses are Not Hiring - Why Should They? Gallagher continues ... If you're eligible to refinance, consider yourself lucky. "You can be the perfect borrower, but you won't qualify to refinance because the neighbor next door went into foreclosure and the house sold for 50 cents on the dollar," says Doug Schukar, CEO of USA Mortgage, one of the largest mortgage banking operations in St. Louis.The one thing I would caution Michele on is the waiver of closing costs. Does it really mean all costs? With no points? Others may disagree, but I like "no points, no fee loans" for the simple reason if rates drop again, you can refinance again without penalty. Addendum: "JH" Writes ... I'd be interested in knowing if JP Chase's offer is to re-fi the entire ORIGINAL loan balance, or just the remaining. If Michele is paying down principal, JPM is seeing less and less actual interest each month on the loan (especially true on a 15yr am), so I'd not be surprised for a loan offered to "start over" the amortization schedule on a new loan for the ORIG amount, thereby maximizing JPM's interest income.Reply: I am pretty certain that JPMorgan Chase would not be doing what you suggest. It would add risk to JPMorgan while giving cash back to Michele. Even if that were the case, Michele could simply take the cash back, and apply it to the new loan, which I believe she would do. Nonetheless, there is a trap of sorts given Michele may only have 10 years left (or 8 or whatever because of the extra payments), and now she is back in a 15-year loan. However, Michele seems disciplined enough to make extra payments. She can easily keep making her current payment (with extras). Assuming Michele has a year's worth of living expenses in an emergency fund in cash, I would suggest she continue to do just that. In that sense, nothing has changed but the lower rate. However, in an emergency she also has the flexibility to make the lower payments. This is an advantage to someone with discipline like Michele. For someone without discipline, it can resort in more interest being paid than their original plan. Addendum II: Michele writes .... I called the Chase representative handling our case, and he assured me that, "even though it seems unbelievable, Chase is covering all closing costs. There will be absolutely no closing costs for us. And, no points." I will get back to you if any hidden costs pop up when we get our first statement on the new refinance loan.Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

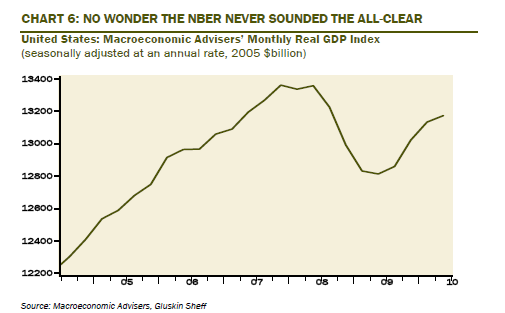

| 3rd Quarter GDP Likely Negative, Recession Never Ended Posted: 23 Aug 2010 01:54 AM PDT While some people still think the odds of a double dip recession are close to zero, ironically, the only reason they may be right is if the first dip never ended. Please consider last Friday's Breakfast With Dave, wherein Rosenberg stated U.S. RECESSION NEVER ENDED; GDP TO CONTRACT IN Q3 Our suspicions have been confirmed — the recession never ended. Macroeconomic Advisers produces a monthly U.S. real GDP series and it shows that the peak was in April, as we expected, with both May and June down 0.4% in the worst back-to-back performance since the economy was crying Uncle! back in the depths of despair in September-October 2008.How Likely is a Double Dip? Flashback June 25, 2010: ECRI Weekly Leading Indicators at Negative 6.9; How Likely is a Double Dip? Inventory restocking contributed 1.88 of the reported 2.7 [first quarter annualized GDP].Flashback August 15, 2010: ECRI WLI "Flattens Out" at -9.8% - ECRI says "Gage is Fine" I actually have the odds of a double-dip recession falling quite rapidly. Why? Because it is increasingly likely the recession that started in 2007 never ended.Second quarter GDP will likely be revised way lower to 1.1% or so. Unless things improve, 3rd quarter GDP will contract. Amazingly, economists are still clinging to estimates of 2.5% and up. So expect to discover the vast majority of economists will be surprised at the forthcoming downward revisions, even after we point these things out well in advance and repeat them. Surprise, Surprise, Surprise Recent Surprises

The ECRI is still touting the "flattening" of the Weekly Leading Indicators (WLI) at -10. With the collapse in treasury yields, a print of -500,000 on weekly claims, and a god-awful Philly Fed report, let's watch the next few weeks. I suspect this "flattening" period will soon be over. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment