Mish's Global Economic Trend Analysis |

- Hawaii Furloughs Its Children; Extreme City Moves; Who Is To Blame?

- Financial Reform Act Requires 67 Studies and 243 New Rules Not Yet Created

- Fooled by Stimulus - Structural Problems Still Intact

| Hawaii Furloughs Its Children; Extreme City Moves; Who Is To Blame? Posted: 09 Aug 2010 06:30 PM PDT Cities and states are running out of cash. In response Governments Go to Extremes as the Downturn Wears On. Here are few examples from the article. Hawaii Furloughs Its ChildrenCommon Themes One thing these stories all have in common is public unions and high public union costs. There did not need to be police layoffs in Colorado Springs, nor does there need to be teacher furloughs in Hawaii. To save jobs and services, all the unions had to do is agree to lower salaries and benefits. But the unions won't do it. In response, cities like Colorado Springs should outsource their police departments to the local sheriffs' association. They should also outsource every other city service as well, all to the low cost bidder. The city's reaction was to stop collecting trash in its parks. Such actions are tantamount to blackmail, hoping to get voters to approve tax hikes. Who Is To Blame? Corrupt politicians willing to buy union votes in conjunction with corrupt unions willing to bribe politicians are the primary parties to blame. However, lazy voters do not get off scot-free. Voters can and should act responsibly. This puts the ball back in the voter's court. In general terms, not just in relation to Colorado Springs, the correct response from citizens should be to get rid of the mayor and any council members who are unwilling to take on the real problem confronting the city: police and firefighter wages and benefits. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Financial Reform Act Requires 67 Studies and 243 New Rules Not Yet Created Posted: 09 Aug 2010 11:11 AM PDT Previously I did a tongue-in-cheek post claiming that the Financial Reform Bill was a Stunning Success given that it accomplished virtually nothing while doing no further major economic damage. Today I see I was overly optimistic (which as regular readers know is simply part of my nature). There are 67 Studies and 243 New Rules that still need to be done, and Lord only knows what kind of damage those will entail. Please consider Crash of 2015 Won't Wait for Regulators to Rein In Wall Street The financial system experiences a crisis "every five to seven years," JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon told the Financial Crisis Inquiry Commission in January. By that measure, the next crash could come by 2015 -- years before new banking reforms are in place.Note the line about padding bank profits before there is any reform. Think those reported bank earnings were real? JPMorgan Chief Executive Officer Jamie Dimon is highly likely correct about another financial crisis before 2015. If so, expect JPMorgan's derivatives unit to be smack in the middle of it. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Fooled by Stimulus - Structural Problems Still Intact Posted: 09 Aug 2010 12:20 AM PDT Bill Watkins, a California Lutheran University professor, provides a nice summary on New Geography of the failure of various stimulus efforts to do anything meaningful in the wake of a collapse by Lehman, a collapse he says is a "regime shift". Please consider Flexible Forecasting: Looking for the Next Economic Model by Bill Watkins. The world changed in September 2008. We call it a regime shift. It's a move from one (good) equilibrium to another (bad) equilibrium. Statistical models that worked well in the old regime don't work in the new regime. We hustled to adjust our models, but admitted that with limited experience in the new regime, we were less confident in our forecasts.Massive Policy Errors Bill Watkins discusses many of the things I have been talking about on this blog for years. Nonetheless, I thank him for a nice summary of why stimulus failed and also for recognizing that stimulus measures would fail in advance. Policy errors certainly have been rampant and very few economists saw them. Watkins thinks economists now understand the "regime shift". More than likely, most of them don't. Instead, economists have a tendency to project current economic status forward, without understanding why. Because things have slowed down, economists became a more realistic. I doubt their understanding is much better. If there is another round of stimulus accompanied by another uptick in the economy (the former is likely coming but probably not the latter), I have no doubt economists would think we are off to the races again and this was just another "soft patch". In contrast, I propose we are going to flirt in and out of recession for perhaps a decade, just as Japan did. Interestingly, every time the Japanese economy rebounded slightly, economists thought "thank God, deflation is over", only to see the Japanese economy relapse. Problems Many, Solutions Nonexistent

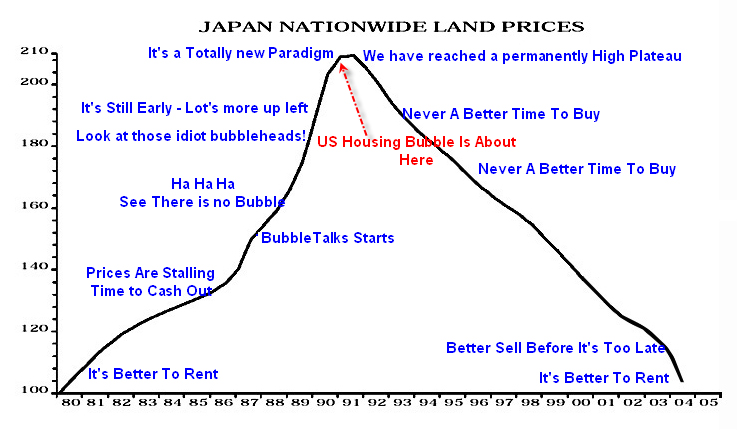

Regime Shift? What? When? Lehman filed bankruptcy in September of 2008. For comparison purposes, I started posting on the phenomenon of people Walking Away from their houses in January of 2008. Here are some Links to Walking Away articles. What is the real regime change: People willing to walk away from their homes for the first time in history, or the bankruptcy of a single company? That people would voluntarily walk away from their homes is without a doubt a "game changer". It turned economic theory 180 degrees. Almost no one thought that would happen. In contrast, nothing especially important changed in September of 2008. That Lehman would file bankruptcy is at best a symptom of attitudes that had long since changed. It's a Totally New Paradigm Secular attitude changes like "walking away" had their roots in the busting of the housing bubble. Flashback Saturday, March 26, 2005: It's a Totally New Paradigm Here are some links to the housing bubble chart updates, all made in real time. One of my favorite updates of that chart regards the cover of Time Magazine going "gaga" over real estate one year after the bubble burst, but before anyone important even recognized that fact. Inquiring minds may wish to consider US vs. Japan Land Prices Pictorial Update for a discussion of Time Magazine going "gaga". They even used the word "gaga" on the cover. Regime Change Started in 2005 The regime change that Bill Watkins mentions, actually began in 2005 with the busting of the housing bubble. It took a couple more years before economists noticed because commercial real estate kept the game going for a while longer. Commercial real estate follows residential housing with a lag, and from 2005-2007 stores like Home Depot, Lowes, Walmart, Pizza Hut, were still in rampant expansion. That expansion provided enough jobs to mask what consumers finally started figuring out: "home prices will not rise forever". Nonetheless, Bill Watkins is actually ahead of the game in understanding there was a regime change. In 2008 Ben Bernanke was still in denial over the housing bubble and he had amazingly optimistic ideas where the unemployment rate was headed. Even now, Bernanke displays little public awareness of what is going on. It would be interesting to hear what he says in private at the FOMC meetings in comparison to the soundbites the Fed delivers to the public. If FOMC soundbites represent what the man really thinks, Bernanke is nearly as clueless as ever, with little understanding of what went wrong or why, what the policy errors were, and what the Fed's role in this mess was. Attitudes are the Game Changer Watkins missed when the regime change occurred and possibly what the regime change even is (changing social attitudes on housing, consumption, risk taking, and debt, by consumers and banks alike). The "attitude change" was the game-changer, NOT the event (the collapse of Lehman). Nonetheless, Watkins is light-years ahead of most economists and economic cheerleaders in understanding that we did have had a massive regime change, that the regime change is lasting, and that stimulus efforts to date have done nothing to fix the structural problems at hand. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment