India has come up with the world's cheapest "laptop," a touch-screen computing device that costs $35. India's Human Resource Development Minister Kapil Sibal this week unveiled the low-cost computing device that is designed for students, saying his department had started talks with global manufacturers to start mass production.

"We have reached a (developmental) stage that today, the motherboard, its chip, the processing, connectivity, all of them cumulatively cost around $35, including memory, display, everything," he told a news conference.

He said the touchscreen gadget was packed with Internet browsers, PDF reader and video conferencing facilities but its hardware was created with sufficient flexibility to incorporate new components according to user requirement.

Quel, as they say, surprise! Aluminum Co. of America kicked off the second-quarter earnings season after the markets closed Monday by beating analysts' consensus earnings expectations. Alcoa, which is traditionally the first Dow stock to report, had a profit of 13¢ a share versus forecasts of 11¢.

Then, on Tuesday, Intel Corp., the leading maker of computer chips, also beat expectations, with profit coming in at 51¢ a share versus analysts' forecasts of 43¢. Quel surprise!

Yes, it's the summer earnings derby, whereby the markets pretend to be surprised by companies beating the consensus forecasts, which, by tacit agreement, have been lowballed. The companies give guidance that is conservative. The analysts willingly concur, rolling over and playing dumb.

In the parlance of the Street, it's "grooming." Companies find no advantage in putting themselves out to guide rigorously and precisely; analysts find no advantage in bucking that guidance. It's a convenient dance, a little two-step that works.

Just as companies pretend to offer guidance with a straight face and analysts concur with a nod and a wink, we in the cheap seats must watch the performance in the knowledge it's merely an act. The so-called "whisper" estimates — what the Street really expects — becomes a loud prompting from stage left, theatre of the absurd.

The first-quarter earnings "beat" rate for S&P 500 index was 73%, one of the top "surprise" levels in the past 10 years. But recent beat-analyst-expectations rates have all been near the 70% mark.

If economics is the dismal science, what ironic description does fundamental analysis deserve? Of course, securities analysts can hide in the consensus pack. And, of course, an analyst does himself and his firm no real favour by going out on a limb and going against the crowd. You can be wrong with the rest and not be punished. You cannot be wrong against the rest.

China's banks are facing serious default risks on more than one-fifth of the Rmb7,700bn ($1,135bn) they have lent to local governments across the country, according to senior Chinese officials.

In a preliminary self-assessment carried out at the request of the country's regulator, China's commercial banks have identified about Rmb1,550bn in questionable loans to local government financing vehicles – which are mostly used to fund regional infrastructure projects.

Local governments had, until recently, been on a construction spree on orders from Beijing to prop up the economy in the face of the financial crisis. However, since the start of this year, top Chinese bankers and regulators have been warning that many of the loans used to fund infrastructure spending and a property boom could go bad.

Chinese banks lent a record Rmb9,600bn last year – more than double the new loans issued in 2008. But stern warnings by regulators for the banks to slow down lending appear to be having an effect on the economy. The regulator ordered a stop to this type of lending at the start of the month.

Among the lessons from earnings season so far: Now is not the time for optimistic CEOs to tell skittish investors an expansion push is right around the corner.

In a sign that the shell shock from the financial crisis, recession and European sovereign-debt mess hasn't worn off, investors last week punished the stocks of companies that are talking openly about plans to expand.

Delta Air Lines executives spent much of an earnings conference call Monday parrying with analysts over the airline's plans to increase capacity by 1% to 3% in 2011, on top of this year's growth of 1% to 1.5%. Delta Chief Executive Richard Anderson said Delta is committed to "capacity restraint," but the stock fell 2.9% that day. The shares lost 2.3% for the week, compared with a 5.4% gain by the NYSE Arca Airline index.

In contrast, the kinder, gentler approach to production capacity went over much better. Harley-Davidson shares jumped more than 13% on Tuesday after the motorcycle maker announced rosy quarterly results and noted its plans to cut shipments by 5% to 10% in 2010.

On Monday, Texas Instruments CEO Rich Templeton pointed to the chip maker's "steady investments in production capacity," saying they were allowing the company "to meet higher demand levels from customers."

The comments and mildly disappointing quarterly revenue pushed the stock down more than 3% Tuesday, though the shares finished the week up 2.5%. Some analysts worried that the expansion could come back to haunt Texas Instruments if the economy softens. The company stressed that prices it has been paying for additional capacity have been good deals, reducing any potential downside risk.

United Airlines parent UAL Corp. got a pat on the back from analysts for its plans to keep capacity additions relatively muted. Its shares jumped 4.8% on Tuesday after UAL released earnings.

Companies for the most part do not want to expand and are instead hoarding cash while outsourcing everything they can to Asia. Pray tell, where is job growth going to come from?

Pity the programmers toiling away at Wall Street's secretive high-frequency trading shops--places like Goldman Sachs ( GS - news - people ), Citadel and Getco. They wrote algorithms that take advantage of fleeting trading opportunities and bring in up to $100,000 a day. In return, they received a fraction of the pay doled out to their bosses.

Now some programmers feel used and are instigating a revolt. They are doing so by striking out on their own or forming profit-sharing arrangements. Jeffrey Gomberg, 32, worked for a trading firm that paid him a low-six-figure income after four years on the job. His trader colleagues, by contrast, made millions manipulating the algorithms he'd written.

Last year Gomberg and a fellow programmer quit their jobs and cut a deal with HTG Capital Partners of Chicago, whose programmers typically trade on regulated futures exchanges. HTG supplies office space, technology and access to exchanges. Gomberg keeps 40% to 80% of net profits, with the percentage rising as his profits do. More importantly, says Gomberg, the programmers retain ownership of the code they write.

"We designed this deal so we wouldn't lose intellectual property," he says. "If it doesn't work out, we can go somewhere else and take all the software [that we developed]. That's really the key."

Another high-frequency programmer, who spoke on condition that his name not be used, quit two firms that he believed were underpaying him. He says one group was generating $100,000 a day from his high-frequency trading software and paying him $150,000 a year. "I'm on my way to making a ton," he says.

Given that HFT programs put out offers that are not legitimate (thus constituting fraud), I fail to see why HFT should not be banned. Thus not only is HFT not needed, neither are the HFT programmers.

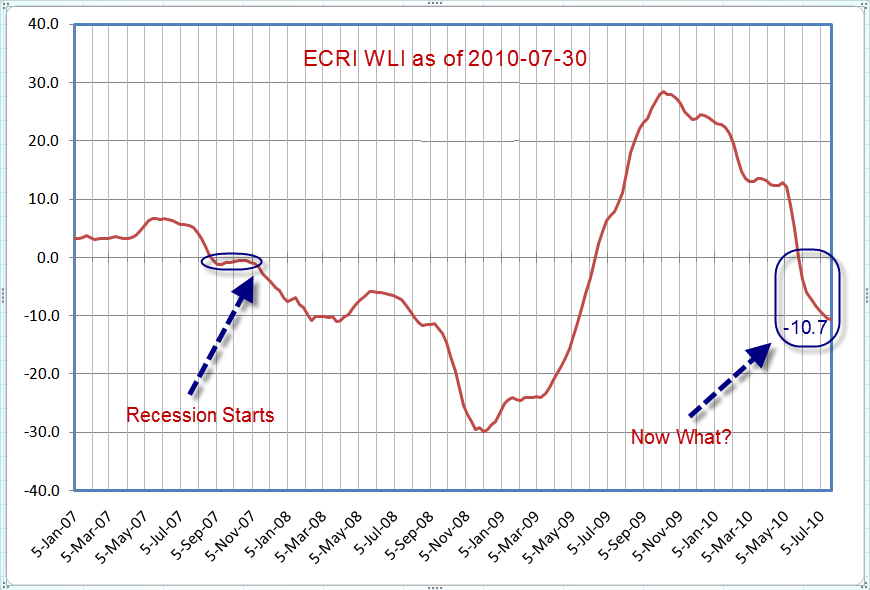

The ECRI's Weekly Leading Indicators (WLI) has now fallen 8 consecutive weeks and has been below -10 for two consecutive weeks.

click on chart for sharper image

Given the July bounce in the stock market, the ever-optimistic me expected some sort of anemic bounce in the WLI as well, but that bounce never came. Of course, it would be helpful to know the makeup of WLI (components and percentages), but unfortunately that information is proprietary.

Nonetheless, we can say there has never been a WLI plunge in history of this depth and duration, nor any dip at all below -10 that has not been associated with a recession.

Whatever the ECRI sees preventing them from issuing a recession alert remains a mystery.

However, in light of today's GDP report sporting 3 Years of Massive Downward GDP Revisions it is becoming increasingly likely that the recession that started in 2007 never ended.

When it comes to the perfect playing golf vacation spots in Ireland, the Southwest area is riddled with incredible playing golf courses filled with great links and stunning views. In these parts you will see Ireland’s most sought after playing golf program all eager to line up for some tee time, the Ballybunion Club, especially its aged course.

Many well-liked names on the planet of playing golf have experienced the wondrous allure of Ballybunion and also have continually used it like a warm up course to unwind and relax before The Open. Names like Jack Nicklaus, Nick Faldo, Tiger Woods and Tom Watson has registered in its log book and has supplied excellent reviews and comments to this wondrous and mesmerizing sell timeshare for cash.

Being the millennium captain from the Ballybunion Golf club, Tom Watson said that it is one of the best and most stunning tests of hyperlinks he has played in, having played there since 1981.

Right here within the old golf course, you’ll find really challenging hyperlinks where the winds are continuous factors and the land is surrounded through the captivating view from the Atlantic.

Opened in August 18, 1893, the Ballybunion Golf club has had its shares of ups and downs. In its early days, the Ballybunion Club didn’t appreciate the popularity it does these days and has fallen into monetary oblivion. Its first 8 years reeled the program to its all time low and was quickly revived only through the changing from the officers from the club.

As much more developments and land hyperlinks were laid out, the reputation from the Ballybunion Club grew and grew. By 1926, the course had strategies to extend to a complete 18 holes, barely a year after, those strategies had been realized. Its national level of recognition started in 1932 once the Irish Ladies Championship was held there. Five years following, Irish Mens Close Amateur Championship followed suit.

Its very first most significant level of competition came at 1957 once the program was selected as the venue for that Irish Expert Championship. Soon after, waves of other competitions and golf organizations recognized its high quality hyperlinks and also have given it higher accolades.

After more than 60 many years, the Ballybunion Golf club finally got the recognition it so rightly deserves and things were never quite exactly the same. Golfers now come in droves from all over the earth to encounter what the lucky Irish people have had for more than a century now. The Ballybunion Golf club would usually be acknowledged as Ireland’s greatest golf vacationing spot.

But apart from its majestic and incredible rolling dunes, and the mesmerizing backdrop set through the Atlantic Ocean, the tradition and culture which has created Ballybunion Golf club what it’s today is what keeps the people coming in.

Plus, it has world class amenities that may cater towards the needs of so numerous golfers from all more than the earth. There you’d discover sell my timeshare now built clubhouse which has a dining room that may seat 120 persons, two bars and some really relaxing lounge areas. There is also a Pro Golf Shop that carries each and every golfing requirements that you might have. Also, becoming a championship playing golf program, you will be capable to find some practice facilities for example; Placing Greens, A Sand Bunker Exercise facility, Driving Variety, and a Chipping Green.

Ballybunion Club is situated at Sandhill Road., Ballybunion, Nation Kerry, Ireland. For the greatest golf holiday spot in Ireland, this is a century old choice for the pros.

Mortgages go back a longtime, in fact they begun in England way back in 1190 and were regarded as a conditional sale able to be repossessed in the event of failure of payment.

Nowadays, nothing much has changed, in so far as the banks or credit company will indeed take your home if you fail to keep up with the monthly repayments.

What has changed however, is the numerous types of mortgages available to you, and both first time buyers and re-investors, can be overwhelmed and at times, confused by the offers put to them.

Therefore, when applying for a mortgage ensure you understand all the terms and conditions involved with the mortgage and be certain to opt for the best mortgage deal appropriate to your circumstances.

You could decide on a fixed mortgage where the mortgage rate is fixed at a certain rate for a certain amount of time. This is beneficial to many people as they know for instance, how much their monthly outgoings will be for the next two years say. Variable mortgages are also common as are tracker mortgages.

When deciding on a mortgage it is vital to consult a mortgage advisor, either independently or through your current bank. Detail your current outgoings and expenditure and work out how much mortgage repayments will be on certain amounts of borrowing. It’s very important that you do not over borrow as failure of meeting monthly repayments will result in the repossession of your house.

A qualified mortgage consultant will advise you on what mortgage deal is right for you based on your private and economic circumstances so ensure you provide all relevant information and paperwork regarding any incomes.

More recently you are also able to re-mortgage your home (basically borrow more money against it) for home improvements, for example or indeed other investment opportunities.

This week Max Keiser and co-host Stacy Herbert look at the scandals of Brown’s Bottom, the worst economic judgment of all time and Bono’s private equity, “the worst investor in America.” Max chats to Brits in Trafalgar Square and also talks to Mark Schapiro, author of the Harper’s article, “Conning the Climate: Inside the Carbon Trading Shell Game”.

Quicken Loans client Carrie from Missouri, discusses in this video review how Quicken Loans and Dana Staniec, her mortgage banker, helped her and her family with their relocation. Carrie’s husband was being relocated and had to beginning working at his new location in 30 days and needed to reside there in 45 days. Carrie’s husband’s work gave them a great relocation package which included two companies as options to work with, Quicken Loans being one of them. Carrie called Quicken Loans first and new instantly after talking with Dana Staniec, that Quicken Loans was who she wanted to work with. Dana was very professional, friendly and knowledgeable. She helped Carrie throughout the entire mortgage process. Carrie loved that the entire process was online because it made the process extremely fast, especially since they had to be in their home in 45 days. Carrie and her husband recommend Quicken Loans to anyone looking to purchase a home or refinance.

A payday loan is a short and convenient way to make an emergency payment. Most do not require a credit check, are fast and require only a few steps to apply. Any individual with a serious financial emergency can consider this option to provide the necessary relief. Borrowers are able to extend their monthly budget in case something unexpected occurs. People can avoid expensive overdraft or late payment fees during times of emergency or crisis with taking out a small amount of money and then paying it back within two weeks. To qualify, the applicant needs to provide proof of employment, personal identification, and evidence of an active checking account. Compared to other types of borrowing, this is a relatively quick and basic process, allowing for budget issues to be resolved efficiently.

Acquisitions are possible either online or in-store. Online accounts directly deposit the money into a checking account the next business day. For repayment, the lender simply makes an electronic withdrawal. Eventhough in store payday loans are in existence in many cities, making an application online with the help of the internet has been a more popular option. Borrowing in-store could be a great option for someone in need of money right away, because of an urgent situation. All that is needed is the appropriate information and a post-dated check to make sure that the person borrowing money is able to repay the amount on time.

Benefits of the in-store process include immediate payment upon approval without having to wait one business day. When the time comes for repayment, most lenders can simply go to the bank and cash a post-dated check provided at the time of application.In-store services cater to the most time sensitive situations. In providing the right information and a check written to be cashed at the agreed upon date, the borrower is insuring their financial credibility by paying their regular bills before the due date.There are several factors involved in deciding to apply for a short-term solution to emergency situations. Many families struggle through severe vehicle damages or hospital visits that create financial risk. Often time, a short term solution may be what is needed to resolve these tragedies.

A lot of instant payday loans have an interest rate and this should certainly not be not considered prior to applying. A common complaint is the high annual percentage rate. Although this interest charge is expensive, when compared to other financial setbacks such as over limit and returned payment charges, it is in reality the most responsible solution for someone in need of help. Something as basic as reconnection charges can carry an unreasonable percentage rate, thus enforcing the trustworthiness of a quick and safe option that is temporary.

In urgent situations, time becomes a crucial precedent in making decisions that best resolve the problem. Anyone interested should consider the reality of his or her financial situation before taking out a loan. Payday loans are able to meet a wide variety of financial needs, and provide help to those looking for some breathing room when bills begin to be too much to handle.

10pts to best answer. Question about auto insurance policies?

I just earned my drivers liscence. My father is dreading the cost of adding another driver to the family auto insurance policy. What are some discounts that many insurance companies offer that might help save my dad some money when the premium is due?

The BEA has finally admitted something anyone with a modicum of common sense already knew: The recession was far deeper and the "recovery" far weaker than previously reported.

Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- increased at an annual rate of 2.4 percent in the second quarter of 2010, (that is, from the first quarter to the second quarter), according to the "advance" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP increased 3.7 percent.

The real story in the report was not the continuing ratcheting down of GDP forward estimates, but rather massive backward revisions, most of them negative, dating back three full years.

Revision Lowlights

For 2006-2009, real GDP decreased at an average annual rate of 0.2 percent; in the previously published estimates, the growth rate of real GDP was 0.0 percent. From the fourth quarter of 2006 to the first quarter of 2010, real GDP increased at an average annual rate of 0.2 percent; in the previously published estimates, real GDP had increased at an average annual rate of 0.4 percent.

For the revision period, the change in real GDP was revised down for all 3 years: 0.2 percentage point for 2007, 0.4 percentage point for 2008, and 0.2 percentage point for 2009.

For the revision period, national income was revised down for all 3 years: 0.4 percent for 2007, 0.6 percent for 2008, and 0.4 percent for 2009.

For the revision period, corporate profits was revised down for all 3 years: 2.0 percent for 2007, 7.2 percent for 2008, and 3.9 percent for 2009.

For 2007, the largest contributors to the revision to real GDP growth were a downward revision to PCE, an upward revision to imports, and a downward revision to state and local government spending;

The percent change from fourth quarter to fourth quarter in real GDP was revised down from 2.5 percent to 2.3 percent for 2007, was revised down from a decrease of 1.9 percent to a decrease of 2.8 percent for 2008, and was revised up from an increase of 0.1 percent to an increase of 0.2 percent for 2009.

National income was revised down for all 3 years: $51.8 billion, or 0.4 percent, for 2007; $77.4 billion, or 0.6 percent, for 2008; and $55.0 billion, or 0.4 percent, for 2009. For 2007, downward revisions to corporate profits and to supplements to wages and salaries were partly offset by an upward revision to wages and salaries.

Personal outlays -- PCE, personal interest payments, and personal current transfer payments -- was revised down for all 3 years: $15.4 billion for 2007, $15.0 billion for 2008, and $79.1 billion for 2009. For all 3 years, downward revisions to PCE more than accounted for the revisions to personal outlays. The personal saving rate (personal saving as a percentage of DPI) was revised up for all 3 years: from 1.7 percent to 2.1 percent for 2007, from 2.7 percent to 4.1 percent for 2008, and from 4.2 percent to 5.9 percent for 2009.

Inventory Rebuilding Runs Its Course

There are pages of revisions, that is just a sample. One of the key findings in the report concerns inventory rebuilding. Dave Rosenberg discusses inventories and the GDP in general in Slow Motion Recovery.

The big story in the second quarter as has been the case for much of the past year was the contribution from inventories – there was a "build" of $75.7 billion and this added over a percentage point to headline GDP growth. This follows a "build" of $44 billion in the first quarter so this is no longer the case that companies are merely reducing the pace of inventory withdrawal. Businesses actually added to their stockpiles at the fastest rate in five years. And with sales lagging behind, this inventory contribution is likely to fade fast in coming quarters. Real final sales – representing the rest of GDP (excluding inventories) – came in at a paltry 1.3% annual rate last quarter and has averaged 1.2% since the economy hit rock bottom a year ago in what is clearly the weakest revival in recorded history.

Normally, real final sales are expanding at closer to a 4% annual rate in the year after a recession officially ends. Then again, we haven't heard anything official just yet about the one that began in December 2007 – and so the fact that it is averaging at around one-third that typical pace in the face of unprecedented policy stimulus is rather telling. And frightening.

Looking at the components of GDP, it appears as though the economy is set to slow even further and a flattening in Q3 and perhaps even contraction by Q4, barring some positive exogenous shock, cannot be ruled out.

If indeed, the inventory cycle is behind us, then what we have on our hands is an underlying baseline trend in GDP of 1.2% at an annual rate. And if we are correct in our assumption that the looming withdrawal of fiscal stimulus at the federal level and the cutbacks at the state and local government level subtract 1.5% from growth in the coming year, then it begs the question: How exactly does the economy escape a renewed moderate contraction over the next four to six quarters, barring some unforeseen positive boost? In turn, how does a strong possibility of such a contraction square with consensus views of a 35% surge in corporate profits to new record highs as early as next year? The answers to these questions are as painful as they are obvious.

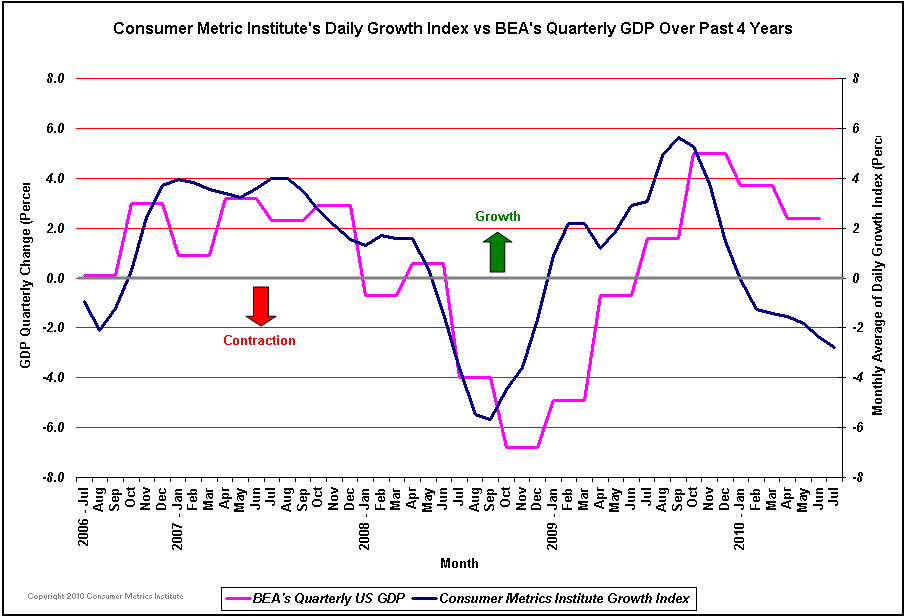

Consumer Metrics Institute Looks Inside the New GDP Numbers

Rick Davis at Consumer Metrics Institute (CMI) has been calling for this slowdown and these revisions in advance. Please consider Inside the New GDP Numbers

The 2.4% figure will garner all of the headlines, but the more important "real final sales of domestic product" continues to be weak, growing at a reported 1.3% annualized rate. The real cause for concern is that the reported inventory adjustments dropped from a 2.64% component in the revised 1st quarter to a 1.05% component during the 2nd quarter. If factories have begun to realize that end user demand remains anemic, the inventory adjustments could well go negative soon, pulling the reported total GDP down with it.

The BEA revised much more than the first quarter of 2010. They revised down 2009, 2008 and 2007 as well. Apparently the "Great Recession" has been worse than our government has previously reported.

The new GDP report shows that the current gap between the consumer demand that we measure and the BEA's reported number continues to grow as factories build their inventories in anticipation of a strong recovery. If factories curb their enthusiasm during the third quarter, the BEA's "advance" estimate for Q3 2010 might be brutal, just 4 days before the U.S. mid-term election.

The new GDP report shows that the current gap between the consumer demand that we measure and the BEA's reported number continues to grow as factories build their inventories in anticipation of a strong recovery. If factories curb their enthusiasm during the third quarter, the BEA's "advance" estimate for Q3 2010 might be brutal, just 4 days before the U.S. mid-term election.

Consumer Metrics vs. BEA

click on chart to enlarge

The CMI lead the BEA by 1-2 quarters at both the prior bottom and again at the most recent peak. Although the CMI has GDP negative, that is as a result of analyzing consumer spending.

We must factor in massive government stimulus that did literally no good, but it did add to GDP.

No matter how useless, government spending is always considered productive. Thus I was certain that GDP would not come in negative this quarter. However, I am equally certain Consumer Metrics has the weakening trend correct.

Unless there is another round of huge government spending, GDP will be headed towards 0% in the 4th quarter.

For a discussion of the parameters Consumer Metrics takes into consideration and how their modeling works, please see my February 26, 2010 post GDP Contraction Coming In Second Quarter 2010?

Where To From Here?

The important point as always is not where we have been, but rather where we are headed. In this regard, note how hopeless the BEA is. We are just now getting revisions as to where we were three full years ago. Looking ahead, everyone listens to Bernanke who not only appears clueless, but has a vested interest to not tell the truth lest it "spook the markets".

However, we do not need Bernanke or the cheerleaders on CNBC to tell us what we need to know, we can open our eyes and see rising foreclosures, no "help wanted signs", a recovery in profits but no real world recovery, and various Obama stimulus measures that have all failed spectacularly, especially home tax credits.

Now that inventory replenishment is nearly over, if not indeed completely over, this economy is headed back into the toilet unless consumer demand picks up.

Real final sales of domestic product -- GDP less change in private inventories -- increased 1.3 percent in the second quarter, compared with an increase of 1.1 percent in the first.

Those anemic numbers are AFTER trillions of dollars of stimulus money had been thrown at it.

Does this sound like Japan to you? It does to me.

Fed's Counterproductive Policies

The Fed wants banks to lend and consumers to spend. St Louis Fed Governor James Bullard ("Bullard the Dullard"), is now proposing QE2, hoping to force down interest rates even more.

Ponder the effect on consumer spending plans. Credit card rates are north of 20%. The savings deposit rate at banks is 1%. Any consumer in his right mind has every incentive to pay down their credit cards and not spend more.

Think about that. Consumers can get effective rates of return on their money by paying off credit cards or other consumer debt and not charging more. Will forcing long-term rates lower change this picture? Of course not. Ironically, it will cause the savings rate to rise (simply by increasing the incentive to pay down debts at much higher interest rates!)

Moreover, forcing down long-term rates will rob those on fixed incomes struggling to make ends meet, thus increasing pressure on bankruptcies and foreclosures. However, it might make gold buyers happy campers as the liquidity attempts to find a home.

In other words, QE2 would be hugely counterproductive to the Fed's desire to spur lending and spending. Those who expect to see massive inflation as a result of Bullard's proposal, simply do not understand the role of collapsing credit in this economic depression.

Every time there is a little blip by China in its purchasing or holding of US treasuries, hyperinflationists come out of the woodwork ranting about the "Nuclear Option" of China dumping treasuries en masse.

Such fears are extremely overblown for several reasons.

1. China's purchasing of US assets is primarily a balance of trade issue. If the US runs a trade deficit, some other countries ruin a trade surplus and thus accumulate dollars. This is purely a mathematical function as I have pointed out many times.

2. If China dumps treasuries for Euro-based assets, oil-based assets, yen-based assets or for that matter anything other than dollar based assets, the problem merely shifts elsewhere and those buyers would have to do something with the dollars such as buying US treasuries or other US assets. This too is purely a mathematical function.

3. If China dumped treasuries it would tend the strengthen the RMB and China has been extremely reluctant to let the RMB appreciate. Indeed, the US is begging China to revalue the RMB upward, but China resists.

While China may make short-term moves in its reserve holdings, the odds of China dumping treasuries or dollars in size is quite remote.

An awful lot of investors and policymakers are frightened by the thought of China's so-called nuclear option. Beijing, according to this argument, can seriously disrupt the USG bond market by dumping Treasury bonds, and it may even do so, either in retaliation for US protectionist measures or in fear that US fiscal policies will undermine the value of their Treasury bond holdings. Policymakers and investors, in this view, need to be very prepared for just such an eventuality.

... the idea that Beijing can and might exercise the "nuclear option" is almost total nonsense.

In fact the real threat to the US economy is not the dumping of USG bonds. On the contrary, in the next two years the US markets are likely to be swamped by a tsunami of foreign capital, and this will have deleterious effects on the US trade deficit, debt levels, and employment. Investors and policymakers should be far more worried that China and other capital exporting countries are trying their hardest to maintain and even increase their capital exports, while the capital importing countries are either going to see capital imports collapse, or are trying desperately to bring them down.

So why not worry about Beijing's "nuclear option"? For a start, unlike you or me the PBoC cannot simply sell Treasury bonds, pocket the cash, and go home. Dollar bills are just as much obligations of the US government as are USG bonds, only that they pay no interest. If the PBoC wants effectively to reduce its holdings of USG bonds it must swap them for something else.

So far, the discussion is purely on mathematical statements of fact. Yet most writers, especially the hyperinflationists, fail to understand simple math.

Should China Dump Dollars For Commodities?

Some want China to dump dollars for commodities and stockpile them. Does this make sense?

Not really, as Pettis explains.

Because of the positive correlation between Chinese growth and commodity prices, stockpiling commodities is a bad balance sheet decision for China.

Why? Because by locking in relatively "cheap" commodities if Chinese growth subsequently surges, or relatively "expensive" commodities if Chinese growth subsequently stalls, it will only exacerbate volatility in China's already incredibly volatile economy.

This exacerbation of volatility is made worse by the widespread suspicion that China has already stockpiled huge amounts of commodities, but the main point is that even if the PBoC were to do this, it does not change anything material. It simply reassigns the problem to commodity exporters, with almost the same net results, because if Brazil, say, sells more iron ore to China, Brazilians now have more dollars, which they must either spend on US imports – thus boosting US employment – or invest in US assets. In this case Brazil simply intermediates the former PBoC purchases of USG bonds.

Finally the PBoC could sell US Treasury bonds and purchase assets in China. This would be most damaging for China because it would mean a drastic reversal in the country's currency regime. The PBoC currently sells huge amounts of renminbi to Chinese exporters in order to keep down the value of its currency. Suddenly to switch strategies and to buy renminbi would cause the value of the renminbi to soar. This would wipe out China's export industry and cause unemployment to surge.

So basically any sharp reduction in China's Treasury bond holdings is likely either to be irrelevant to the US or to cause far more damage to China than to the US. I really don't think we should waste a lot of time worrying about the nuclear option.

The Capital Tsunami

Pettis goes on to argue the real problem is exactly the opposite of what most are ranting about. While I mostly agree with what Pettis has to say, I strongly disagree on one point. Let's tune in.

The problem facing the US and the world is not that China may stop purchasing US Treasury obligations. The problem is exactly the opposite.

The major capital exporting countries – China, Germany, and Japan – are desperate to maintain or even increase their net capital exports, which are simply the flip side of their trade surpluses.

China, for example, is unwilling to allow the renminbi to rise against the dollar because it wants to protect and even increase its trade surplus.

Japan is in a similar position. In Japan, consumption growth has been glacially slow, and any contraction in its trade surplus will lead almost directly to reduced production and higher unemployment, so Japan, too, is eager to maintain capital exports.

Finally Germany, like China, has been reluctant to put into place policies that boost net demand, and in fact the collapse of the euro means that Germany's trade surplus will almost certainly grow. Needless to repeat, if the German trade surplus grows, so must its export of capital.

So who will import capital?

Here the situation is dire. The second largest net importer of capital until now has been the group of highly-indebted trade-deficit countries of Europe – including Spain, Greece, Portugal, and Italy. The Greek crisis has caused a sudden stop to private capital inflows, as investors worry about insolvency, and it is only official lending that has prevented defaults. These countries are unlikely soon to see a resurgence of net capital inflows. The world's second-largest net capital importer, in other words, is about to stop importing capital very suddenly. I discuss this more generally in my May 19 blog entry: Don't misread the trade implications of the euro crisis for China.

This leaves the US. Because it has the largest trade deficit in the world it is also the world's largest net importer of capital. So what will the US do?

At first nothing. As net capital exporters try desperately to maintain or increase their capital exports, and deficit Europe sees net capital imports collapse, the only way the world can achieve balance without a sharp contraction in the capital-exporting countries is if US net capital imports surge. And at first they will surge. Foreigners, in other words, will buy more dollar assets, including USG bonds, than before.

But remember that an increase in net US imports of capital is just the flip side of an increase in the US current account deficit. This means that the US trade deficit will inexorably rise as Germany, Japan and China try to keep up their capital exports and as European capital imports drop.

I have little doubt that as the US trade deficit rises, a lot of finger-wagging analysts will excoriate US households for resuming their spendthrift ways, but of course the decline in US savings and the increase in the US trade deficit will have nothing to do with any change in consumer psychology or cultural behavior. It will be the automatic and necessary consequence of the capital tug-of-war taking place abroad.

Whoa! Stop right there.

Please read that last paragraph again.

While I agree that the math MUST balance, to say that attitudes play no part in the formation of that math is simply wrong.

If consumers decide to stop buying goods from China there is almost nothing China can do about it? Why? Wages!

Factory workers demanding better wages and working conditions are hastening the eventual end of an era of cheap costs that helped make southern coastal China the world's factory floor.

A series of strikes over the past two months have been a rude wakeup call for the many foreign companies that depend on China's low costs to compete overseas, from makers of Christmas trees to manufacturers of gadgets like the iPad.

Where once low-tech factories and scant wages were welcomed in a China eager to escape isolation and poverty, workers are now demanding a bigger share of the profits. Many companies are striving to stay profitable by shifting factories to cheaper areas farther inland or to other developing countries, and a few are even resuming production in the West.

Labor costs have been climbing about 15 percent a year since a 2008 labor contract law that made workers more aware of their rights. Tax preferences for foreign companies ended in 2007. Land, water, energy and shipping costs are on the rise.

In its most recent survey, issued in February, restructuring firm Alix Partners found that overall China was more expensive than Mexico, India, Vietnam, Russia and Romania.

Mexico, in particular, has gained an edge thanks to the North American Free Trade Agreement and fast, inexpensive trucking, says Mike Romeri, an executive with Emptoris, the consulting firm.

Attitudes Are The Key

This has everything to do with attitudes.

If US consumers decide to hold out for lower prices, China will be in an enormous squeeze, unable to cut prices much.

I agree 100% with Pettis that Europe will not pick up the slack. However it is not a mathematical certainty the US will pick up the slack. Perhaps no one picks up the slack. Given the math must balance, pray tell what is stopping a collapse in global trade?

Nothing as far as I can see. It all depends on consumer attitudes. Certainly Bernanke and Congress will do their best efforts to get banks to lend and consumers to spend, it is by no means a certainty the Fed will succeed.

Moreover, given the highly likely dramatic shifts in the next Congress and given the appetite for more stimulus efforts now has nearly dried up, it is problematic at best to suggest Congress will keep consumers happy and spending.

Furthermore, cutbacks in state budgets are just now beginning to severely bite. Those cutbacks have to be factored in unless sugar-daddy Congress steps up to the plate.

While Congress may partially bail out the states, don't count on it, especially in entirety.

Can Global Trade Collapse?

Given that Bernanke has already failed once, and in a big way, why can't he fail again? I suggest he will. Regardless of the outcome (even if Pettis is correct), consumer attitudes towards spending and debt will determine the global trade imbalance math NOT preordained math deciding the role of the US.

The result may be a collapse in global trade, not an inflationary event to say the least.

Dee Williams, who lives in a simple but stylish 84 square-foot home has started a company to help other people build their own mini-homes. It's all part of the "tiny house" movement, a trend becoming more popular as people look for ways to save money, help the environment and simplify their lives.

Think this will this catch on? I don't, at least in a big way. 84 square foot homes (or even 250) are simply too extreme. However, tiny homes are just a small part of a major and growing trend towards frugality and downsizing in general.

That trend has just begun. It is a crucial part of the deflationary environment in which we live.

It's been one hell of a non-recovery in housing, smack in the face of now-expiring $8,000 home tax credits that have proven to be as stimulative and futile as attacking fire ants with a BB-Gun.

Foreclosure filings climbed in three-quarters of U.S. metropolitan areas in the first half as high unemployment left many homeowners unable to pay their mortgages, according to RealtyTrac Inc.

The number of properties receiving a filing more than doubled from a year earlier in Baltimore, Oklahoma City and Albuquerque, New Mexico, the mortgage-data company said today in a report. Notices of default, auction or bank seizure rose more than 50 percent in areas including Salt Lake City; Savannah, Georgia; and Atlantic City, New Jersey.

"Foreclosures are spreading out from areas that had been hardest hit," Rick Sharga, senior vice president for marketing at Irvine, California-based RealtyTrac, said in a telephone interview. "We're dealing with underlying economic weakness as opposed to unsustainable home prices and bad loans."

Continued weakness in employment and efforts to prevent foreclosure may "delay the inevitable" and weigh on home prices, RealtyTrac Chief Executive Officer James J. Saccacio said in a statement.

The company said 154 of 206 U.S. metro areas with populations of more than 200,000 had increases in households with filings from January through June.

Cities in Nevada, Florida, California and Arizona accounted for the 20 highest foreclosure rates. Nine of the top 10 metro areas had decreases in the total properties receiving filings, a sign that foreclosures may have peaked in the states hurt the most by the housing market's collapse, RealtyTrac said.

Video with Rick Sharga Senior Vice President of RealtyTrac

Partial Transcript: "There is a pretty direct correlation between job loss and foreclosure. Until the unemployment rates start to go down, and until we actually see net job creation, and importantly until consumer confidence comes back, the housing market has really slim chances of recovery. That coupled with the huge overhang of distressed property, really suggests the housing market is not going to turn around for the next few years."

The excesses of the current cycle have never been greater in history. The odds are strong that we have seen secular as opposed to cyclical peaks in housing starts and new single family home construction. With that in mind it is highly unlikely we merely return to the trend. If history repeats, and there is every reason it will, we are going to undercut those long term trendlines.

There will be additional pressures a few years down the road when empty nesters and retired boomers start looking to downsize. Who will be buying those McMansions? Immigration also comes into play. If immigration policies and protectionism get excessively restrictive, that can also lengthen the decline.

Finally, note that the current boom has lasted well over twice as long as any other. If the bust lasts twice as long as any other, 2012 just might be a rather optimist target for a bottom.

The Last Bubble is Not Reblown

In a few locations, the bottom may be close at hand but certainly not everywhere. More importantly, think of tech stocks and remember the creed "the last bubble is not reblown". Ten years after the tech bust, the Nasdaq is still down over 50%.

The recovery in housing will be even slower. There is no need to rush into housing at this point even IF the bottom was at hand.

Governor Schwarzenegger has once again furloughed workers, declaring California is in a fiscal emergency. Excuse me for asking but when has California ever not been in a state of fiscal emergency?

California Governor Arnold Schwarzenegger ordered more than 150,000 state workers to take three days of mandatory unpaid time off to conserve cash.

The executive order, effective Aug. 1, stipulates that the furloughs will end when a budget for the fiscal year that began July 1 is enacted, the governor's press secretary, Aaron McLear, said in an e-mail. It comes after government workers endured furloughs over almost 12 months that ended June 30.

California began its fiscal year without a spending plan after Schwarzenegger and Democrats remained deadlocked over how to fill a $19.1 billion deficit. Controller John Chiang has warned he may again need to issue IOUs to pay bills if the impasse continues into September.

"Every day of delay brings California closer to a fiscal meltdown," Schwarzenegger said in a statement today. "Our cash situation leaves me no choice but to once again furlough state workers until the Legislature produces a budget I can sign."

California Governor Arnold Schwarzenegger declared a state of emergency over the state's finances yesterday, raising pressure on lawmakers to negotiate a state budget that is more than a month overdue and will need to close a $US19 billion ($A21.3 billion) shortfall.

The deficit is 22 per cent of the $US85 billion general fund budget the governor signed last July for the fiscal year that ended in June, highlighting how the steep drop in California's revenue due to recession, the housing slump, financial market turmoil and high unemployment have slashed its all-important personal income tax collection.

In the declaration, Schwarzenegger ordered three days off without pay per month beginning in August for tens of thousands of state employees to preserve the state's cash to pay its debt, and for essential services.

California's budget is five weeks overdue, joining New York among big states with spending plans yet to be approved, and Schwarzenegger and top lawmakers are at an impasse over how to balance the state's books.

Analysts say it could be several more weeks before the Republican governor and leaders of the Democrat-led legislature reach an agreement, a delay that threatens to lower the state's already weak credit rating, now hovering just a few notches above "junk" status.

Schwarzenegger's new furlough order was instantly condemned by labor officials as a political ploy.

"To once again force state employees to take unpaid furloughs is just another punitive measure by Governor Schwarzenegger because he couldn't impose minimum wage," said Patty Velez, president of the California Association of Professional Scientists.

Political Ploy or Act of Sanity?

The unions accuse Schwarzenegger of playing politics. Here's the real story: He had 8 years to get rid of unions and failed to do so. He is not playing politics now, he played them before, being too spineless to take on the unions until recently.

Now he is a lame duck. Let's hope the next governor has more common sense. Don't count on it. After all we are talking about California where pandering to unions is the best way of getting elected.

By the way, can someone even tell me why California has an "Association of Professional Scientists"? Is there anything in California that is not unionized?

The solution is privatize everything, putting people like Patty Velez out on her ass where she has to do some real work instead of preying on taxpayers for more unjustified union benefits. The same applies to the prison guards and every other California union as well.

City Council members are considering doing away with a guaranteed pension for newer employees as the council struggles to bring Fort Worth's spending in line with the drop in taxes.

No decisions have been made. And Assistant City Manager Karen Montgomery said the city would still have to deal with a big backlog in pension costs even if the council decides to cut benefits. But pensions have been a sacred cow among state and local governments, and few others have even discussed cutting them.

By law, the city can't change the benefits that it's already paying retirees or those that it has promised to employees who have worked long enough to be vested in the pension system. Also, police and firefighter pensions are guaranteed under labor contracts.

The city could be forced to pour tens of millions of dollars into the pension system over the next few years, and pension costs are a major contributor to Fort Worth's projected $73 million budget gap.

"This is the elephant in the room for not only this budget but all future budgets," Mayor Mike Moncrief said.

Montgomery suggested moving new employees and perhaps even unvested employees to a "defined contribution" plan. The specifics of the plan haven't been determined, but Montgomery suggested a range of options, including annuities or accounts similar to a private-sector 401(k). That would be a game-changer for municipal employees, who often stay in their jobs because of the pension and other benefits.

"In our current pension, employees cannot outlive their benefit," Montgomery said. "In a defined contribution, that risk is on the employee to manage their money until they die."

Employees, including the police and firefighters associations, have argued to keep the pension system as it is. A committee made up mostly of employees recommended that the city contribute an additional 6 percent of payroll to the pension, which would fix the shortfall in a few years.

Finally!

At long last a major city in the US (Fort Worth has a population in excess of 600,000) is considering doing what desperately needs to be done: killing defined benefit pension plans for public workers.

Instead, the union suggests "an additional 6 percent of payroll to the pension, which would fix the shortfall in a few years". Where would that contribution come from? Taxpayers of course. Will it fix the system? No, it will not fix the shortfall because of insane pension plan assumptions.

The only solution is to kill these plans right here, right now. Unfortunately, such action will not fix the problem of unfunded plans for current vested employees, but it is a major step in preventing further buildup of a fiscally insane proposition.

If unions had any common sense they would embrace, not fight these decisions. The reason of course is the only other solution for cities would be to resolve these difficulties by declaring bankruptcy, putting accrued benefits at risk.

Just wanted to say thanks for the balanced and objective view on Afghanistan. My son is on the front lines with the 101st Airborne (Infantry). He's been there since the first week in May.

The things I could tell you would make your hair stand on end. What civilian leadership, with some complicity of military leadership is doing to our young men and women is repulsive.

The war is getting a little more coverage in the media now, but for a while there, it looked like all these fine men and women would be led to their deaths and no one would even know.

It has been hard as a parent (and there are MANY of us) not able to speak up. Most people have no idea what it is like to live 24/7 being terrified of the doorbell ringing.

Thanks again for the article on Afghanistan. The more people talk about it, the better chance something will be done.

Stephanie S. Jasky, Founder, Director - FedUpUSA.org

Troops Do Not Support The Mission

Several people have informed me that OPSEC bars the military from saying things like "Troops Do Not Support The Mission" no matter how true that might be. Thus, all those stuck in Afghanistan, not supportive of the mission, wanting to speak their minds have no means of doing so.

Worse yet, inability to speak ones mind not only applies to military, but their family's ability as as well. I am not just talking about sensitive data like troop, size, location, strength, etc, but simple matters of freedom of speech as to whether or not troops believe in what they are doing.

Freedom of speech means nothing anymore. It's the new American way.

The Vietnam Afghanistan Song

Well, come on all of you, big strong men, Uncle Sam needs your help again. He's got himself in a terrible jam Way down yonder in Vietnam Afghanistan So put down your books and pick up a gun, We're gonna have a whole lotta fun.

And it's one, two, three, What are we fighting for ? Don't ask me, I don't give a damn, Next stop is Vietnam Afghanistan; And it's five, six, seven, Open up the pearly gates, Well there ain't no time to wonder why, Whoopee! we're all gonna die.

Come on Wall Street, don't be slow, Why man, this is war au-go-go There's plenty good money to be made By supplying the Army with the tools of its trade, But just hope and pray that if they drop the bomb, They drop it on the Viet Cong Taliban.

And it's one, two, three, What are we fighting for ? Don't ask me, I don't give a damn, Next stop is Vietnam Afghanistan. And it's five, six, seven, Open up the pearly gates, Well there ain't no time to wonder why Whoopee! we're all gonna die.

With thanks to Country Joe and the Fish I wonder "Where are the protest songs?" Are boomers too worried about stock market and housing prices to care if our youth is getting slaughtered?

What ARE we there for anyway? Oil? Empire Building? Obama's Reelection Bid? All Three?

By the way, I neither endorse nor denounce other positions of FedUpUSA.org. I have not followed them closely enough to know. Rather, and as always, I support specific policies on a case by case basis. In this case we both seem to agree on the need to get the hell out of Afghanistan.

The best way to "Support the Troops" is to not put them needlessly in harm's way in the first place. It's time to declare the war won and bring them home.

President Obama has been a huge disappointment in regards to war, torture, Guantanamo Bay, and of course the economy. Youth of America, are you paying attention?

Bill Gross usually writes an interesting column provided you skip over the first few paragraphs of introduction. His August Investment Outlook regarding population demographics is no different. Please consider Private Eyes.

Our modern era of capitalism over the past several centuries has never known a period of time in which population declined or grew less than 1% a year. Currently, the globe is adding over 77 million people a year at a pace of 1.15% annually, but slowing.

Observers will point out, as shown in the following chart, that global population growth rates have been declining since 1970 with no apparent ill effects. True, until 2008, I suppose. The fact is that since the 1970s we have never really experienced a secular period during which the private market could effectively run on its own engine without artificial asset price stimulation. The lack of population growth was likely a significant factor in the leveraging of the developed world's financial systems and the ballooning of total government and private debt as a percentage of GDP from 150% to over 300% in the United States, for example. Lacking an accelerating population base, all developed countries promoted the financing of more and more consumption per capita in order to maintain existing GDP growth rates. Finally, in the U.S., with consumption at 70% of GDP and a household sector deeply in debt, there was nowhere to go but down. Similar conditions exist in most developed economies.

The danger today, as opposed to prior deleveraging cycles, is that the deleveraging is being attempted into the headwinds of a structural demographic downwave as opposed to a decade of substantial population growth. Japan is the modern-day example of what deleveraging in the face of a slowing and now negatively growing population can do.

The preceding analysis does not even begin to discuss the aging of this slower-growing population base itself. Japan, Germany, Italy and of course the United States, with its boomers moving toward their 60s, are getting older year after year. Even China with their previous one baby policy faces a similar demographic. And while older people spend a larger percentage of their income – that is, they save less and eventually dissave – the fact is that they spend far fewer dollars per capita than their younger counterparts. No new homes, fewer vacations, less emphasis on conspicuous consumption and no new cars every few years. Healthcare is their primary concern. These aging trends present a one-two negative punch to our New Normal thesis over the next 5–10 years: fewer new consumers in terms of total population, and a growing number of older ones who don't spend as much money. The combined effect will slow economic growth more than otherwise.

PIMCO's continuing New Normal thesis of deleveraging, reregulation and deglobalization produces structural headwinds that lead to lower economic growth as well as half-sized asset returns when compared to historical averages. The New Normal will not be aided nor abetted by a slower-growing population nor by cyclical policy errors that thrust Keynesian consumption remedies on a declining consumer base. Current deficit spending that seeks to maintain an artificially high percentage of consumer spending can be compared to flushing money down an economic toilet.

Keynesian Stimulus is Money Flushed Down the Toilet

Please read that last paragraph closely. Here is the key sentence "The New Normal will not be aided nor abetted by a slower-growing population nor by cyclical policy errors that thrust Keynesian consumption remedies on a declining consumer base."

If anyone needs to read that paragraph, it is none other than PIMCO's Paul McCulley.

In spite of the complete failure of Keynesian and Monetarist policies of Japan over two decades, amazingly Paul McCulley wants Japan to go "All In".

"Japan's problem is deflation, not inflation as far as an eye can see," wrote Paul McCulley, a member of the investment committee, and Tomoya Masanao, the head of portfolio management for Japan, in a report on the Web site of Newport Beach, California-based Pimco. "An 'all-in' reflationary policy is what is needed."

The BOJ may also consider promising to refrain from raising interest rates until inflation becomes "meaningfully positive," McCulley and Masanao said.

Definitions of Insanity

In One Sentence: Insanity is doing the same thing over and over and over and expecting different results each time.

In Two Words: Paul McCulley

In One Word: Keynesianism

In Another Word: Monetarism

Japan has already gone "all in". It has tried everything under the sun for two decades including Keynesianism, Monetarism, and selling its own currency to sink it. All it has to show for its efforts is a massive pile of debt equaling 227% of GDP.

Amazingly, some people have learned nothing from two decades of complete failure.

Send a Message to McCulley

I am glad to see Bill Gross admit that McCully advocates "flushing money down an economic toilet" because that is exactly what McCully has proposed on numerous occasions. My question now is "How long it will take for Gross to relay the message to McCulley?"

Now, if we can only get the message to Obama, Geithner, Krugman, Barney Frank, Nancy Pelosi, and all the other Keynesian clowns perhaps it would do some good.

That said, I do have one point of contention with Gross: Demographics or not, Keynesian stimulus never works. The idea one can spend one's way to prosperity is preposterous. As Japan has proven, attempts to do so in tantamount to a can-kicking escapade at best, and an unsustainable Ponzi scheme at worst. I lean towards the latter.

Not once do any of the Keynesian clowns ever address the question "What happens when the stimulus runs out?"

Keynesian Definition of Temporary is Forever

Take note of the $8,000 housing tax credits. Demand picked up and then subsequently collapsed. What next? Do we buy everyone a house whether they need one or not?

That is essentially what McCulley suggested when he asked for Japan to go "All In". That is what Krugman and others are suggesting still.

Geithner portrays it as "temporary".

The Keynesian definition of temporary is "until it works". In other words "forever" because lunacy cannot and will not work in a sustainable fashion. It only appears to work for short-term durations.

The classic example is the Greenspan induced housing bubble. Unemployment dropped to record lows , GDP soared, but in the end the bubble collapsed.

That is what "All In" does.

Demographic Analysis

While I commend the viewpoint of Bill Gross, it is hardly revolutionary except perhaps of his implied criticism of McCulley.

Structural demographic effects imply that prospects in the full-time labor market will be poor for those over age 50-55 and workers under age 30. Teen and college-age employment could suffer a great deal from (1) a dramatic slowdown in discretionary spending and (2) part-time Boomer reentrants into the low-paying service sector; workers who will be competing with younger workers.

Ironically, older part-time workers remaining in or reentering the labor force will be cheaper to hire in many cases than younger workers. The reason is Boomers 65 and older will be covered by Medicare (as long as it lasts) and will not require as many benefits as will younger workers, especially those with families. In effect, Boomers will be competing with their children and grandchildren for jobs that in many cases do not pay living wages.

Consider what such a decline in US GDP growth and its multiplier effect could mean for Asian growth, global trade, demand for commodities, and growth elsewhere in the world (BRIC).

The world equities markets have barely begun to discount the increasingly likely severe deceleration in US and world GDP growth ahead, including the secular Boomer drawdown of accumulated wealth of the past 25 yrs.

$400 Billion: Amount that will come out of annual U.S. consumption as thrifty boomers push savings rate from 1% to nearly 5%.

47%: Boomers share of national disposable income in 2005 before the bubble burst. Boomers contributed only 7% to national savings.

2.4%: Forecasted GDP growth over the next three decades as boomers ratchet back. GDP has grown 3.2% a year since 1965.

69%: Portion of boomers aged 54 to 63 who are financially unprepared for retirement.

78%: Boomers' share of GDP growth during the bubble years of 1995 to 2005

Those stats are from a McKinsey study, and there is nothing remotely inflationary about boomer demographics.

Nor is there anything inflationary about Generation X demographics. Generation X's have seen boomers blow it. By sharply curtailing spending, generation X at least has chance to right the ship before retirement. It's too late for most boomers. Time ran out.

Now consider generation Y with 19% of the population. Think the income levels of generation Y are going to catch boomers or generation X?

When?

Finally, think about tightening lending standards and attitudes about debt in general. Because of lower incomes and tighter lending standards, it is unlikely that Generation Y will be either able or willing to carry debt burdens to sustain a strong recovery.

Distortionary vs. Inflationary

Bernanke can flood the world with "reserves" and indeed he has. However, he cannot force banks to lend or consumers to borrow.

Here is a simple analogy that everyone should be able to understand: You can lead a horse to water but you cannot make it drink. And if the horse does not want to drink, it was a waste of time and energy to lead the horse to the water.

Yet every day someone comes up with another convoluted theory about how inflationary this all is. It is certainly "distortionary" in that it creates problems down the road and prolongs a real recovery by keeping zombie banks alive (as happened in Japan). However, it is not (in aggregate) going to cause massive inflation because it is not spurring the creation of new debt.

Recognition Phase

I have been talking about these trends for quite some time. The fact that Bill Gross is discussing these trends now is part of the "Recognition Phase".

Bear in mind that Robert Prechter figured this out decades ago, far before most anyone else, indeed far too soon to do him or anyone else any good. Consumers figured it out a year ago. Mainstream media of which Bill Gross is an early practitioner is just starting to catch on. Bill Gross is behind bloggers, but he is far ahead of most of his peers.

By the time mainstream media fully embraces these trends we will be two thirds through it. Such is the nature of the game.

Brutal Combination

Please note that it is not demographics per se that is doing us in, but rather enormous amounts of consumer debt (as a result of decades of Keynesian and Monetarist stimulus) in conjunction with unfavorable demographics and global wage arbitrage that is doing us in. Bill Gross missed this essential point.