Mish's Global Economic Trend Analysis |

- Stupid Times: NBA Star Puts ATM in Kitchen; Peak Sport Salaries?

- GDP, Real GDP, and Shadowstats "Theater of the Absurd" GDP

- New Confusion Over Hispanbonos and Regional Debt: Spanish Regional Government Accounting Postponed, Press Conference by Montoro is Postponed; Regional Government Debt Issuance Method Unclear

- Capital Flight Intensifies to Record Levels in Spain; Outflows Make Spanish Banks Increasingly Reliant on ELA Funding

- Eurozone Retail Sales Crash: Record Declines in France and Italy, Overall Revenues Drop at Near Record Pace

| Stupid Times: NBA Star Puts ATM in Kitchen; Peak Sport Salaries? Posted: 31 May 2012 07:16 PM PDT As a prime example of the extreme disparities between the haves and the have-nots as well as how stupid things have gotten in general, please consider DeShawn Stevenson Installs ATM In Kitchen For the sports star who has everything there remains one tiresome problem – how do you get hold of your millions without having to leave the house?Peak Sport Salaries? A friend writes: "Mish this is proof positive sports salaries have peaked or are about to peak." Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

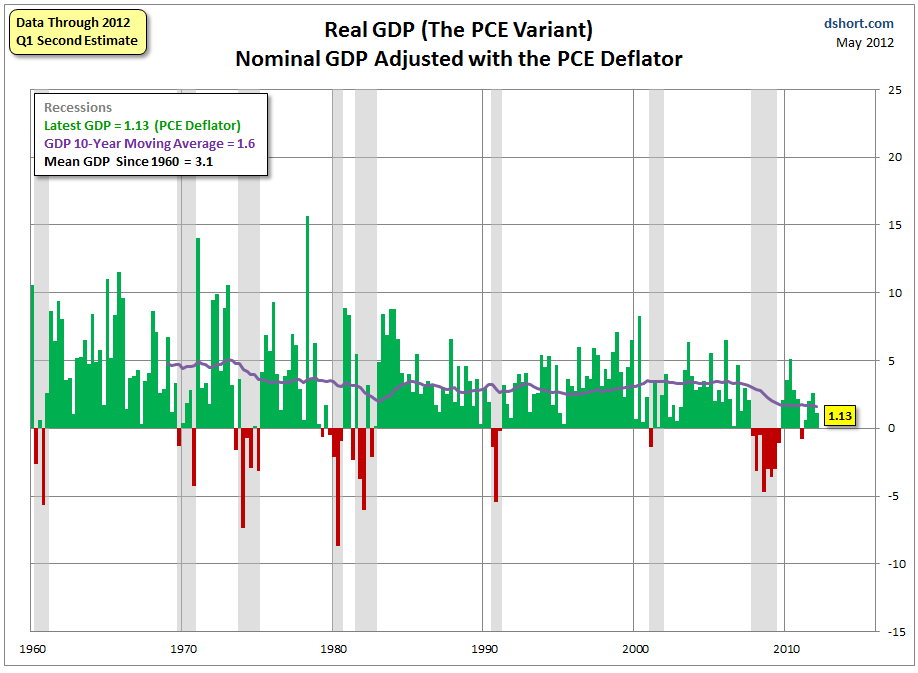

| GDP, Real GDP, and Shadowstats "Theater of the Absurd" GDP Posted: 31 May 2012 11:43 AM PDT Every month Doug Short at Advisor Perspective writes an excellent report on GDP. With today's release of the Q1 GDP Second Estimate, Doug Short has a new column worth a good look: Will the "Real" GDP Please Stand Up? (The Deflator Makes Big a Difference). How do you get from Nominal GDP to Real GDP? You subtract inflation. The Bureau of Economic Analysis (BEA) uses its own GDP deflator for this purpose, which is somewhat different from the BEA's deflator for Personal Consumption Expenditures and quite a bit different from the better-known Bureau of Labor Statistics' inflation gauge, the Consumer Price Index.GDP Four Ways Doug Short calculates the GDP using four different deflators.

The first three charts are all similar looking but charts 2 or 3 seems more reasonable than the official numbers. Here are two of the charts. Real GDP Using PCE  click on chart for sharper image Shadowstats GDP  click on chart for sharper image Doug Short Writes ... I find this "alternate Real" GDP to be interesting (in a bizarre sort of way), but I personally see no credibility in the hyper-negative GDP it produces. On the contrary, I see this chart as further evidence that the alternate CPI, despite its popular among many critics of government data, is a misguided concept.Alternate Nonsense Bizarre is a polite way of putting things. I would call it total nonsense. For Williams to be correct one would have to believe the economy was in a recession the vast majority of the time for the last 25 years. Williams has a huge following, mainly by the hyperinflationist crowd. Williams himself has been predicting hyperinflation for some time.

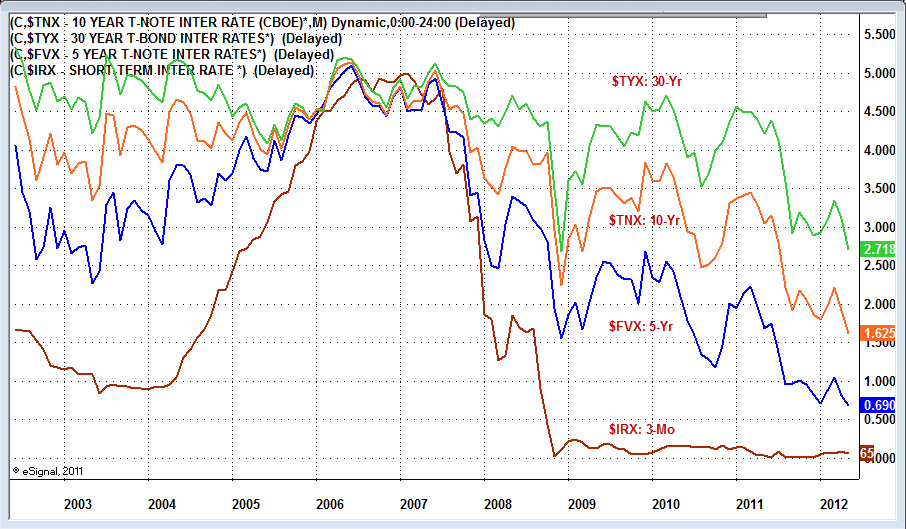

All of the hyperinflation calls have been missed by a mile. The dollar is strengthening, consumer credit is once again sinking, and treasury yields just made 60-year lows. This is what happens when you fail to take into consideration:

Williams makes all of those mistakes, being far too US-centric in his analysis, and compounds the errors by methodology that produces the absurd results shown above and also by confusing unfunded liabilities with debt. $1.06 Trillion of Consumer Debt is Currently Delinquent Note that according to the latest HOUSEHOLD DEBT AND CREDIT report by the Fed, consumer credit other than student debt is contracting. Also note that $1.06 trillion of consumer debt is currently delinquent, with $796 billion seriously delinquent. Think that will be paid back? I don't. And Hyperinflationists fail to understand the ramifications. I happen to agree that the US has a day-of-reckoning coming, but the entire fiat global financial system fueled by insane levels of fractional reserve lending will come crashing down at the same time. That is precisely why this deflationist (unlike others) happens to like gold as a safe haven. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 31 May 2012 09:42 AM PDT My friend Bran who lives in Spain writes ... Hello MishHispabonos are central government guarantees of regional debt. The regional governments want central guarantees because without them, interest rates will skyrocket. Presentation of Accounting Postponed Courtesy of Google Translate from El Economista: The Government postponed the presentation of the accounts of the CCAA's first quarter The Ministry of Finance has decided to postpone the press conference that he would publish the budget execution of the regions for the first quarter of the year in the National Accounts. Montoro endorse autonomy and park each issue of 'hispanobonos.Regional Governments Press for Hispanbonos The clear gist is regional governments are in severe trouble, probably much worse than reported. Delays are needed to present the facts to the Spanish central government which is now pressed by regional authorities once again to guarantee regional debt. Hispanbonos Already a Done Deal? Interestingly RTE News reported yesterday in Debt premium on Spanish bonds hits euro-era high that hispanbonos were already a done deal. Spain's government said it would approve the issuing of joint bonds -- "hispanobonos" -- by the 17 regional governments next Friday, so as to make it cheaper for them to finance their debts.Hispanbonos may (and should) trigger additional debt downgrades of Spanish sovereign debt and send yields higher. However, without guarantees, regional governments are going to have an exceptionally difficult time financing new debt and rolling over existing debt as well. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 31 May 2012 08:52 AM PDT Here is a note regarding capital flight in Spain and Greece that I received via email. Capital flight has intensified to record levels in Spain but interestingly leveled off in Greece. Capital flight from Greece is expected to resume when next reported given statements by the Greek president. The original source of this information appears to be Credit Suisse AG. Spanish private Sector Deposit numbers dropping at a faster rateMike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 31 May 2012 12:20 AM PDT Retail sales in France, Italy, and the eurozone as a whole hit the skids according to Markit. Retail sales in Germany were positive, but barely. Steepest Decline in French History Further sharp fall in French retail sales during May Key points:Record Declines in Italy Record year-on-year decrease in Italian retail sales in May Key points:German Sales Show Slight Growth German retail sales return to growth in May Key points:Sharp Drop in Overall Sales, Revenues Decline at Near Record Pace Eurozone retail sales continue to fall sharply in May Key points:This should bury the notion the eurozone recession will be short and shallow. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |