Mish's Global Economic Trend Analysis |

- Spain Potpourri: Official Denials From Finance Minister; More Nationalizations Coming Up; Banks Use ECB Money to Refinance Large Enterprises in Dire Shape, New Credit To Households Down 80%

- Screeching Halt in China; Weak Trade Data; Imports and Exports Fall Way Short of Expectations; Credit Crunch Underway; Feeble Forecasts From Pimco, Others

- Mish Interview on the "Daily Bell": Rise of Money Metals, Why Credit Matters

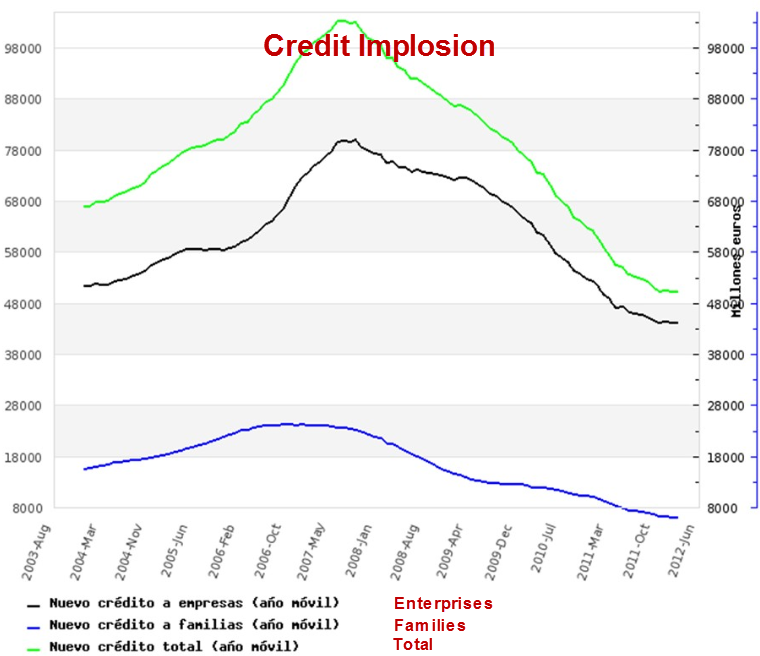

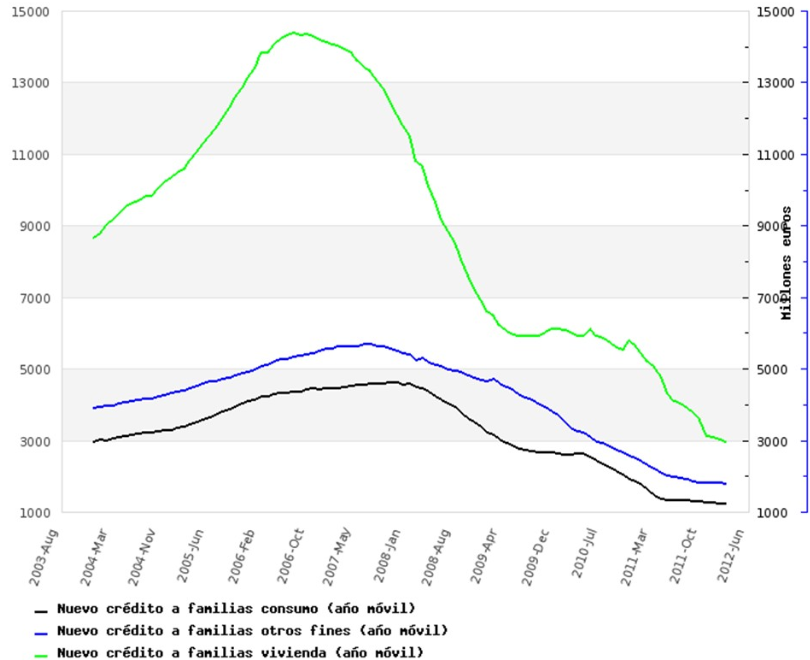

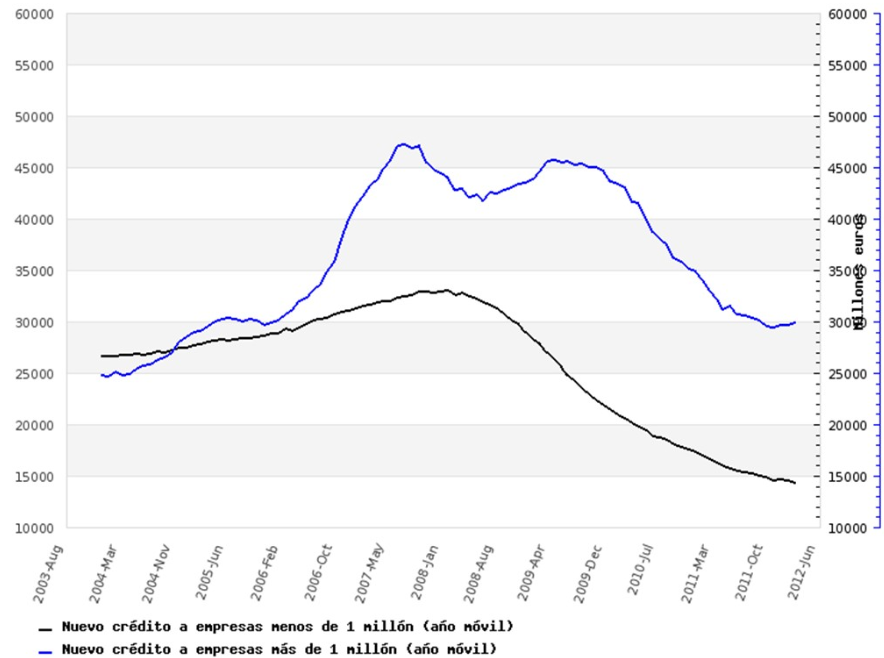

| Posted: 15 May 2012 05:04 PM PDT Official Denials From Finance Minister Finance Minister Says "Nothing to Hide" Asks for ECB Audit of Banks, Denies Need for Rescue Fund The Economy Minister Luis de Guindos, said Tuesday it has asked the European Central Bank (ECB) to assist in the independent audit of the Spanish banks' balance sheets and is committed to full throttle work as has asked the Eurogroup, in order to have results within two months.Another 30 Billion Euros Needed, More Nationalizations Coming Up Banks that do not return the aid within 5 years will be nationalized The State nationalize financial institutions that do not return within five years aid articulated through convertible bonds, the so-called 'coconuts', designed to 'clean up' their balance sheets of real estate assets.Collapse in Credit Banks Use ECB Money to Refinance Large Enterprises, New Credit To Households Down 80% Loans from the European Central Bank (ECB) for Spanish banks are finally beginning to be seen in the figures for new credit. After many months of fall shows signs of stabilization and down only 1.5%. However, the news is not as good as it seems.Ponzi Financing Those charts show the Spain is banking system is in deep, deep trouble in spite of official denials from the finance minister. Ponzi financing of the largest enterprises is the name of the game and the bond market has zeroed in on it. Yield on the 10-year bond has soared to 6.35%. I expect back above 7% soon. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 15 May 2012 03:48 PM PDT China bulls are in for a multi-year shock because rebalancing from an economy overly dependent on exports is going to be far more painful, and last much longer than most think. Data is coming in much weaker than expected, but I propose this is only the very beginning. The New York Times reports Data Signal Economic Trouble in China China announced Thursday that growth in imports had unexpectedly come to a screeching halt in April — rising just 0.3 percent from the same period a year earlier, compared with expectations for an 11 percent increase. Businesses across the country appeared to lose much of their appetite for products as varied as iron ore and computer chips.Imports and Exports Fall Way Short of Expectations The Financial Times reports China trade: warning signals. Whichever way you look at it, China's latest set of trade figures is bad news. Not only did both exports and imports fall short of expectations, they missed by quite a way.Easily Predictable All of this was easily predictable yet most did not see this coming and fewer still still see what is ahead. For example please consider this feeble China forecast by PIMCO. China's slowdown may deepen as policy makers unwind the excesses of a record credit boom while only gradually increasing stimulus, leaving 2012 growth at the weakest in 13 years, Pacific Investment Management Co. says.Bottom When? Note the feeble forecasts by Pimco, Citigroup, JP Morgan, Bank of America, and UBS. And what's with this bottom call by Pimco in the third quarter? I have to ask, third quarter of what year? 2020? What a bunch of collective bunk! I am sticking with 3.5% average growth for the rest of the decade, an idea proposed by Michael Pettis in a bet with The Economist. For details, please see 12 Predictions by Michael Pettis on China; Non-Food Commodity Prices Will Collapse Over Next Three to Four Years; Nails in the Hard Landing Coffin? Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Mish Interview on the "Daily Bell": Rise of Money Metals, Why Credit Matters Posted: 15 May 2012 09:16 AM PDT On Sunday, May 06, 2012 I gave an Exclusive Interview to the "Daily Bell" with Anthony Wile that I would like to share with my readers. The Daily Bell is pleased to present this exclusive interview with Mish Shedlock. Introduction: Mike "Mish" Shedlock blogs at Mish's Global Economic Trend Analysis, for which he has won awards from the New York Times, Time Magazine, Bloomberg, CNBC and Strategist News. Mish is a contributing "professor" blogger at the economic and financial education site Minyanville and offers podcasts every Thursday on HoweStreet. He's a registered investment advisor representative for SitkaPacific. He says that unlike many free-market "Austrians," he emphasizes credit impacts and deflationary trends within larger business-cycle manifestations. When not writing about economics, Mike enjoys photography; 80 of his photos have become magazine and book covers. Daily Bell: Give us some background. Mish Shedlock: My background is actually in computer programming and engineering. I worked for banks for 20 years primarily as a computer analyst working on the technical end of applications. I was an assistant vice president for Harris Bank for most of that time. AVP was as high a position as technicians could get. When Bank of Montreal bought out Harris, I left to become a consultant. Shortly after 9/11, contracts dried up and I was out of work for three years with literally no income. When the economy was doing well, I wasn't. My message at the time was cash is not trash and be prepared to lose your job. Needless to say, few listened. I started a blog in 2005 hoping to be discovered as an economic writer. Given there are millions of blogs the success of which are near-zero, one might even think such a chance would be impossible since I had no background in either economics or investing. However, I had some excellent teachers, primarily but not exclusively Austrian-economic minded. A person named Heinz Blasnik from Germany taught me Austrian economic fundamentals. I picked up many ideas about debt from Australian economist Steve Keen. More recently, Michael Pettis from China taught me nearly everything I know about trade. I blended those views into my own model on credit. I received lots of help from others at numerous spots along the way. Barry Ritholz at the Big Picture Blog promoted some of my material and Calculated Risk created the first template for my blog. Daily Bell: How did you get interested in investing? Mish Shedlock: Shortly before I lost my job, I started hanging out on stock message boards. I met some pretty smart minds on a place called Silicon Investor and I ran one of the most popular boards on the Motley Fool. Daily Bell: Why do people call you "Mish"? Mish Shedlock: Every bank I worked at formulated user IDs out of a combination of one or two characters from first names and six characters of last names. Thus my login to many banks where I worked was Mishedlo. I used that name on the Motley Fool and Silicon Investor. In stock message chat rooms, people truncated that to "Mish." I thought "Mish" had a nice ring to it and adopted it as my "brand." Daily Bell: Tell us about your relationship to Sitka Pacific and how it was formed. Mish Shedlock: Sitka Pacific was founded by Brian McAuley. His background is not stocks or the economy, either. Rather, Brian worked for a biotechnology firm. I met Brian on the Motley Fool in early 2000. At the time he was trading for himself, then himself and family, then friends of family. Once you get above ten, you need a license. He got that license and decided he no longer wanted to work in biotechnology but rather the investment community by putting their needs first. Indeed, Sitka always puts client needs first. That does not mean we will always be right but rather we will never do anything that puts our interests first. I am proud of the fact that our backgrounds are not Wall Street oriented. Daily Bell: Tell us about Minyanville. Mish Shedlock: Shortly after I started my blog John Succo, a Minyanville "professor," asked the founder, Todd Harrison, to post my columns. There was some concern by the Minyanville staff that I did not have a Wall Street or hedge fund background. However, eventually, my work stood for itself. I have always believed that being an outsider and not having preconceived notions about money supply, money multipliers, buy-and-hold strategies and efficient market theory (which I think is nonsense) to be to my advantage. I was the first industry outsider (I was not yet at Sitka) to make "professor" status. The term simply means regular contributor. Daily Bell: What is your relationship to Dollar Collapse? Mish Shedlock: Many of the ideas I write about come from articles I read elsewhere. Dollar Collapse and Bloomberg were at the top of the list. Currently I get many stories from Financial Times. Also, writers from around the world send me links. "Brisbane Bear" sends me stories every day from Australia. "Bran" sends me links every day from Spain. I get email updates from Michael Pettis in China and from Steen Jakobsen, the chief economist from Saxo bank in Copenhagen, to name a few. Literally I am swamped with links from all over the world. My goal is to make sense of the news. Sometimes I agree with those I quote and sometimes I am very harsh. Either way, I try to add something to the conversation, not just copy a story. Daily Bell: How were you able to find the time to do so much incisive writing? Mish Shedlock: When you are out of a job, with no income, you have plenty of time on your hands. That is how it all started. Now blogging and Sitka Pacific are full-time jobs. I am reading and writing 14 hours a day on many days. However, it does not seem like a job. Many times I am laughing my head off at what I write and hope others do, too. One of the best compliments I ever received was when someone asked me to please remind them to not drink coffee while reading my blog. That request came from someone who spit coffee out his nose trying to suppress laughter while reading my blog. Certainly I am not always humorous. Sometimes I am sarcastic, angry or questioning. There is no particular slant I try for. However, my role is always the same: to make sense out of the news in an educational way that people can easily relate to. I am pleased the New York Times recognized that effort, naming my blog, along with Calculated Risk and the Big Picture, as their number one idea for the year. (See "NYT 10th Annual Year in Ideas - #1 Idea of the Year 'Do-It-Yourself Macroeconomics.") Daily Bell: Do you consider yourself an Austrian in some sense? Mish Shedlock: Absolutely I am Austrian. Money supply and credit are paramount in economic analysis. However, many Austrians missed the mark badly by failing to consider credit. To me, inflation is an increase in money supply and credit with credit marked to market. Deflation is the opposite. Those who predicted massive "price inflation" based on rapidly rising base money supply or M2 missed the boat and missed it badly. Many Austrians called for treasury yields to go to the moon. When oil hit $140 in 2008 I called for record low yields across the entire yield curve. Most thought I was crazy. My rationale was based on credit, the demand for more credit and the value of credit on the balance sheets of banks. The demand for credit plunged, the value of debt as an asset on balance sheets plunged and in response, yields plunged. This set of events was very predictable but many called for hyperinflation based on rapid increase in base money supply and the misguided money multiplier belief that increases in money supply get lent out ten times over. In practice, the money multiplier theory is nonsense and the $1.5 trillion in excess reserves at the Fed proves it. Banks lend under three conditions, all of them required: 1) Banks are not capital impaired. 2) Banks believe they have credit-worthy borrowers. 3) Credit-worthy businesses and individuals want loans. If any of those conditions fail, credit expansion goes nowhere (at best) and is negative if defaults rise. Except for student loans, credit expansion has indeed gone nowhere in this recovery. I wrote about credit expansion recently, complete with nice charts, in my post, The Real Consumer Credit Story: Virtually No Recovery in Revolving Credit, No Recovery in Non-Revolving Credit. Daily Bell: What is your position relative to Bill Still, Ellen Brown and others who espouse public central banking? Mish Shedlock: Should populist Ellen Brown get her way, I would have to rethink my US hyperinflation position. Sadly, Brown is another one of those who understands various problems with the Fed, but proposes a solution that is worse, putting state politicians in charge of printing presses. When push comes to shove, the Fed would protect the banking system. Politicians would not. Moreover, the idea that North Dakota, a small, loosely populated farm state is in good shape because it has a state bank is preposterous. Worse yet, Brown takes that absurd position to the extreme, with a proposal to end the Fed and put California politicians (state politicians in general) in charge of printing money to support union causes. For further discussion please see "Lawmakers Threatenn to Take Over Monetary Policy." Daily Bell: You want to end the Fed don't you? What would you put in its place? Mish Shedlock: One word: nothing. The free market can easily set interest rates. Daily Bell: Do we need government bureaucrats to dictate the production or the price of cement, oranges, automobiles, computers or copper? Mish Shedlock: Anyone proposing such an insane idea would be laughed out of the room yet we expect a bunch of academics, with no real world experience, to do something far more difficult: set the proper amount of money and the interest charged on it. The idea is as ludicrous a Russian central planners setting steel production levels. Results speak for themselves: a series of economic bubbles and collapses with increasing amplitude in both directions. The result is a shrinking middle class and increasing wealth concentration at the top. Daily Bell: Does Greenbackerism lead to inflation? If not, why not? Mish Shedlock: Before there can be intelligent discussion, one must define the terms "Greenbackerism" and also "inflation." Let me ask a simple question: What's more important to the economy, home prices falling from $600,000 to $250,000 or the price of steak going from $4.99 to $5.99 or gasoline from $2.50 to $4.00. People constantly moan about the latter, but economically speaking, the plunge in home prices is far more important. I discussed this at length in "How Far Have Home Prices 'Really' Fallen? HPI and the CPI." I suspect the answer to your "Greenbackerism" question is, "Yes, eventually," with an emphasis on eventually. It is safe to say, regardless of your definitions, that printing is unsound and ultimately, printing money leads to bigger boom-bust cycles or other economic distortions that crucify the middle class. Once again, my definition of inflation is an increase in money supply and credit, with credit marked-to-market. Deflation is the opposite. Let's compare the practicality of my definition vs. a definition that involves prices or a definition that involves money supply in isolation. If the definition of inflation is a nominal rise in the CPI, then the inflationists have allegedly been correct. However, treasury yields are at record lows, home prices are at record lows, jobs have languished and credit has stalled. Simply put, most of the things one would expect to see in inflation have not happened. The same holds true for those who only look at exploding base money, forever predicting the money will multiply ten times over and treasury yields will soar. On the other hand, my credit-view of deflation has accurately called for most of these things, including the rise in the price of gold and a collapse in the value of houses. Like Humpty Dumpty, people can define the term inflation however they want, but those who miss the boat on credit are left wondering why the economy is not acting as generally expected by their definition. Most Austrians completely missed the ramifications of collapsing credit and the collapsing value of credit on bank balance sheets. Similarly, virtually all Keynesians missed the boat on the housing bust. In general terms, Keynesians missed the inevitability of a collapse that must follow a reckless expansion of credit. Only those who focused on credit have been properly aligned with what is actually taking place. Daily Bell: What's the future for the EU? Mish Shedlock: No currency union in history has ever survived without there being a fiscal union as well. Since there will not be a fiscal union, the Eurozone must break up. The ideal way would be for Germany and the Northern countries to exit. The painful way will be a piecemeal exit. I expect this to be long and painful. Daily Bell: How about China? Mish Shedlock: China is due for a "hard landing" which I define as less than 3.5% growth for the rest of the decade. I expect commodity prices will likely crash and the commodity producing currencies such as Australia and Canada will take a big hit as well. The Economist believes China will be the world's largest economy by 2018. I suggest 2030 may be optimistic and Chinese growth will average 3% or less for the rest of the decade. For a discussion of the implications, please see "12 Predictions by Michael Pettis on China; Non-Food Commodity Prices Will Collapse Over Next Three to Four Years; Nails in the Hard Landing Coffin?" Daily Bell: If China goes into a meltdown, the world faces a full-scale depression. What's your take? Mish Shedlock: The US will actually fare relatively well in a collapse of China. It is the trade surplus nations and commodity produces that will take the biggest hit as noted in the previous link. Daily Bell: Where is the US headed? Mish Shedlock: The US is headed for recession. The US recession will not be as bad as Europe, but corporate earnings will sink like a rock. The US dollar will strengthen much to the dismay of the hyperinflationists. Then, after Europe, China, and Japan take big hits, then and only then will the final plunge in the US dollar occur. Daily Bell: Where is Japan headed? Mish Shedlock: Japan is all but guaranteed to blow up before the US. A mere rise in long-term interest rates from 1% to 2% would consume nearly all government revenues. Ironically, I like Japanese equities but only hedged against a plunge in the Yen. After 20-plus years of deflation, Japanese companies have almost no debt but the currency risk is huge. Daily Bell: Are you confident of your businesses success in the US? Mish Shedlock: If you mean me personally, yes, pretty much so, but not overconfidently so. I am debt-free. We paid off our mortgage this month. The key will be to catch the turn. I will not be bearish forever. Daily Bell: Are you thinking of traveling abroad? Mish Shedlock: Personal difficulties make overseas travel problematic. I am now involved in a fundraiser for ALS research (Lou Gehrig's Disease). My wife is in the late stages and nearly immobile. She has been on a feeding tube for over a year and cannot eat or drink anything, including water. So far, people from at least 22 countries have made donations. I ask everyone to please consider making a contribution. To learn how you can help, please read "My Wife Joanne Has ALS, Lou Gehrig's Disease." Daily Bell: What do you think of US monetary policy? Mish Shedlock: It's hopeless. We should get rid of the Fed specifically and all central bankers in general. As noted earlier, central bankers are nothing but serial bubble blowers. The irony is they purport to be "inflation fighters." In reality, central banks are the very cause of inflation. Bernanke even wants a 2% inflation target. Economically speaking, it's crazy. Eventually asset prices and wages do not follow consumer prices and all hell breaks loose, which is precisely where the global economy is today. I have some nice charts of inflation targets and real disposable income in "Huge Problem With Bernanke's 2% Inflation Target Explained in Pictures." Daily Bell: On US government statistics? Mish Shedlock: Any statistics that need to be produced, the free market can do better and cheaper. For example, Gallup does monthly surveys on unemployment and they do a very good job. Do we need a mountain of highly paid government bureaucrats to gather unemployment stats? I think not. Most do not believe the stats anyway. Daily Bell: What's in the future for gold and silver? Mish Shedlock: Gold is money. When available, the free market has always selected gold as money. Government decree cannot change that fact. Silver, however, has a huge industrial component. Sometimes silver acts like money but most of the time it acts more like a commodity plaything. Would the free market accept gold and silver as money right now if allowed? I don't know but I sure would like to find out. What sets me apart from the Prechter deflationists is my recommendation that people hold 10-30% of their investment capital in gold. I do not have a price target but strongly believe another big surge is coming. Note that gold does not necessarily respond to movements in the US dollar. For example, the US dollar index is near 80. The dollar index was at 80 in late 2004 and gold was just over $400. If gold is not responding to moves in the dollar then what is it responding to? I suggest gold has responded to central bank efforts to revive credit. It has also responded well to sovereign credit stress. The Fed wants home prices to rise. The Fed also wants another credit lending spree. Neither happened. Clearly, the Fed can provide liquidity but it cannot determine where (if anywhere) liquidity goes. Since more liquidity efforts are surely on the way, and gold is the likely beneficiary, I highly doubt that gold has peaked. Eventually there will be a huge currency crisis and gold will soar. Daily Bell: Tell us more about the performance of your firm. Mish Shedlock: Sitka Pacific manages portfolios that look across asset classes in an effort to generate absolute returns without exposing the portfolio to catastrophic drawdowns. You can find more information including our 6-plus year performance track record at sitkapacific.com. Daily Bell: What's your investment strategy? Mish Shedlock: Sitka Pacific is very cautious right now. Our Absolute Return strategy currently has a position in gold, but is otherwise essentially market neutral. Our current mission is risk avoidance with a focus on avoiding the next big decline. We feel risk is high and if we avoid big drawdowns we will more than make up for it by hopping in when valuations are more attractive. To be fair, I said the same thing over a year ago. Sometimes the market has other ideas. That's why we do not use leverage, and we are never net short. My personal views on risk and valuations are reflected in my post, "Misty Water-Colored Memories, Dirt-Cheap Stocks, and Patient Opportunism." I also believe there is a strong likelihood of "Negative Returns for a Decade." There are numerous references in the preceding link. Daily Bell: Do you believe there's a power elite that wants to create global government? Mish Shedlock: Yes. One can easily see it in Europe. Many are angling for what I call the European "nanny zone." One can also see the idea in various IMF Special Drawing Rights proposals. Daily Bell: Is that a good idea? Mish Shedlock: Obviously not. It will fail for the same reasons the Euro will fail. Europe is the big test and I think the Eurozone splinters. Should the Eurozone actually hold together, expect zero growth for at least a decade. Germany will take a huge hit regardless. Either Germany provides more capital, or the Southern states default leaving Germany holding the "euro bag." Expectations that Germany will decouple from the rest of the Eurozone are thus nonsensical. Daily Bell: What about this tax situation? Why the current emphasis on tax revenue? Mish Shedlock: Hiking taxes in the midst of a global recession is foolish at best. Europe and the US need work rule reforms and pension reforms, not higher taxes. I strongly support ending collective bargaining of public unions, scrapping Davis-Bacon and all prevailing wage laws and instituting national right-to-work laws. Many US cities are effectively bankrupt by making pension promises that cannot be met. Greece is bankrupt for that reason (and others) as well . Raising taxes is not the answer. So what's the solution? I have an eight point proposal in "Public Unions Bankrupt Illinois: Unpaid Bills Top $9 Billion as Comptroller Reports 'State Treading Water'; Mish's Eight-Point 'Bold' Plan to Save Illinois." Daily Bell: Where do you go from here? Mish Shedlock: I am thinking about writing a book on the direction the US should take. I have lots more ideas. However, the problem is finding the time to do it. Daily Bell: Thank you for taking time from your busy schedule for this interview, and our best wishes to you and your wife. Mish Shedlock: Thank you for the invitation. Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment