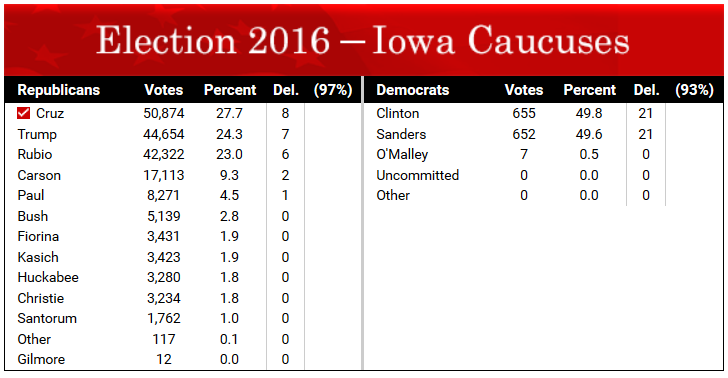

| Iowa Caucuses: Cruz Edges Trump and Rubio; Clinton and Sanders in Dead Heat Posted: 01 Feb 2016 09:06 PM PST Ted Cruz was the surprise winner in the Iowa Republican caucuses tonight edging out Donald Trump who in turn edged out Marco Rubio in a very strong voter turnout. On the Democratic side, Hillary Clinton is just a handful of votes ahead of socialist Bernie Sanders in a vote still too close to call. Given that Clinton was ahead of Sanders by 40 percentage points a few weeks ago, this result may raise more eyebrows than Cruz did by winning the Republican side. Via Real Clear Politics, the delegate totals look like this.  Mike Huckabee dropped out tonight. In speeches following the caucuses, both Trump and Rubio reached out to Huckabee. New Hampshire Trump and Sanders are both supposed to easily win new Hampshire. Unless Trump puts in a poor New Hampshire showing, Iowa will soon be a meaningless result. Hillary's test comes after New Hampshire. Mike "Mish" Shedlock |

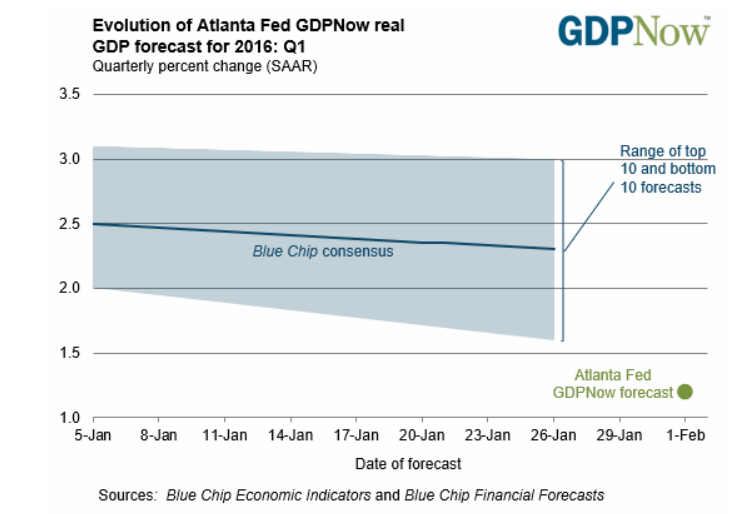

| "Blue Chip" Optimism vs. GDPNow 1.2% 2016 Initial Q1 Forecast; Strengths and Weaknesses of GDPNow Posted: 01 Feb 2016 10:30 AM PST "Blue Chip" OptimismThe Atlanta Fed initial GDPNow Forecast for first quarter 2016 starts off with an anemic 1.2% whimper. "The initial GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2016 is 1.2 percent on February 1. " First Quarter 2016 GDPNow Forecast  The Atlanta Fed "Final" GDPNow Estimate for the 4th Quarter was posted on January 28. The 4th quarter "Blue Chip" consensus at that time was about 1.9%. The actual BEA release was 0.7%. Strengths and Weaknesses of GDPNow The strength of the Atlanta Fed GDPNow model is that it mimics BEA calculations, thus providing an advance look as to what the BEA will report. The inherent and unavoidable weakness in the GDPNow model is BEA revisions. GDPNow mimics a model in which data is revised, revised, and revised again. Late last year the BEA announced it made a major " processing error" in regards to construction spending. The error affects GDP all the way back to 2005. We will not know the total effect until July 2016. We do know the biggest errors pertain to 2014 GDP which will rise, and 2015 which will fall. I discussed the forthcoming construction revisions in depth in When are Construction Revisions Coming?Moreover, GDP is notoriously wrong around economic turns, like now. It's highly likely the GDPNow model has mimicked bad data from the BEA that will be revised substantially lower in the future. If so, the US is in recession now, with the vast majority of economists in Economic Fantasyland. Mike "Mish" Shedlock |

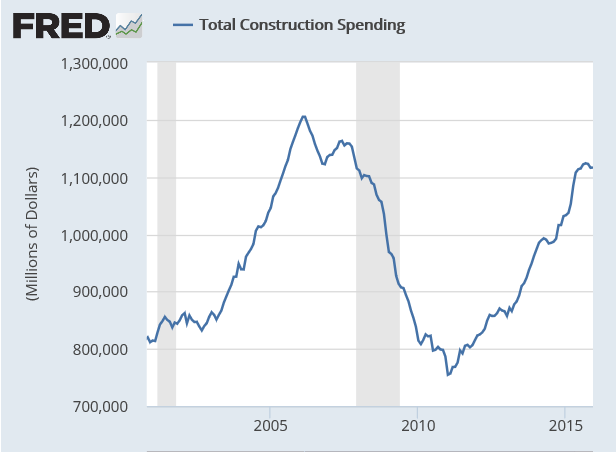

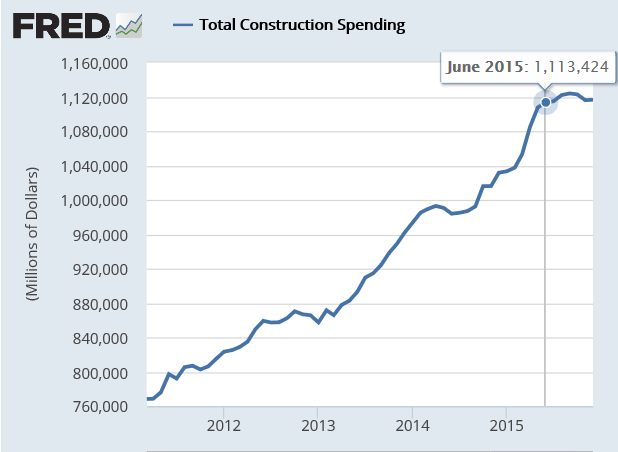

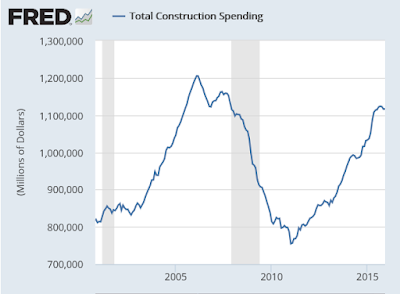

| Construction Spending Anemic Despite Warm Weather; Where to From Here? Posted: 01 Feb 2016 09:20 AM PST Economists expecting a huge surge in construction spending thanks to unusually warm December weather were no doubt shocked by today's anemic report. The Econoday Consensus Estimate was for +0.6% in a range of 0.3% to 1.3%, but not a single economist came close. Held down by weakness in the nonresidential component, construction spending didn't get a lift at all from the mild weather late last year, rising only 0.1 percent in December following a downwardly revised 0.6 percent decline in November and a 0.1 percent contraction in October. Year-on-year, spending was up 8.2 percent, a respectable rate but still the slowest since March last year.

But there is very good news in the report and that's a very strong 0.9 percent rise in residential construction where the year-on-year rate came in at plus 8.1 percent. Spending on multi-family units continues to lead the residential component, up 2.7 percent in the month for a 12.0 percent year-on-year gain. Single-family homes rose 1.0 percent in the month for an 8.7 percent year-on-year gain.

Now the bad news. Non-residential spending fell 2.1 percent following a 0.2 percent decline in November. Steep declines hit manufacturing for a second month with the office and transportation components also showing weakness. Still year-on-year, non-residential construction rose 11.8 percent.

Rates of growth in the public readings are led by highway & streets, at a 9.4 percent surge for December and a year-on-year rate of plus 12.0 percent. Educational growth ended 2015 at 9.4 percent with state & local at plus 4.4 percent. The Federal subcomponent brings up the rear at minus 1.4.

Lack of business confidence and cutbacks for business spending are evident in this report but not troubles on the consumer side, where residential spending remains very solid and a reminder that the housing sector is poised to be a leading driver for the 2016 economy. Still, the weak December and revised November headlines are likely to pull down, at least slightly, estimates for revised fourth-quarter GDP which came in at plus 0.7 percent in last week's advance report. Total Construction Spending Total Construction Spending Detail Total Construction Spending Detail Where to From Here? Where to From Here?Total construction spending has stalled since June 2015. Bloomberg noted the "good news" in residential. Residential construction, especially single family homes, is more likely to be more opportunistic based on weather. New Wal-Mart superstores etc., are planned events. It remains to be seen if " the housing sector is poised to be a leading driver for the 2016 economy". I strongly suspect "not". Mike "Mish" Shedlock |

| ISM Negative 4th Month, Employment Shows Significant Declines Posted: 01 Feb 2016 08:41 AM PST Manufacturing in January continues its dismal track record with the latest ISM reading. Econoday reports ... Employment sank the ISM index in January which could muster no better than a 48.2 for what, following annual revisions to 2015, is the fourth sub-50 reading in a row. This is by far the worst run for this closely watched indicator since the Great Recession days of 2009.

Employment fell a very steep 2.1 points to 45.9 to signal significant contraction for manufacturing payrolls in Friday's employment report, which however would not be much of a surprise given the sector's prior payroll contraction. This is the third sub-50 reading for employment of the last four months and the lowest reading since, once again, 2009.

There is good news in the report and that's a snapback for new orders, to 51.5 for only the second plus 50 reading of the last five months and which points to overall improvement in the coming reports. But backlog orders, at only 43.0, remain in deep contraction, and what strength there is in orders isn't coming from exports which are in contraction for the seventh of the last eight months. Manufacturers have been working down backlogs to keep production up, which came in at 50.2 to signal fractional monthly growth. Inventories remain steady and low but the sample still say they are too high, sentiment that points to lack of confidence in the business outlook.

Confirming the weakness is breadth among industries with 10 reporting composite contraction against eight reporting monthly growth. If it wasn't for strength in new orders, January's data would be almost entirely negative. This report is a downbeat opening to 2016 which follows a definitively downbeat year for the factory sector in 2015. ISM Manufacturing Index Let's further dive into the numbers straight from the ISM Report. | Index | Jan | Dec | PP Change | Direction | Rate of Change | Trend in Months |

|---|

| PMI® | 48.2 | 48.0 | 0.2 | Contracting | Slower | 4 | | New Orders | 51.5 | 48.8 | 2.7 | Growing | From Contracting | 1 | | Production | 50.2 | 49.9 | 0.3 | growing | From Contracting | 1 | | Employment | 45.9 | 48.0 | -2.1 | Contracting | Faster | 2 | | Supplier Deliveries | 50.0 | 49.8 | 0.2 | Unchanged | From Faster | 1 | | Inventories | 43.5 | 43.5 | 0.0 | Contracting | Same | 7 | | Customers' Inventories | 51.5 | 51.5 | 0.0 | Too High | Same | 6 | | Prices | 33.5 | 33.5 | 0.0 | Decreasing | Same | 15 | | Backlog of Orders | 43.0 | 41.0 | 2.0 | Contracting | Slower | 8 | | Exports | 47.0 | 51.0 | -4.0 | Contracting | From Growing | 1 | | Imports | 51.0 | 45.5 | 5.5 | Growing | From Contracting | 1 |

Key Points- Backlog of orders in contraction 8 months

- Exports back in contraction

- Prices in contraction 15 months

In December I stated " There's nothing in the ISM report to make the Fed want to hike, but the Fed will do what they want.The Fed did indeed hike. And economists still believe no recession is coming. For my take, please see Economists in Fantasyland: Economists See 20% Chance of Recession That's at Least 20% Likely Already Here. Mike "Mish" Shedlock |