Mish's Global Economic Trend Analysis |

- Schwarzenegger on Public Pensions and the Cost of the "Protected Class"

- Market Cheers 1.6% Growth; Treasuries Hammered; What's Next?

- Former Fed Vice Chairman vs. Mish: Is the Fed Out of Ammo?

| Schwarzenegger on Public Pensions and the Cost of the "Protected Class" Posted: 27 Aug 2010 01:31 PM PDT Now that Schwarzenegger is a certifiable lame duck (dead duck may be a more appropriate term) Schwarzenegger sees fit to take on public unions in a major way. It's too late now (for him) even as he speaks the truth. Please consider Public Pensions and Our Fiscal Future by Arnold Schwarzenegger. Recently some critics have accused me of bullying state employees. Headlines in California papers this month have been screaming "Gov assails state workers" and "Schwarzenegger threatens state workers."Schwarzenegger Washes His Hands Schwarzenegger drones on and on about who is to blame. He also acts as if he was fiscally responsible. That is far from the truth. In Turn out the lights California, the party is over I blasted Schwarzenegger's fiscally reckless proposals. Flashback March 2, 2007: Schwarzenegger wants $500 billion to rebuild CaliforniaThank God Schwarzenegger did not get what he asked. Now in massive revisionist history he attempts to take credit for being fiscally conservative. Please, let's stop the charades. While there is some truth he wanted concessions from unions, unlike Governor Chris Christie, he never fought for them very hard. Only now is he saying "All of these reforms must be in place before I will sign a budget." He should have said that in 2009, 2008, and 2007. He is saying that now that he is a lame duck. While I commend the idea, the problems he was elected to fix are more broken than ever. It will be interesting to see how this budget battle plays out, but no amount of hand-washing can absolve Schwarzenegger of his share of the blame. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

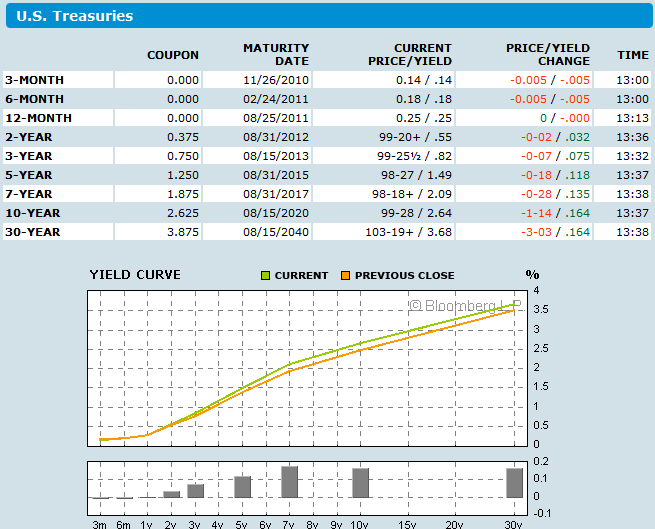

| Market Cheers 1.6% Growth; Treasuries Hammered; What's Next? Posted: 27 Aug 2010 10:56 AM PDT Today the DOW has crossed the 10K line for the umpteenth time (at least 3 times in the past 3 days alone depending on how you count), smack on the heels of "fantastic news" that second quarter GDP was 1.6%. For a change, economists were a bit too pessimistic but to get to that point, their estimates had to be ratcheted down twice from 2.5% to 1.4%. Now the market, temporarily at least, thinks 1.6% is good. It isn't. More importantly, GDP expectations looking forward for 3rd quarter are in the neighborhood of 2.5%, a number that is from Fantasyland. I expect a negative print. GDP News Release Inquiring minds are digging into the BEA's report National Income and Product Accounts Gross Domestic Product, 2nd quarter 2010 (second estimate) for additional details. Real gross domestic product -- the output of goods and services produced by labor and property located in the United States -- increased at an annual rate of 1.6 percent in the second quarter of 2010, (that is, from the first quarter to the second quarter), according to the "second" estimate released by the Bureau of Economic Analysis. In the first quarter, real GDP increased 3.7 percent.Positive Contributions

Take a look at that list and ask "How many of them will increase again in Q3?" Any? Amazingly, the deceleration in second quarter GDP was "partly offset by an upturn in residential fixed investment, an acceleration in nonresidential fixed investment, an upturn in state and local government spending, and an acceleration in federal government spending." Think housing will add to GDP in Q3? State and local government spending? Evolution of Estimates Dave Rosenberg discusses GDP in today's Breakfast with Dave. REVISIONISTS UNITE!Treasuries Hammered  After a massive rally in treasuries since April, at some point there was bound to be a correction. Exciting news of an unexpectedly "good" GDP at 1.6% was a nice trigger. The selloff looks sharp but it's not. 10-year treasury yields were above 4% in April. The 10-year yield after today's hammering is 2.64%. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Former Fed Vice Chairman vs. Mish: Is the Fed Out of Ammo? Posted: 27 Aug 2010 12:08 AM PDT Alan Blinder, a former Fed Vice Chairman says the Fed still has options if more monetary easing is needed. Please consider Fed Is Running Low on Ammo by Alan S. Blinder. Chairman Ben Bernanke has told the world that the Fed is not out of ammunition. It still has easing options, should it need to deploy them. The good news is that he's right. The bad news is that the Fed has already spent its most powerful ammunition; only the weak stuff is left. Mr. Bernanke has mentioned three options in particular: expanding the Fed's balance sheet again, changing the now-famous "extended period" language in its statement, and lowering the interest rate paid on bank reserves. Let's examine each.Mish Reply: It is not at all clear the Fed was "successful". Blinder is making an assumption that the Fed's purchase of MBS is what drove rates lower. Is that really the case or did Congressional guarantees of unlimited bankrolling of Fannie and Freddie losses do it? Perhaps it is a combination. Remember, at best the Fed can enhance the primary trend, it cannot change it. Regardless, New Home Sales Consensus 330K, Actual 276K, a Record Low; Nationwide, Zero New Homes Sold Above 750K . By what practical measure can Bernanke's efforts be considered a success? Alan Blinder: But when the Fed buys long-dated Treasury securities it is trying to flatten the yield curve instead—by bidding up the prices on long bonds. That effort also seems to have succeeded, perhaps surprisingly so given the vast size of the Treasury market. Now put the two together. By reducing its holdings of MBS and increasing its holdings of Treasurys, the Fed de-emphasizes shrinking risk spreads and emphasizes flattening the yield curve. That strikes me as a bad deal for the economy because the real problem has been high risk spreads, not high Treasury bond rates.Mish Reply: Once again, the question at hand is: Did Bernanke succeed and if so by how much? Clearly yields are lower, but why? The answer is the economy is weakening rapidly in spite of heroic efforts by both the Fed and Congress. In simple terms, the Fed failed to stimulate either lending or the economy. Thus yields fell. The goal was not to lower rates, the goal was to stimulate lending. Pray tell, how can a policy that failed to meet its objectives be construed a success? Alan Blinder: If the FOMC is serious about re-entry into quantitative easing, it should buy private assets, not Treasurys. Which assets? The reflexive answer is: more MBS. But with mortgage rates already so low, how much further can they fall? And would slightly lower rates revive the lifeless housing market?Mish Reply: The last damn thing we need is for the Fed to get creative. Can the already distorted economy possibly take any more Fed creativity? Look at the failures of all the stimulus programs. Are we any better off? Are banks lending? Are consumers in any better shape? In order, the answers are: No, No, No, No (not that the order makes any difference). Alan Blinder: The FOMC has been telling us repeatedly since March 2009 that the federal-funds rate will remain between zero and 25 basis points "for an extended period." This phrase is intended to nudge long rates lower by convincing markets that short rates will remain near zero for quite some time.Mish Reply: Blinder finally implied something that I totally agree with: jawboning by the Fed is virtually useless. Alan Blinder: Interest on reserves. In October 2008, the Fed acquired the power to pay interest on the balances that banks hold on reserve at the Fed. It has been using that power ever since, with the interest rate on reserves now at 25 basis points. Puny, yes, but not compared to the yields on Treasury bills, federal funds, or checking accounts. And at that puny interest rate, banks are voluntarily holding about $1 trillion of excess reserves.Mish Reply: Blinder is correct to assume paying negative interest on reserves will not stimulate much lending. Moreover, it would be stupid to try, because forced lending will increase bank losses. How much additional pain can the FDIC take? Blinder is also correct in stating the money will go somewhere. The "where" should be easy to spot although Blinder failed to mention it: longer dated treasuries. Should that indeed be the target, it would further suppress yields, which as Blinder says "strikes me as a bad deal for the economy because the real problem has been high risk spreads, not high Treasury bond rates" The second place money might go is gold. That would not do the economy much good either. Alan Blinder: There is a fourth weapon, which the Fed chairman has not mentioned: easing up on healthy banks that are willing to make loans. Given bank examiners' record of prior laxity, it is understandable that they have now turned into stern disciplinarians, scowling at any banker who makes a loan that might lose a nickel. That tough attitude keeps the banks safe, but it also starves the economy of credit.By not making risky loans, banks are acting responsibly for the first time in a decade. Now Blinder proposes more of what got us into this mess in the first place. Assets at Banks whose ALLL Exceeds their Nonperforming Loans  The ALLL is a bank's best estimate of the amount it will not be able to collect on its loans and leases based on current information and events. To fund the ALLL, the bank takes a periodic charge against earnings. Such a charge is called a provision for loan and lease losses. One look at the above chart in light of an economy headed back into recession and a housing market already back in the toilet should be enough to convince anyone that banks already have insufficient loan loss provisions. That is one of the reasons banks are reluctant to lend. Lack of creditworthy customers is a second. Quite frankly would be idiotic to force more lending in such an environment. Useless Jawboning The one thing I completely agreed with Blinder about is that jawboning is useless. However that has not stopped others from recommending the tactic. Jeannine Aversa, AP Economics Writer, claims Bernanke's top tool now may be power of persuasion. The economy appears to be stalling. Yet the Federal Reserve has run out of simple steps it can take to revive it. Short-term interest rates near zero have yet to rejuvenate the economy. The benefits of federal stimulus programs are fading, and Congress has declined to pass any major new economic aid. That puts increasing weight on Bernanke's words.A speech from Bernanke would not quiet the noise, rather it would be noise, and nothing but noise. "The challenge is for Bernanke to communicate to the world at large -- to financial markets and the public -- that monetary policy is currently contributing to the economic expansion, and we need to be patient, says William Poole, former president of the Federal Reserve Bank of St. Louis.The Real Challenge The real challenge for the Fed and President Obama is to admit neither the Fed's policies nor Congressional policies are working, that there are no short-term cures or fixes, and that it is time to share the pain more equitably including huge concessions from public unions, a haircut by Fannie and Freddie bondholders, and a reduction in unsustainable spending, especially military spending. Unfortunately, neither Bernanke, nor Obama is capable of saying what needs to be said, or doing what needs to be done. Unless and until they are, all the yapping by Obama and Bernanke will be as productive as giving a bullhorn to a bullfrog. For demagogues and fools, It's Not Practical To Tell The Truth. I wrote that column on August 1, 2008. Nothing has changed except banks and bondholders are better off at an enormous expense to ordinary taxpayers. Simply put, thanks to Obama and the Fed, the poor are bailing out the wealthy. No amount of bullhorn blowing can change that fact, and fortunately the public is starting to catch on. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment