Mish's Global Economic Trend Analysis |

- Looking for Love in all the Wrong Places? Contrary Investor Examines Misguided Fed and Obama Admin. Efforts to Increase GDP Via Increased Consumption

- Anecdotes on the Payroll Tax Cut

- Jobs Forecast 2011 Calculated Risk vs. Mish

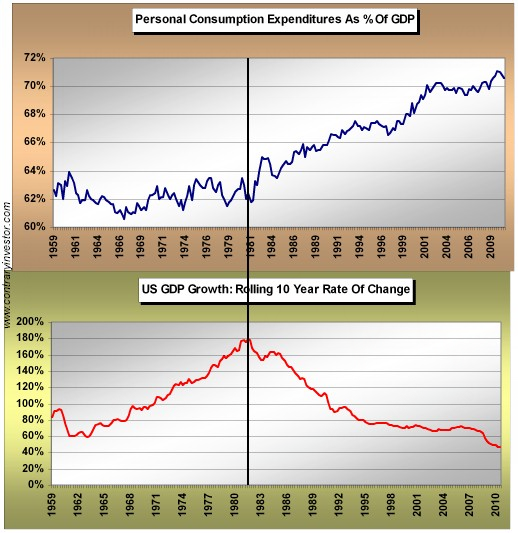

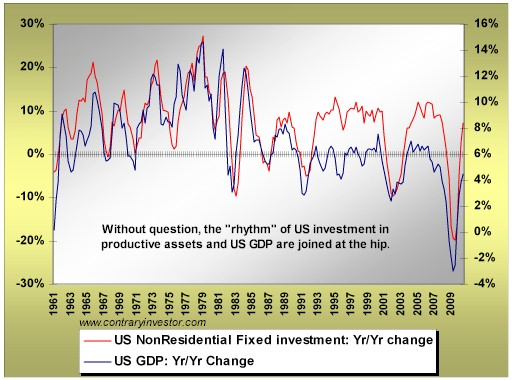

| Posted: 30 Dec 2010 05:16 PM PST The latest Contrary Investor Subscriber Report contains an interesting set of charts and commentary that shows just how misguided Fed and Obama administration focus on supporting consumption as the means to improve GDP. Their analysis is always well written, so inquiring minds may wish to take a closer look. I have permission to do occasional clips so please consider this clip from Looking For Love In All The Wrong Places? Looking For Love In All The Wrong Places?...You are all very much aware of the change in market tone and sentiment over the last four months. Strategists and investors fretting over rapidly deteriorating macro leading economic indicators (remember the ECRI reaching levels always consistent with recession?) and contemplating the possibility of a double dip has given way to these same folks now trying to one up each other in putting forth ever higher domestic GDP growth estimates for the new year. Goldman (Jan Hatzius) has been a poster child example of this about face, but they have plenty of company. The transition is not hard to understand. With the heavy POMO started in September, followed up by QE2, and now the tax cut extension legislation that should add about $400 billion of "new" fiscal stimulus in 2011, we better have an improved outlook. Certainly THE issue as we move into 2011 is the potential for organic economic growth, or otherwise. Personally, we just can't put a big "multiple" on marginal stimulus (read borrowed money) additions to macro near term economic expansion. But this issue will not become relevant until 2011 is well underway.Explaining Fed Actions The Fed is clearly beholden to the banks, especially large too-big-to-fail (TBTF) banks. Certainly the Fed may sound concerned about unemployment, but it's safe to assume the Fed's overriding concern is borrowers' ability and willingness to pay back the banks. History shows Bernanke's idea of inflation targeting at 2% ignoring asset bubbles that build along the way is economically stupid. So why does he do it? For the sake of argument and in deference to Occam's Razor , let's assume that all of the Fed's mistakes are out of ignorance as opposed to some conspiracy by the Fed to transfer wealth to the financial sector. Simply put, never ignore stupidity when it is a plausible answer to why something happened. Regardless of why, nothing changes from the perspective of the Bank CEO. The TBTF banks know full well they can take enormous economic risks, secure in the knowledge the Fed will bail them out if they get into trouble. The latest twist is Citigroup's chairman now brags that Citigroup is "Too Interwoven To Fail". Please see 98 TARP Recipients Close To Failure; Citigroup's Chairman Gives Reasons Citigroup Should Be Broken Up for details. When profits are rising CEO and executive compensation soars. When the banks fail, taxpayers bail out the banks and shareholders take the hit. However, the CEO gets a golden parachute worth hundreds of billions of dollars. Thus, from the perspective of TBTF banks, the right thing to do is take enormous risks. The same thing is happening in Canada right now. Please see Canadian Borrowing Gone Mad: A Look at BMO's Misguided Balance Sheet Theory and the Keep on Dancin' Market Share Theory of Toronto-Dominion for further discussion. This process explains the massive boom bust cycles we have seen and how wealth gets increasingly concentrated into fewer and fewer hands over time. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Anecdotes on the Payroll Tax Cut Posted: 30 Dec 2010 11:46 AM PST A small business owner friend of mine has some thoughts on the 2% payroll tax cut that I would like to share. SBO writes ... Hello MishThis adds to what I said in Jobs Forecast 2011 Calculated Risk vs. Mish (correcting a couple of awkward sentences). OK there is going to be more money in paychecks because of a reduction in Social Security collection. In response, I see ever increasing estimates as to how much that payroll tax cut will add to GDP.SBO adds another aspect I did not even consider. Some employees who share medical costs with their employer will have the payroll tax cut completely eaten up before they see a penny of it. The payroll tax cut will not be there to spend, it will have already been spent. That applies even more so to the self-insured. Then there are property taxes, state income taxes, and sales tax increases to consider (or additional cutbacks in states that do not raise taxes). GDP may get a small boost from this in theory, but the overall net effect will be a decrease in jobs and the average taxpayer will not see a dime of the decrease. Addendum: Here is a a reader email from David who lives in North Carolina regarding the above post. Hi Mish,Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

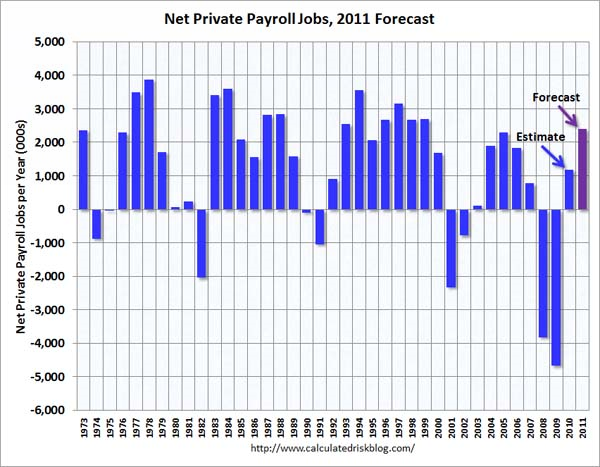

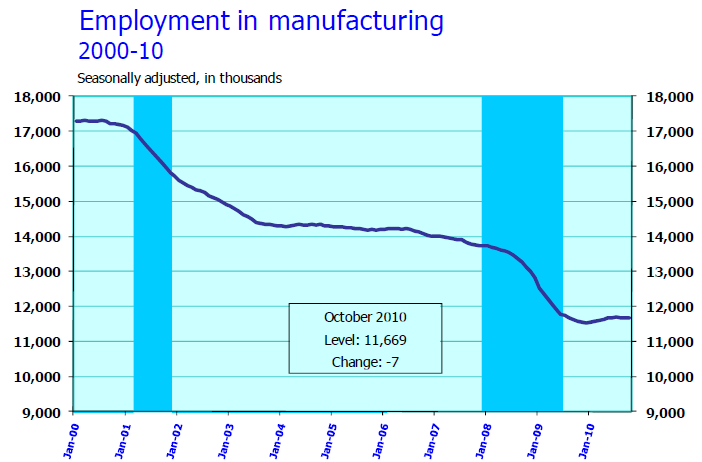

| Jobs Forecast 2011 Calculated Risk vs. Mish Posted: 30 Dec 2010 04:05 AM PST Calculated Risk, a good friend of mine, has come up with employment projections for 2011. He thinks the economy will grow by 2.4 million private jobs (200,000 a month), with an upside chance of 3 million jobs. I think those estimates are extremely high and we will not come close to even 2.4 million jobs. I give my rationale below, but first let's see what Calculated Risk has to say. Please consider Calculated Risk's Question #5 for 2011: Employment The U.S. economy added about 87 thousands payroll jobs per month in 2010 through November. This was extremely weak payroll growth for a recovery. How many payroll jobs will be added in 2011?What is the Driver for Jobs? One question I continually ask is "What is the driver for jobs?" Let's address that question, sector by sector, using all the major component breakdowns of job categories by the BLS, starting with the BLS Current Statistics reports for October or November (the latest graphs available). Please click on any chart below to see a sharper image.

January and February were a disaster for construction in 2010 so let's drop those. The average March through November is +3,000. Let's be generous and round to the nearest 5,000.  The average number of mining jobs January-October 2010 is +8,000. Mining Jobs Expectation for 2011 is +8,000 per month.

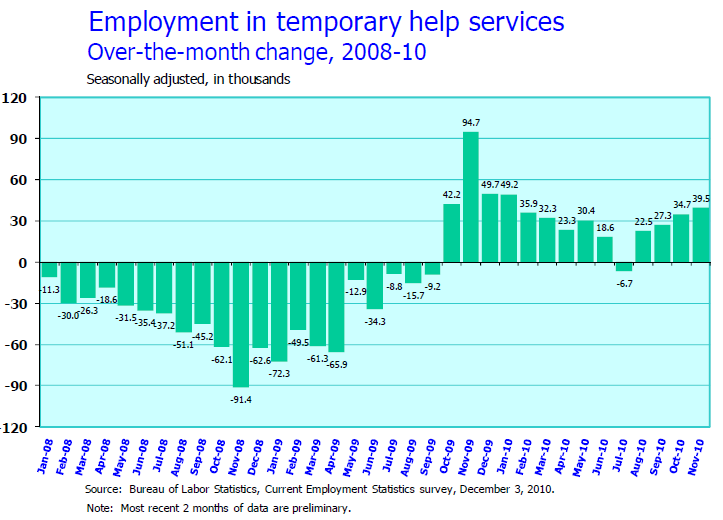

BLS has Temporary Help as a subcomponent of Professional and Business Services. It is hard to say whether or not permanent hiring takes hold but if it does it will likely be at some expense to Temporary Help. There are no charts available for Professional and Business Services, but let's add another 10,000 jobs a month to give a total of +45,000 jobs per month for Professional and Business Services.  Retail trade was certainly all over the map in 2010. I am not sure what to make of these big swings. The average for January-November 2010 is +6,000. Retail Trade Jobs Expectation for 2011 is +6,000 per month. Let's discard January and February as not being representative of the year. The 9 month average March-November is 9,000. Transportation and Warehousing Jobs Expectation for 2011 is +9,000 per month.  Financial activities is one sector that did not recover in 2010. Look for a repeat in 2011. Mortgage refinancing is falling off a cliff. I expect bank warnings about profits and lots of layoffs in this sector as a result of rising interest rates in general and mortgage rates in particular. The average number of jobs January-November is -7,000. Look for a repeat with job losses stacked in the first half. Financial Activities Jobs Expectation for 2011 is -7,000 per month.  The January-November average is +15,000. I think we have seen some of the restaffing we are going to get and growth in 2011 will not be as robust. Leisure and Hospitality Jobs Expectation for 2011 is +10,000 per month.  Healthcare has been a rock solid performer throughout the recession. The one possible downside to 2011 is cutbacks at country hospitals over budget concerns. Otherwise a continuation of 2010 seems likely. The average for January-October is +20,000. Let's ignore the downside risk and be slightly generous, using the average of the latest 4 months. Healthcare Jobs Expectation for 2011 is +24,000 per month. The BLS groups education and healthcare together in the monthly jobs reports (why I do not know). However in these summary reports the BLS breaks out healthcare separately. There are no charts for education. Education is one of the big wildcards. Traditionally this is a growing segment. However, cities are under a lot of pressure here. There could be losses in this component, perhaps big losses with increasing class sizes unless teachers' unions take pay or benefits cuts or unless help comes from the federal government. I am going to assume no growth in education as a middle ground. Education Jobs Expectation for 2011 is +0 per month. Wholesale trade is a minor jobs component. I do not have a chart, but will assume a nominal amount of growth. Wholesale Trade Jobs Expectation for 2011 is +3,000 per month. Information is a very minor jobs component. I do not have a chart. The last three months were -7,000, -1,000, and +1,000. Let's assume +1,000 a month. Information Jobs Expectation for 2011 is +1,000 per month. I do not have a chart of Other Services . The last three months were +17,000, +30,000, and -8,000. The average is +13,000. Other Services Jobs Expectation for 2011 is +13,000 per month.  Note how local governments were still expanding mid-recession, all the way up till July of 2008. A year later, starting June of 2009, local governments finally got religion and started cutting jobs. Look for this trend to continue into 2011. The average number of local government jobs for January-November 2010 was -21,000. Let's assume it will be the same for 2011 although there could be a disaster coming up at the local level. Local Government Jobs Expectation for 2011 is -21,000 per month.

In spite of all the whining at the state level, states have not yet made any significant cuts in employment. The average for January-November 2010 rounded to the nearest 1,000 is 0. Let's assume there will be no net gains or cutbacks at the state level for 2011, even though I expect some losses. State Government Jobs Expectation for 2011 is +0 per month.Total private employment January-November 2010 was +1.2 million. Total nonfarm employment was +951,000. That means 249,000 government jobs were lost so far in 2010. Of those 231,000 were local government jobs and none at the state level. Thus a net of 18,000 jobs, about 1,000 a month were lost at the Federal level. Instead, let's assume no net federal jobs for 2011. Totals and Subtotals by Category  I come up with +127,000 private jobs a month in comparison to Calculated Risk's estimate of +200,000 jobs a month. That is quite a difference. I have total nonfarm jobs at +106,000. Let's do a reality check. Monthly Job Growth 1999-2009  Chart courtesy of BLS. Annotations by me, numbers are in thousands. The areas in deep blue mark recessions.

Neither the housing boom, nor the commercial real estate boom is coming back. Nor is there going to be another internet revolution. If anything, outsourcing of jobs to Asia is likely to remain intense. Finally, consider all the financial engineering jobs, banking jobs etc, that are not coming back. I simply do not see any driver for jobs. Many of these optimistic scenarios are based on a "typical recovery". Well this is not going to be a typical recovery. Indeed, it already is not a typical recovery. Furthermore, Europe is a basket case, the housing bubbles in Australia and Canada are popping, China and India are both overheating and will slow, and topping it off, there is a very genuine chance that the retail hiring done for the Christmas season is all we get. Store expansion is not going to be like it was in 2006-2007. OK there is going to be more money in paychecks because of a reduction in Social Security collection. In response, I see ever increasing estimates as to how much that payroll tax cut will add to GDP. However, I have to ask "How much of that payroll tax cut will go to increased sales taxes, state income taxes, and property taxes?" I have not seen anyone properly address that question. I suggest we need that payroll tax cut to break even. Certainly taxes of all kinds are going up in Illinois. Our idiotic governor wants to hike income taxes 33%. Sales taxes will likely go up as well. While Illinois may be an extreme example, bear in mind that places where taxes are not going up will see more layoffs. Thus, from every angle, I struggle mightily to come up with +200,000 a month. Note that I stretched in several places to be purposely optimistic, tossing out bad months at the beginning of the year, etc. If everything goes right, perhaps we can add 160,000 jobs a month, but that assumes I am way off on the education component. If the economy does add 160,000 private jobs a month, depending on government cutbacks, the unemployment rate will barely drop, and in fact might not even drop at all. At +100,000 to +125,000 total jobs a month, the unemployment rate will likely rise. Given all the tremendous risks, the economy might not add that. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment