Mish's Global Economic Trend Analysis |

- Czech Republic Enters Currency Debasement Club; Koruna Intervention Triggers Record Drop; "Hardball" in Pictures

- Euro Swings Significantly, Gold Dips Following ECB Rate Cut Announcement; US Tapering Coming Up?

- ECB Unexpectedly Cuts Rate to .25%; Draghi Promises Loose Policy for "Extended Period", "Ready to Consider All Instruments"; What Debasement is Next?

| Posted: 07 Nov 2013 05:23 PM PST Currency madness has spread to the Czech Republic. Central bank intervention triggered a record plunge in the Koruna vs. the Euro. Bloomberg reports Czechs Play Koruna Hardball as Intervention Triggers Record Drop The Czech central bank's return to currency interventions after 11 years heralds a push for a weaker koruna to ward off deflation and kick-start the economy.Hardball in Pictures - Koruna vs. Euro  It seems the "ideal" level of 27 was reached in a day. Of course it is preposterous to propose that anyone, especially central banks have any notion of what the "ideal" level is. From a consumer standpoint, the more European goods Czech citizens can buy with the Koruna the better. But central banks will have none of that. About That Eurozone Entry Wikipedia comments on the Czech Republic Plans to Join the Eurozone. The Czech Republic planned to adopt the euro in 2012, but its government suspended that plan in 2007. Although the country is economically well positioned to adopt the euro, there is considerable opposition to the move within the Czech Republic. According to a survey conducted in January 2011, only 22% of the Czech population was in favour of replacing the koruna with euro.One alleged disadvantage of joining the eurozone is giving up the ability to do what the Czech Republic just did. Of course the ECB is on its own currency debasement mission vs. the US dollar and Japanese Yen as noted in ECB Unexpectedly Cuts Rate to .25%; Draghi Promises Loose Policy for "Extended Period", "Ready to Consider All Instruments"; What Debasement is Next? Where Does It End? For years, I have been asking supporters of these competitive currency debasement schemes "where does it end"?

Recently, Ambrose Evans-Pritchard at the Telegraph proposed the ECB devalue the Euro to support growth and end deflation. For further details, please consider Lunatic Howls for Competitive QE Debasement; Another Swan Dive Into Cesspool of Economic Silliness; Following Lemmings Over The Cliff; It's Madness! How the hell can competitive devaluation work, when every country can "theoretically print as much currency as it wants" and every country wants a declining currency vs. every other currency to support growth? Ambrose, I am still waiting for the answer to that question. Given that Ambrose (and every other misguided monetarist on the planet) proposes a mathematical impossibility, I may be waiting for a long time. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

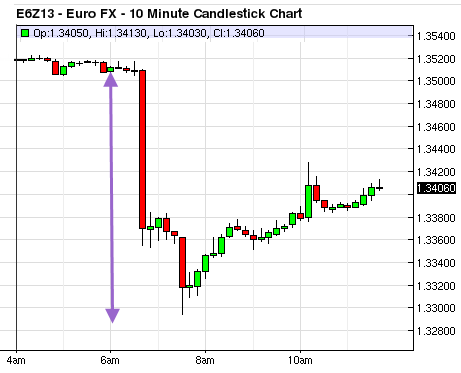

| Euro Swings Significantly, Gold Dips Following ECB Rate Cut Announcement; US Tapering Coming Up? Posted: 07 Nov 2013 10:41 AM PST Here is a 10-minute Euro chart that shows wild swings following the Unexpected ECB Decision to lower rates today. 10-minute Euro Chart  The Euro swung 2 cents vs. the US dollar but has now regained about half of the move.On a percentage basis, these are substantial swings. 10-minute Gold Chart  Charts from Barchart. Gold fell about $30 following the ECB announcement and has taken back about a third of the decline. US Tapering Coming Up? Is competitive currency debasement bad for gold? It shouldn't be. Likely, this is more of an over-reaction to the still-lingering belief that the Fed is going to taper. How likely is that? Not very according to Bloomberg columnist Caroline Baum in her article today A GDP Report in Search of Liftoff While real GDP increased 2.8 percent in the third quarter, inventories accounted for almost a third of the growth. Consumer spending added 1 percentage point and net exports 0.3 percentage point. Real final sales, which is GDP less inventories, rose 2 percent, close to the trend since the recession ended in June 2009. Final sales to domestic purchasers, which excludes exports and includes imports, rose a meager 1.7 percent.Should vs. Will are Horses of a Different Color Given the huge asset bubbles in equities and corporate bonds, the Fed ought to be tapering now. Then again, given that repetitive bubble blowing never makes any sense, the Fed should never have launched three rounds of QE in the first place. But what the Fed "should" do and what the Fed "will" do are horses of a different color. Baum is highly likely correct in her assertion "tapering asset purchases isn't in the cards any time soon." Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Posted: 07 Nov 2013 09:22 AM PST The ECB did the unexpected today, cutting the interest rate to .25% from .50%. Here is the ECB press release. 7 November 2013 - Monetary policy decisionsNews Conference Text Bloomberg has the ECB President Draghi News Conference Text. Here are a few key snips.

What Debasement is Next? It could be anything. Here is the key sentence: "We are ready to consider all available instruments, and, in this context, we decided today to continue conducting the main refinancing operations as fixed rate tender procedures with full allotment for as long as necessary, and at least until the end of the 6th maintenance period of 2015, more precisely on July 7, 2015." The currency cranks calling for more debasement got their wish today. But given the ECB did not do everything at once, and is only "ready to consider all available instruments", I doubt the cranks will be satisfied. For further discussion, please see Lunatic Howls for Competitive QE Debasement; Another Swan Dive Into Cesspool of Economic Silliness; Following Lemmings Over The Cliff; It's Madness! Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment