Mish's Global Economic Trend Analysis |

- Detroit Files Chapter 9 Bankruptcy; Oakland, LA, Others on Deck; Pension Promises vs. Bondholders in Spotlight; The Bright Side

- Survey on Impact of Obamacare on Corporate Hiring; Businesses Far More Pessimistic vs. March

- Loosen This Tighten That

- European Car Sales Plunge to 20-Year low

| Posted: 18 Jul 2013 06:19 PM PDT In an inevitable, anticlimactic decision today, Detroit files for bankruptcy. Detroit became the largest US city to ever file for bankruptcy on Thursday, seeking protection from its creditors as it restructures more than $18bn in debt.Welcome to Chapter 9, Detroit FT Alphaville says Welcome to Chapter 9, Detroit Beyond the list of derelict buildings and brownfield sites owned by the city — you'll want to read the approval letter by Michigan Governor Rick Snyder, in Exhibit A. Here is a link to Detroit's Bankruptcy Filing Amusing Flashback of the Day The amusing flashback of the day with a hat tip to ZeroHedge goes to a CBS news headline from October 13, 2012 Obama: I "refused to let Detroit go bankrupt". Gut Kick Bloomberg says Detroit 'Gut Kick' Poses New Test for Long Suffering City The move was inevitable, said Steven Rattner, a New York financier who headed President Barack Obama's auto-industry task force in 2009 that put the predecessors of General Motors Co. and Chrysler Group LLC into bankruptcy reorganizations.10 Pages of Bankruptcy References on This Blog I have 10 pages of Detroit Bankruptcy References on this blog. The earliest is in regards to GM and is from 2005. Here are a few examples:

Clearly this is not a surprise. Nor did the stock market treat it like a surprise. What's going to be a surprise (but not to Mish readers) is when Oakland, LA, Houston, Baltimore, and numerous other cities declare bankruptcy to escape untenable pension and health-care promises. The Bright Side Taxpayers should be fed up with ever-escalating property taxes, sales taxes, and fees to pay ridiculous retirement plans for unappreciative public union employees, especially police, fire, and teachers' unions. So, look on the bright side. The Detroit bankruptcy is a good thing, and it will be even better when numerous other cities, bankrupted by public union greed, do exactly the same thing. If you are desperate for yield and holding questionable municipal bonds, especially long-term municipal bonds, you may wish to reconsider. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

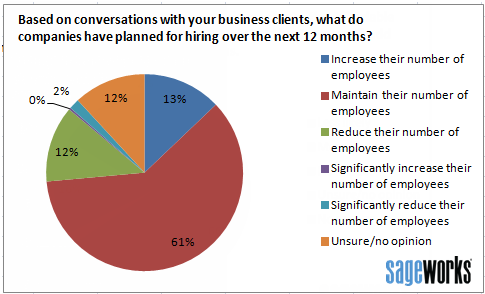

| Survey on Impact of Obamacare on Corporate Hiring; Businesses Far More Pessimistic vs. March Posted: 18 Jul 2013 03:10 PM PDT SageWorks conducted an interesting survey on corporate hiring plans of private businesses in March and again recently. Let's start with a look at results from the June 25 to July 16 survey, collecting responses from 300 accountants. Sageworks surveyed 300 accounting professionals who work closely with [privately held] firms and found that 66 percent expect the new health care changes will make it less likely that businesses will add new employees in the next year. Sixteen percent said it would have "no impact," and 14 percent of respondents said they were "unsure" about the ultimate impact. Only 2 percent said the Act makes it "more likely" that businesses will add new employees. Impact of Obamacare on Hiring Plans  "Private companies are performing well, but they're simply not hiring with the same volume and consistency that we'd expect from them at this point in the economic recovery," noted Sageworks Chairman Brian Hamilton. He continued, "The recent delay in the implementation of the Affordable Care Act, and the uncertainty that accompanies such a delay, won't help the employment situation. Private businesses are trying to map out their hiring and investment plans for the next twelve months, and a last minute delay like this will increase the likelihood that companies remain on the fence about hiring." Businesses More Pessimistic than in March Let's Compare the Current Survey to March Current Survey  March Survey  March vs. July

These survey results are not unexpected (by Mish readers), but the results likely are unexpected by economists and mainstream media writers. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Posted: 18 Jul 2013 10:55 AM PDT It's hard not to laugh at the ECB's latest attempt to stimulate lending to small and medium-sized entities (SMEs). Please consider ECB Changes Collateral Rules as It Seeks to Boost Lending. The Frankfurt-based ECB will reduce the risk premium, or haircut, applicable to asset-backed securities to 10 percent from 16 percent, according to an e-mailed statement today. It'll also lower the quality threshold for six ABS classes that are subject to loan-level reporting requirements to two A- ratings from two AAA ratings. At the same time, the central bank will tighten rules for retained covered bonds so the total effect on eligible collateral will be "overall neutral," it said.For starters, I rather doubt that the ECB has a clue as to what is really AAA. Next I point out the absurd assumption that sovereign bonds will not default when there have already been defaults and writedowns in Greece and Cyprus. I happen to think Spain and Portugal are next, with Italy not too far behind. Here's the key question: What is the point of lending to SMEs when the main problem is not funding but lack of customers? It seems to me that more lending is a sure path to more bank losses. And the banks are capital impaired (which of course is precisely why banks are not lending more in the first place). The only reason banks do not appear to be capital impaired is they do not have to mark all their assets to market. Finally, even if it made sense to stimulate lending to SMEs, is a mere reduction in collateral from 16% to 10% enough? If it is, I suggest it will expose the ECB to losses on its collateral. "Loosen This Tighten That" as a strategy to stimulate SME lending is ridiculous. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| European Car Sales Plunge to 20-Year low Posted: 18 Jul 2013 02:00 AM PDT Amidst all the happy talk that Europe is on the verge of some sort of recovery, here is yet another counterpoint: European Car Sales Plunge to 20-Year Low Despite hopes that the European market might have finally bottomed out, car sales for the first half of 2013 plunged to a 20-year low, according to industry data, with little sign that the downturn is about to reverse itself.As I said yesterday .... Expect the recovery to be "weaker than expected". Indeed, expect no recovery at all. Rather, expect Germany to contribute in a major way to the pending "unexpected" non-recovery, unless by some miracle European exports to Mars suddenly take off. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment