Mish's Global Economic Trend Analysis |

- EU officials Give Greece Three Days to Deliver Reforms or Face Consequences; The Eventual Outcome

- Ritholtz on Gold and on Making Predictions; How Secular Bull Markets End; Winning vs. Investing

- Credit Contraction Exceeds 6% in Spain, Highest Ever in Crisis

| EU officials Give Greece Three Days to Deliver Reforms or Face Consequences; The Eventual Outcome Posted: 02 Jul 2013 08:53 PM PDT Reuters reports Greece Has Three Days to Deliver Reforms or Face Consequences. Greece has three days to reassure Europe and the IMF that it can deliver on conditions attached to its bailout in order to receive its next tranche of aid, four euro zone officials said on Tuesday.The Eventual Outcome Given that Greece has caved in on every demand so far, it's certainly likely Greece will do so again, right now. But if Greece does not immediately cave in, then expect the Troika to grant more time until Greece does cave in. If by some remote chance, should Greece not cave in, then expect the Troika to slightly change its demands so that Greece will meet the demands. I actually prefer to be wrong about this. I would prefer Greece to tell the Troika "go to hell", then default. History suggests the odds that will happen "this time" are remote. However, somewhere along the line, and totally unexpected, Greece (or Portugal, or Spain, or Ireland, or Cyprus) will indeed have had enough of the Troika, then accept the consequences and default. I cannot predict the time, but I am quite certain of the eventual outcome. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

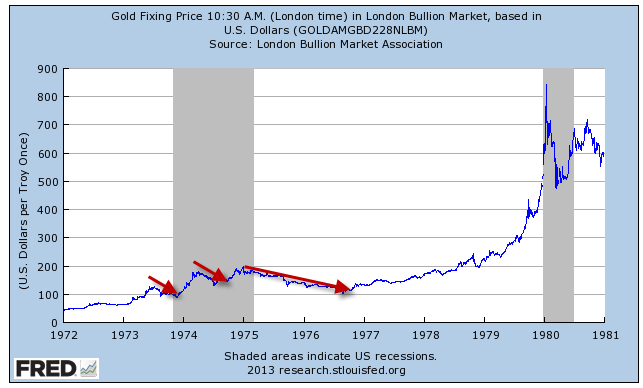

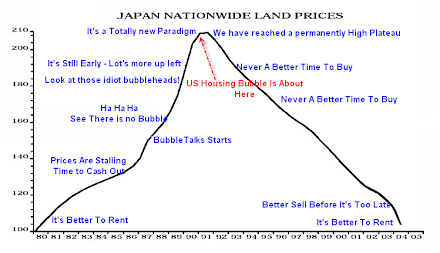

| Ritholtz on Gold and on Making Predictions; How Secular Bull Markets End; Winning vs. Investing Posted: 02 Jul 2013 11:59 AM PDT Folly of Forecasting Inquiring minds may be interested in this flashback from Barry Ritholtz originally written published June 2005 and republished March 27th, 2011 on The Folly of Forecasting. It's very easy for a confident-sounding analyst, fund manager or professor to say something on TV that can throw off the best laid plans of investors. Is Gold Overdue for a Bounce? One Day ago Barry Ritholtz pondered the question Is Gold Overdue for a Bounce? If you are a trader — and I no longer consider myself one — then you have to be wondering when Gold is going to bounce. It has plummeted on little inflation, a strong dollar and an improving economy. When the breathless narrative of hyper-inflation, collapsing fiat currency and end of the world failed to come about, Gold's spectacular rise ended.Don't Be Fooled; Sell Gold at $1,400, Then It's All Downhill, Says Ritholtz Today on Market Ticker Ritholtz says Sell Gold at $1,400, Then It's All Downhill. "I wouldn't be surprised to see a nice bounce in gold from this level up to $1400, $1440, but I don't know if it's sustainable after that." His advice to investors: "Hit the bid" once gold climbs to near $1400... $600 to $800 an ounce is certainly a possibility."Ritholtz was very careful to make his predictions sound like non-predictions while asserting the "gold bull market is over". Of course that assertion itself is another prediction. Gold Monthly Trendline  Whether or not the trendline is broken depends on how you draw it, but I suspect that even Ritholtz would have to admit the above interpretation is reasonable enough. And if the above trendline is intact, then it's impossible to say whether or not the secular bull market is over. Gold 1972-1981  Between 1972 and 1980 there were three selloffs of 30% or greater one of which was a 50% selloff. Was the gold bull market over? Certainly not the secular bull market. Is the secular bull market over now? I doubt it, but I suppose it's possible. Why do I doubt it? Because secular bull markets tend to end with public participation in a massive way and prices going parabolic. Here are some examples: Gold and silver in the 1980s, tech stocks in 2000, housing in 2005, the stock market in general in 2007 and arguably again (this time on the misguided belief the Fed has the markets back and nothing can go wrong). How Secular Bull Markets End Anyone recall Time Magazine going "gaga" over housing, using exactly that word on the cover? A Summer 2005 cover marked the secular peak in housing. What follows next is a repeat of my April 10, 2010 post US vs. Japan Land Prices Pictorial Update In Spring of 2005 I announced It's a Totally New ParadigmGrave Dancing Ritholtz claims to be agnostic regarding gold. I suggest his current hyperbole proves otherwise, even though he once liked the metal. For the record, Ritholtz is a good guy, we just happen to disagree regarding gold. And I certainly side with Ritholtz regarding the folly of $10,000 or even $3,000 gold predictions by hyperinflationists, especially when people put timeframes on them. But not every gold fan is a hyperinflationist or an inflationist of any kind. As a staunch deflationist, as well as someone who is definitely not agnostic regarding gold, I am proof enough. And who is it now that is coming out of the woodwork to dance on the grave of gold? It's a Plague of Gold Bears Now Say "Gold Unsafe at Any Price". What's the Real Long-Term Driver for Gold? Click on the preceding "Plague of Gold Bears" link to find out. Gold - The Despised Asset Class  In Gold We Trust The above chart is from the report In Gold We Trust by Incrementum AG Incrementum concludes (and I agree) ... We are firmly convinced that the fundamental argument in favor of gold remains intact. There exists no back-test for the current era of finance. Never before have such enormous monetary policy experiments taken place on a global basis. If there was ever a time when monetary insurance was needed, it is today.Is It Different This Time? Did the bull market end with bears coming out of the woodwork and gold's share of financial assets a mere 0.5%? Price Targets People keep asking, but I have no price targets for either gold or silver. Within a couple years, neither $1,000 nor $2,500 would shock me for the price of gold. However, history suggests the secular bull will not end without the public going gaga over the stuff. Winning vs. Investing Ritholtz says he no longer considers himself a trader. I am in the same camp. I consider myself an investor (with all the problems that entails, including the ups and downs of positioning for long-term trends). Cyclical bear markets make things tough, especially when a parade of bulls thinks the Fed can keep other asset classes levitated forever. Sometimes long-term positioning makes one look silly in the intermediate timeframe, and sometimes not. But I like my chances here with gold, whether or not "all the gold in Fort Knox is irradiated". I don't recall who first said this, but "If investing was easy, it would be called winning, not investing." Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Credit Contraction Exceeds 6% in Spain, Highest Ever in Crisis Posted: 02 Jul 2013 12:34 AM PDT According to prime minister Mariano Rajoy, Spain has been on the verge of recovery for two years. Rajoy has also promised to bring Spain's budget deficit to 3% of GDP for two straight years. And EU has extended the timeline for Spain to hit that goal from 2012 to 2013 to 2014 to 2015 and now to 2016. Last year Spain's budget deficit was 7.1% and the unemployment rate is nearly 27% with a youth unemployment rate over 56%. Spain's Misery Index Today we can add another piece to Spain's misery index. Via Google Translate, please consider Credit Contraction Exceeds 6% for First Time. Despite the efforts, or the good wishes of the Government, the day of the reopening of the credit tap still seems distant. According to the Bank of Spain, loans to the private sector residents, families and businesses have registered a fall of 6.1% in the month of May, the highest percentage in the entire crisis. Spain Lending Stats

And we are supposed to believe conditions are improving, recovery is just around the corner, and Spain will reduce its budget deficit to 3%. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment