| Obamacare "Observations" and the Elusive Search for Improvements; Seniors Beware! Posted: 02 Dec 2015 04:11 PM PST Obamacare "Observations"Team Obama brags that the readmission rate of patients to hospitals has been dropping. It has. And that was one of the goals of Obamacare. Are congratulations in order? Not exactly. Medicare enacts a penalty on hospitals that do not meet readmission goals. To meet the new goals, hospitals readmit patients, but they don't label it " readmission", they label it " observation". Elusive Search for Improvements The Wall Street Journal explains how Medicare Rules Reshape Hospital Admissions. At Banner Health's general hospitals, the rate of heart-failure patients who wind up admitted to the hospital again soon after leaving has been dropping significantly, according to a Wall Street Journal analysis of Medicare billing data. So has the readmission rate for patients treated for pneumonia and three other serious conditions.

The Obama administration has cast such results as a triumph of the Affordable Care Act, which penalizes hospitals that have too many readmissions within 30 days of an inpatient stay. The goal is to encourage better follow-up treatment so patients can stay out of the hospital—keeping them in better health and whittling down the cost to the government.

But this seemingly good news isn't as encouraging as it appears. At Banner, based in Phoenix, and at hospitals around the country, more patients are entering or re-entering hospitals under something called "observation status"—a category that keeps them out of the readmission tallies.

Patients on observation status can remain in the hospital for days, and typically receive care that is indistinguishable from inpatient stays, experts say. But under Medicare billing rules, the stays are considered outpatient visits, and as such, don't trigger penalties under the health law.

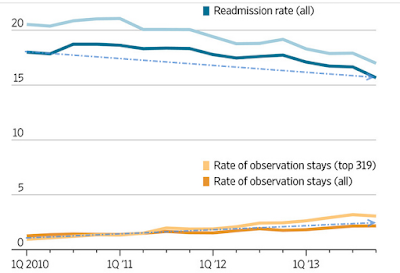

The Journal's analysis of Medicare billing data shows that increases in observation stays can skew the readmission numbers, letting hospitals avoid penalties even if patients continue to have complications and return for repeat visits. Readmissions vs. Observations The above chart shows the top 319 hospitals compared to all the hospitals. For the top 319 hospitals and all hospitals in aggregate, readmission rates fell while "observation" rates rose. Who Pays for Obamacare "Observations"? Medicare does not pay for observations. If patients don't spend three days under formal inpatient admission in the hospital, the federal program won't pay for a subsequent nursing-home stay. So patients pay out of pocket, and it can be very costly. Shocking? "We were shocked," said Bob Wellentin, 87 years old, a retired teacher in Puyallup, Wash., who said he had never heard of observation stays before his wife spent four days in a hospital after a fall in June 2014. She recuperated for more than two months in a nursing home, costing the couple more than $20,000, according to billing records and receipts. To pay the bills, the couple liquidated a life-insurance policy and cashed in certificates of deposit set aside to pay for their burials. Seniors Beware!Please note that the Wellentin case does not even appear to be a readmission, but rather an initial stay after a fall! That increases the need for awareness. Make sure you are being " admitted, not observed". The difference can set you back $20,000 or more. Shocking or not, I strongly suspect we still have not seen the end of these types of " improvement" revelations by the Obama administration. Mike "Mish" Shedlock |

| Yellen Yap: Dollar Briefly Takes Out March High, Surging to Level Last Seen March 2003; For What It's Worth Posted: 02 Dec 2015 12:37 PM PST As Fed Chair Janet Yellen yapped about the strength of the US economy in a speech to the Economic Club of Washington, the US dollar index briefly surged above a level set in March, to a high last seen in April of 2003. US Dollar Weekly As noted by the last red candle, the US dollar index is now down for the week. The last time the dollar touched as high as it did today was in March of 2003. US Dollar Monthly Speech Highlights Speech HighlightsThank you to the Economic Club of Washington for inviting me to speak to you today. I would like to offer my assessment of the U.S. economy, nearly six and half years after the beginning of the current economic expansion, and my view of the economic outlook.

The U.S. economy has recovered substantially since the Great Recession. The unemployment rate, which peaked at 10 percent in October 2009, declined to 5 percent in October of this year. At that level, the unemployment rate is near the median of FOMC participants' most recent estimates of its longer-run normal level. The economy has created about 13 million jobs since the low point for employment in early 2010, and total nonfarm payrolls are now almost 4-1/2 million higher than just prior to the recession.

I anticipate continued economic growth at a moderate pace that will be sufficient to generate additional increases in employment, further reductions in the remaining margins of labor market slack, and a rise in inflation to our 2 percent objective. I expect that the fundamental factors supporting domestic spending that I have enumerated today will continue to do so, while the drag from some of the factors that have been weighing on economic growth should begin to lessen next year. Although the economic outlook, as always, is uncertain, I currently see the risks to the outlook for economic activity and the labor market as very close to balanced.

Turning to the factors that have been holding down growth, as I already noted, the higher foreign exchange value of the dollar, as well as weak growth in some foreign economies, has restrained the demand for U.S. exports over the past year. In addition, lower crude oil prices have reduced activity in the domestic oil sector. I anticipate that the drag on U.S. economic growth from these factors will diminish in the next couple of years as the global economy improves and the adjustment to prior declines in oil prices is completed.

Although developments in foreign economies still pose risks to U.S. economic growth that we are monitoring, these downside risks from abroad have lessened since late summer. Among emerging market economies, recent data support the view that the slowdown in the Chinese economy, which has received considerable attention, will likely continue to be modest and gradual. China has taken actions to stimulate its economy this year and could do more if necessary. A number of other emerging market economies have eased monetary and fiscal policy this year, and economic activity in these economies has improved of late. Accommodative monetary policy is also supporting economic growth in the advanced economies. A pickup in demand in many advanced economies and a stabilization in commodity prices should, in turn, boost the growth prospects of emerging market economies.

A final positive development for the outlook that I will mention relates to fiscal policy. This year the effect of federal fiscal policy on real GDP growth has been roughly neutral, in contrast to earlier years in which the expiration of stimulus programs and fiscal policy actions to reduce the federal budget deficit created significant drags on growth.

Regarding U.S. inflation, I anticipate that the drag from the large declines in prices for crude oil and imports over the past year and a half will diminish next year. With less downward pressure on inflation from these factors and some upward pressure from a further tightening in U.S. labor and product markets, I expect inflation to move up to the FOMC's 2 percent objective over the next few years. Of course, inflation expectations play an important role in the inflation process, and my forecast of a return to our 2 percent objective over the medium term relies on a judgment that longer-term inflation expectations remain reasonably well anchored. In this regard, recent measures from the Survey of Professional Forecasters, the Blue Chip Economic Indicators, and the Survey of Primary Dealers have continued to be generally stable. The measure of longer-term inflation expectations from the University of Michigan Surveys of Consumers, in contrast, has lately edged below its typical range in recent years. However, this measure often seems to respond modestly, though temporarily, to large changes in actual inflation, and the very low readings on headline inflation over the past year may help explain some of the recent decline in the Michigan measure.

Let me now turn to the implications of the economic outlook for monetary policy.

In the policy statement issued after its October meeting, the FOMC reaffirmed its judgment that it would be appropriate to increase the target range for the federal funds rate when we had seen some further improvement in the labor market and were reasonably confident that inflation would move back to the Committee's 2 percent objective over the medium term. That initial rate increase would reflect the Committee's judgment, based on a range of indicators, that the economy would continue to grow at a pace sufficient to generate further labor market improvement and a return of inflation to 2 percent, even after the reduction in policy accommodation. As I have already noted, I currently judge that U.S. economic growth is likely to be sufficient over the next year or two to result in further improvement in the labor market. Ongoing gains in the labor market, coupled with my judgment that longer-term inflation expectations remain reasonably well anchored, serve to bolster my confidence in a return of inflation to 2 percent as the disinflationary effects of declines in energy and import prices wane.

Committee participants recognize that the future course of the economy is uncertain, and we take account of both the upside and downside risks around our projections when judging the appropriate stance of monetary policy. In particular, recent monetary policy decisions have reflected our recognition that, with the federal funds rate near zero, we can respond more readily to upside surprises to inflation, economic growth, and employment than to downside shocks. This asymmetry suggests that it is appropriate to be more cautious in raising our target for the federal funds rate than would be the case if short-term nominal interest rates were appreciably above zero. Reflecting these concerns, we have maintained our current policy stance even as the labor market has improved appreciably.

However, we must also take into account the well-documented lags in the effects of monetary policy. Were the FOMC to delay the start of policy normalization for too long, we would likely end up having to tighten policy relatively abruptly to keep the economy from significantly overshooting both of our goals. Such an abrupt tightening would risk disrupting financial markets and perhaps even inadvertently push the economy into recession. Moreover, holding the federal funds rate at its current level for too long could also encourage excessive risk-taking and thus undermine financial stability.

It is thereby important to emphasize that the actual path of monetary policy will depend on how incoming data affect the evolution of the economic outlook. Stronger growth or a more rapid increase in inflation than we currently anticipate would suggest that the neutral federal funds rate is rising more quickly than expected, making it appropriate to raise the federal funds rate more quickly as well; conversely, if the economy disappoints, the federal funds rate would likely rise more slowly. Given the persistent shortfall in inflation from our 2 percent objective, the Committee will, of course, carefully monitor actual progress toward our inflation goal as we make decisions over time on the appropriate path for the federal funds rate. For What It's WorthIn the "For What It's Worth" category, that's what Yellen believes. Q: What's it worth? A: Absolutely nothing. A seven-year recovery is quite long by any reasonable measurement stick. Inflation targets are very damaging. In striving to hit those targets the Fed blew huge asset bubbles once again, while bragging about being diligent about "excessive risk taking". The number of jobs did indeed take out the 2007 high, not because of Fed policy, but primarily because of population growth. US fiscal policy and deficit spending is a wreck waiting to happen. Inflation expectations are meaningless. And this recovery is the weakest on record. 2% growth has been the norm. Finally, the idea that a bunch of bureaucrats can divine where interest rates should be is absurd. Bubbles of increasing amplitude over time, for which the Fed has never apologized, are proof enough. Mike "Mish" Shedlock |

| Triumph of Trumpism and LePenism; Waiting for a Volunteer Mouse Posted: 02 Dec 2015 11:10 AM PST Waiting for a Volunteer Mouse Recall the tale of the mouse who had a brilliant idea to tie a bell on a the cat's tail so they would know when the cat was around? The mouse who hatched the plan called for volunteers. No one stepped up. And so it is with the Republican party. Everyone sees the need to take on a cat named Trump, but no volunteers can be found. Cat and Mouse GameThe New York Times phrases the cat and mouse game this way: Wary of Donald Trump, G.O.P. Leaders Are Caught in a Standoff. For months, much of the Republican Party's establishment has been uneasy about the rise of Donald J. Trump, concerned that he was overwhelming the presidential primary contest and encouraging other candidates to mimic his incendiary speech. Now, though, irritation is giving way to panic as it becomes increasingly plausible that Mr. Trump could be the party's standard-bearer and imperil the careers of other Republicans.

From Our Advertisers

Many leading Republican officials, strategists and donors now say they fear that Mr. Trump's nomination would lead to an electoral wipeout, a sweeping defeat that could undo some of the gains Republicans have made in recent congressional, state and local elections. But in a party that lacks a true leader or anything in the way of consensus — and with the combative Mr. Trump certain to scorch anyone who takes him on — a fierce dispute has arisen about what can be done to stop his candidacy and whether anyone should even try.

That has led to a standoff of sorts: Almost everyone in the party's upper echelons agrees something must be done, and almost no one is willing to do it.

"You have to deal with Trump berating you every day of the week," explained a strategist briefed on the thinking of both groups [hedge fund billionaire Paul Singer and another led by the industrialists Charles G. and David H. Koch].

"I think it would play into his hands and only validate him," said Senator Lamar Alexander, Republican of Tennessee. "A 'Stop Trump' effort wouldn't work, and it might help him." Triumph of TrumpismFinancial Times writer Edwards Luce proclaims Trumpism has Triumphed, Whoever Wins the Republican Nomination. Sinclair Lewis, the American novelist, is supposed to have said: "When fascism comes to America it will be wrapped in the flag and carrying the cross". It has long been easy — far too easy — to write off Donald Trump as a self-promoting celebrity with little chance of winning the White House. His chances remain low (Nate Silver, the guru of election data, puts them at 10 per cent, which is nevertheless five times more than when he started). But our lens is still too rosy. Whether Mr Trump defies the odds, or eventually fizzles out, is beside the point. The outrageousness of his success has paved the way for others to try. Mr Trump's invective has disrupted the character of US politics. It will be hard to change.

For proof of that, look no further than Mr Trump's "moderate" rivals in the Republican race. Instead of offering an alternative, mainstream candidates are moving ever closer towards Mr Trump's nativism. Jeb Bush, the original establishment favourite, now believes the US should only accept Syrian refugees if they are Christian. This year Mr Bush referred to children of undocumented aliens as "anchor babies" — so named because the illegal immigrants allegedly come to the US to ensure their unborn will have citizenship. Contrast this to what he said in February before Mr Trump entered the race: "We should welcome all immigrants," Mr Bush told the Chicago Council on Global Affairs. "[As Americans] we come in 34 different flavours."

Chris Christie, the ultimate moderate, since he governs the Democratic state of New Jersey, believes the US should accept no Syrian refugees at all regardless of religious background, even if they are "three-year-old orphans".

Meanwhile, John Kasich, the governor of Ohio, and ultimate insider, last week said that the US should set up a federal agency to promote Judeo-Christian values. Until Mr Trump, most Republicans rejected the "clash of civilisations" view of the world. Now it is normal.

With rivals such as this, does Mr Trump need friends? It will become ever harder for the likes of Messrs Bush, Christie and Kasich to disown what they have said. All three have tried to qualify their various Trumpist lapses. But such straying is occurring more often and few notice their qualifications. Moreover, their self-editing reinforces Mr Trump's contention that the Republican establishment is run by a bunch of mealy-mouths who lack conviction.

One lesson of Mr Trump's rise is that voters reward clarity. Having already muddied the waters, moderates are in little position to bring Mr Trump down when they think he goes too far. Last week, Mr Trump said there should be a database of Muslim Americans. He even hinted that they should carry identity cards. Few paid attention to his rivals' tut tutting. The Republican establishment is paralysed with fear. Appeasing him makes him worse. ... His brand of politics has already been validated. Triumph of LePenismIn France, voters on the left and center-right think Marine Le Pen's National Front (FN) party would be a disaster for the country. FN has never won a regional election. Care to guess who is leading the polls? Breitbart reports Marine Le Pen And Front National Surge In French Regional Elections. Ms. Le Pen is now the overwhelming favourite to capture north-western France and the Marseille-Nice region in elections set for the next two weekends, according to polls published yesterday. Such is the backing for the party that it might harvest as many votes as its conservative and centrist rivals combined.

The FN is also running neck-and-neck with Nicolas Sarkozy's centre-right party, Les Républicains, in the Burgundy-Franche-Comté region in eastern France.

A series of regional polls by BVA on Sunday, and published by the Independent, showed the FN gaining between 4 and 7 per cent compared to similar polls before the terrorist assault on Paris.

The FN has never won a regional government before. The regional elections are the first political test for French President Francois Hollande since the Nov. 13 terrorist attacks in Paris that killed 130 people. With the country reeling from that violence and grappling with border controls, FN candidates are showing "a significant increase" in support across the country, BVA said.

The FN would get 28 per cent of votes in the first round of elections starting Saturday, the same as a combination of parties including the Republicans and the centrist MoDem, according to an Ifop opinion poll published in Le Journal du Dimanche newspaper.

Her opponents try and define her message as "racist" and "xenophobic" when she says: "The absolute rejection of Islamic fundamentalism must be proclaimed loudly and clearly" but voters are listening in ever increasing numbers.

Ms. Le Pen would become a representative for the North Pas de Calais-Picardie region if the latest polls prove correct. Her niece, Marion Maréchal-Le Pen, is the party's candidate to lead the Provence-Côte d'Azur region. Le Pen Blasts EURT reports Marine Le Pen blasts EU for 'Blind Relationship with Islamist States'Marine Le Pen, the leader of the French National Front party, has slammed the EU's handling of foreign and migrant policy, saying that current problems in France stem from a lack of foresight in geopolitics and 'blind conformity in relations with Islamist states.'

Le Pen said that problems in France are rooted in the country's "crazy immigration policy, made without discernment, and with the abandoning of the principle of assimilation."

Le Pen went on to remark that "clandestine people and those who spread hatred should be systematically expelled to their countries of origin."

"The government and its president are confined to symbols. They don't fear a paradox when they call people to wave the national flag, to invoke the nation but always appeal to post-national logic, meaning anti-national from Brussels."

Le Pen is currently on trial in Lyons facing hate speech charges for comments made at a rally in 2010, when she compared Muslims praying in the streets to the Nazi occupation. She has denied any wrongdoing, but could face up to a year in prison if found guilty of inciting racial hatred. Middle Ground Anywhere?Voters in the US have to choose between the likes of Clinton (who will carry on Obama's open door refugee policy), and someone like Donald Trump, or even worse yet, John Kasich, the governor of Ohio, who said the US should set up a federal agency to promote Judeo-Christian values. In Germany, Merkel's open door policy has led to " Peak Merkel" and increasing support for the Euroskeptic, anti-immigration AfD party. Even members of Merkel's party are fed up with her stance. In France, the established parties are waiting for someone to take on Le Pen, while increasingly promoting anti-immigration policies she supports. Not a mouse can be found in the US or in France, willing to tie a warning bell on the lead cat's tail. Voters are caught in the middle, having to choose between extreme candidates on every issue from abortion to immigration to war-mongering to torture. Trump's increasingly extreme message, coupled with his announcement he supports totally discredited torture procedures such as waterboarding, makes Trump hard to take? But what is the alternative? The ChoiceAnd that's just one issue. Do you want Warmonger Clinton on the left? Warmongers Cruz, Rubio, or Graham, on the right? Abortion with no restrictions? No abortions at all? Extremism Sells In retrospect, it's not so much a triumph of Trumpism, but rather a triumph of extremism on nearly every issue, on both sides of the aisle. There is not much of a middle ground on anything. Immigration just happens to be the hot button at the moment. None of the AboveMy preferred choice would be a Libertarian like Ron Paul. But a middle-of-the-road candidate with moderate views on tax hikes, spending cuts, welfare, military spending, abortion, etc., would likely win a presidential election by a landslide except for one not-so-small problem: only extreme candidates can get nominated. Mike "Mish" Shedlock |

No comments:

Post a Comment