Mish's Global Economic Trend Analysis |

- Two Important Points on the Yield Curve and Spreads

- Fed Funds Effective Rate Shows Fed Did Indeed Hike by 25 Basis Points

- Kansas City Manufacturing Region Back In Contraction, Employment in Severe Contraction

- Yield Curve and Spreads: Fed's Real Policy Error in Pictures; What's Next?

| Two Important Points on the Yield Curve and Spreads Posted: 18 Dec 2015 12:15 PM PST In my post this morning on Yield Curve and Spreads: Fed's Real Policy Error in Pictures; What's Next? there were two important points I intended to make but didn't. First here's a repeat of two charts. Yield Curve 1998-2015 (Year-End Values)  Click on either chart for sharper image. Values for 2015 are from the December 16 close, the day the Fed hiked. Yield Curve Differentials 1998-2015 (Year-End Values)  Two Important Points

If the economy was strengthening as widely believed, the yield curve ought to be widening, not collapsing. Greenspan's first hike in four years was on 2004-06-30. Check out the yield curve and differentials ahead of and right after that hike. Compare to today. Those who believe the yield curve must invert before a recession hits, need think about those two important points in addition to taking a look at recession in Japan. A recession without a preceding yield curve inversion has not happened in the US before, but neither have yield spread differentials collapsed in the initial stages of a Fed tightening cycle. Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Fed Funds Effective Rate Shows Fed Did Indeed Hike by 25 Basis Points Posted: 18 Dec 2015 11:16 AM PST I was on record stating a belief the Fed would effectively hike by 1/8 point. I had that belief because that is what the Fed Fund Futures implied. Regardless, I was wrong. If someone is going to prove you wrong it may as well be yourself. Here is a table of Effective Fed Funds Rates straight from the New York Fed. I created the table from their downloadable data. Effective Fed Funds Rate

Previous effective rates hovered around 12.5 basis points. That is 1/8 of a point. A quarter-point (25 basis points) hike would have been to 37.5. An eighth-of-a-point hike would have been to 25 basis points. Today we are at 37. Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Kansas City Manufacturing Region Back In Contraction, Employment in Severe Contraction Posted: 18 Dec 2015 10:37 AM PST The Kansas City manufacturing index is back in contraction as expected in this corner after a brief wonderland experience last month that took the diffusion index to +1. Economists don't guess about this region, so let's dive into the details straight from the 10th District Fed Report.  . .The first three columns show the Fed surveys about 100 manufacturing companies. The diffusion index is formed by subtracting the number of companies with a decrease from the number of companies with an increase. The last column is a seasonal adjustment. The bad news in manufacturing goes on, and on, and on. This is the eighth contraction in nine months. Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

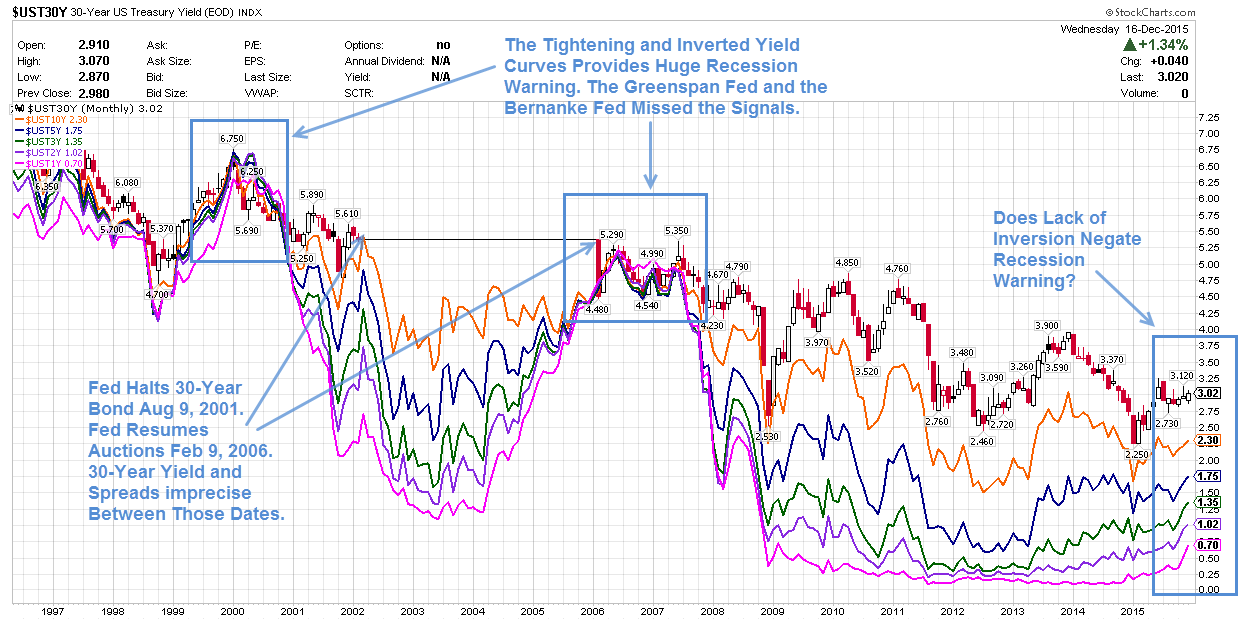

| Yield Curve and Spreads: Fed's Real Policy Error in Pictures; What's Next? Posted: 18 Dec 2015 01:38 AM PST Inquiring minds may be interested in a detailed look at the yield curve and spreads between various durations following the Fed's Wednesday rate hike. Let's start with a long-term chart from 1996 to 2015. Yield Curve 1996-Present  click on any chart for much sharper image Legend

Notes

Spotlight on Spreads and Inversions It is very difficult to see spreads and inversions over such a long duration in the above chart. There are simply too many data points. For ease in viewing, I took year-end closing numbers (except the current year which is as of close on December 16, the day of the hike), and plotted them in Excel. Yield Curve 1998-2015 (Year-End Values) Yield Curve Differentials 1998-2015 (Year-End Values) Bubbles of Increasing Amplitude Over Time In the above chart, my statement "Fed's Real Policy Error is to Encourage Massive Speculation, First in Housing, then Everywhere. Bubbles Reblown, Only Bigger" is a play on John Hussman's post this week entitled Deja Vu: The Fed's Real "Policy Error" Was To Encourage Years of Speculation. Unfortunately, here we are again. The Fed has blown another bubble at least as big as the bubble in 2007 and 2000. A friend recently commented something along the lines "there is no way this is bigger than the 2000 bubble". Actually, it is bigger in many ways. While it's true the dotcom bubble had huge numbers of stocks that went completely bust and never recovered, that bubble was predominantly centered around technology. Energy, mining, consumers staples, and non-technology smallcaps were not in bubble territory. In 2007, housing and financials were in a massive bubble. Today, valuations are stretched nearly everywhere you look except mining and energy. Median P/E ratios are at an all-time high. For details please see Stocks More Overvalued Now Than 2000 and 2007 No Matter How You Look at Things. What's Next? "What's next?" is a key question that everyone seems to be asking. Yet, in aggregate, market participants do not seem concerned about the obvious bubbles and likely answers. Many think that a recession cannot be on the horizon because the yield curve is not inverted. However, Japan proves otherwise. Things change at zero bound. Although the belief that rates cannot go negative has been shattered, I do not ever expect to see the day when 10-year yields are even more negative than 3-month yields. Four More Hikes Coming? Are four more hikes coming in 2016? I doubt that, but see Saxo Bank's Real Forecast for 2016; Mish Comments and Projections for a differing opinion. Meanwhile, watch that yield curve carefully. If the Fed hikes and the curve inverts, immediately kiss the recovery goodbye. If the Fed does not get in its stated hikes, it will likely be because the Fed is worried about a recession that is long overdue and already baked in the cake. Finally, for everyone who thinks the economy is about to take off, please explain ....

If you think manufacturing is no longer relevant, please think again. Mike "Mish" Shedlock |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment