| Spanish Election: Two-party Dominance Ends; Rojoy's PP Party Fails to Win Majority; Vote Buying Spanish Style; Fragile Coalition Possibilities Posted: 20 Dec 2015 03:42 PM PST Spanish Election ResultsMariano Rajoy may be the first leader of a country to be re-elected having imposed harsh austerity measures, but he will either need to find a coalition partner, or form what is likely to be a fragile minority government. There are 350 Seats in the Spanish legislature and the results look like this. - People's Party (Conservatives): 122 seats, 28% of vote

- PSOE (Socialists): 93 seats, 22% of Vote

- Podemos (Eurosceptic, Anti-Austerity Socialists): 69 seats, 20.5% of vote

- Ciudadanos (Anti-corruption, nationalistic party): 28 seats, 14% of vote

This result complicates things greatly. Many expected PP and Ciudadanos would have enough seats form a majority. Ciudadanos had been polling above 20% with Podemos sinking. Like PP, Ciudadanos is very much against the separatists in Catalonia, and very pro-euro. But 122 + 28 does not come close to the 176 needed for an outright majority. The socialists and conservatives could form a government, but how stable would that be? PSOE, Podemos, and Ciudadanos could in theory form a coalition but huge philosophical differences abound. Podemos is eurosceptic while Ciudadanos is very pro-Europe. In addition, Podemos is open to separatist elections and Ciudadanos would never go along. A minority government with Rajoy remaining in power is possible but that might not be stable either. Two-party Dominance EndsThe Guardian reports People's party wins Spanish election but without absolute majority. The PP and Socialists earned a combined vote share of around 50%, compared to the 70-80% in combined votes in past general elections. "The two-party political system is over and we are entering a new era in our country," Podemos' Iñigo Errejón said on Sunday as results began rolling in.

Podemos did notably well in Catalonia, suggesting widespread approval for its campaign promise to hold a referendum on independence for the north-eastern region. Preliminary results suggested a coalition backed by Podemos and Barcelona en Comú was poised to take first place in the region.

In order to be able to govern for the next four years, the PP will have to rely on other parties, suggesting a protracted process of negotiations lies ahead for political leaders.

Several scenarios are possible. The PP could form a minority government, particularly since Ciudadanos leader Albert Rivera said last week his party would abstain from a vote of confidence in order to allow the party with the most seats to govern. The scenario is a risky one for the PP, as a minority government could fall easily, triggering new elections.

"Reaching a deal between the Socialists, Ciudadanos and Podemos is not going to be straightforward ... but if the alternative is leaving the country without a government, the pressure will be on the parties," Federico Santi, a London-based analyst with the Eurasia Group, told the Associated Press. Vote Buying Spanish StyleRajoy, 60, remains the most popular option with Spaniards over the age of 55, buoyed in part by his party's consistent support for pensions. Even as his government was slashing spending for public wages, education and research, pensions were raised. Not only is this the demographic that is most likely to vote, it has also grown by more than a million people since the 2011 election, while those under the age of 34 years have dropped by almost a million. Spain's pension promises are not sustainable of course, but getting reelected always takes precedence over everything else, including economic realities. Mike "Mish" Shedlock |

| Why Does GDPNow Model Sometimes Move Counter to Economic Releases? Posted: 20 Dec 2015 12:06 PM PST I am sometimes puzzled as to why the Atlanta Fed GDPNow Model moves counter to what one would normally expect following economic news releases. For example, on December first, construction spending hit an 8-year high. On the same day the ISM was a huge disappointment. I expected the net overall result of those to be a small net minus, with construction adding to GDP and ISM subtracting. I commented on that idea in GDPNow Forecast for 4th Quarter Dips to 1.4% Following Weak ISM and Strong Construction Reports. Here are a few snips. Construction Spending Beats Estimates

The consensus estimate for construction spending was +0.6% but the actual month-over-month reading was +1.0%.

Construction Contribution to GDP

As noted earlier today, this morning's ISM report was a disaster. (See Manufacturing ISM Contracts; Lowest Reading Since June 2009; Glimmers of Hope Extinguished). But the construction report looked good.

Combined with ISM spending, I would have expected the net result of today's reports to be an overall small minus.

Actual GDPNow Forecast Results were dramatically different.

GDPNow Forecast Sinks 0.4 Percentage Points to 1.4 Percent.

Construction Subtracts From GDP vs. Prior Estimate

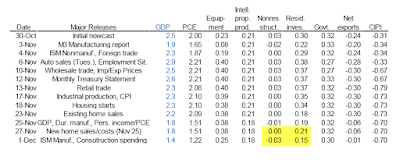

Compared to the November 27 report that included new home sales, construction appears to have subtracted approximately 0.09 percentage points and ISM roughly another 0.31 percentage points. Other reports in between may have contributed but those should be the main factors.

I have a question into the Atlanta Fed regarding construction contribution to GDP. My Question to Atlanta FedConstruction Spending was up 1% month-over-month today. I would have expected this to add to your GDPNow forecast.

Instead it subtracted.

Bloomberg Econoday made this comment: "The housing data in this report are not only favorable but the pop higher in related permits, in data previously released with the housing starts & permits report, hints at further gains ahead. This report points to a solid fourth-quarter contribution from construction."

Instead it appears the construction report subtracted 0.09 vs. the prior estimate. Can you explain?

Thanks

Mish Reply from Atlanta FedI received a reply from Patrick Higgins at the Atlanta Fed on December 8. I missed his reply as it somehow went into my spam bucket. Higgins writes ... Hi Mike,

This far away from the GDP release, the forecasts of nonresidential structures and residential investment depend importantly on an estimate of a dynamic activity factor very similar to the Chicago Fed National Activity Index (CFNAI). As of December 1, the estimate of that factor for November (and the forecast for December) was heavily influenced by the ISM Manufacturing Index since there was very little data for November released at that point. Like the CFNAI, the dynamic factor has mean 0, standard deviation 1. As of the GDPNow release on Nov 25, the model had forecasted values for the dynamic factor of -0.06 for November and -0.05 for December (i.e. both were essentially 0, or trend). These changed to -0.72 for November and -0.31 December after the data on December 1. Since then, the estimates of the dynamic factors for November and December have returned close to their November 25 readings. You can see these values in row 5 of the tabs Residential and NonresStructures of the Model. You can also see how they feed into forecasts of the monthly data but clicking the formula bar for any of the teal shaded cells. For example, cell FV9 of tab Residential.

If you simply replace the December 1st estimates of the dynamic factor with the estimates as of last GDPNow release on November 25th, the December 1 nowcast for residential investment growth becomes 6.5% [instead of 4.5%] and the December 1 nowcast for nonresidential structures investment growth becomes -0.4% [instead of -1.1%]. So the nowcasts for these components depend importantly on the dynamic factor even though that is not a direct input into GDP. Once we get closer to the GDP release, the dynamic factor becomes less important as the model relies more heavily on actual released data.

Pat Thanks Pat. That may be a bit complicated for most to follow, but it provides a nice explanation as to why the GDPNow model moves counter to what one might otherwise conclude on release of the data. By the way, I have found the folks at the Atlanta Fed as well as the BLS very helpful in answering questions like these. Mike "Mish" Shedlock |

No comments:

Post a Comment