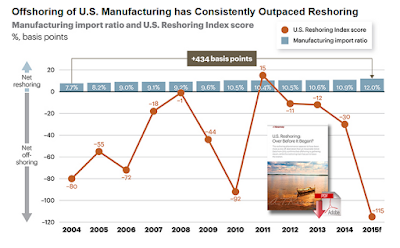

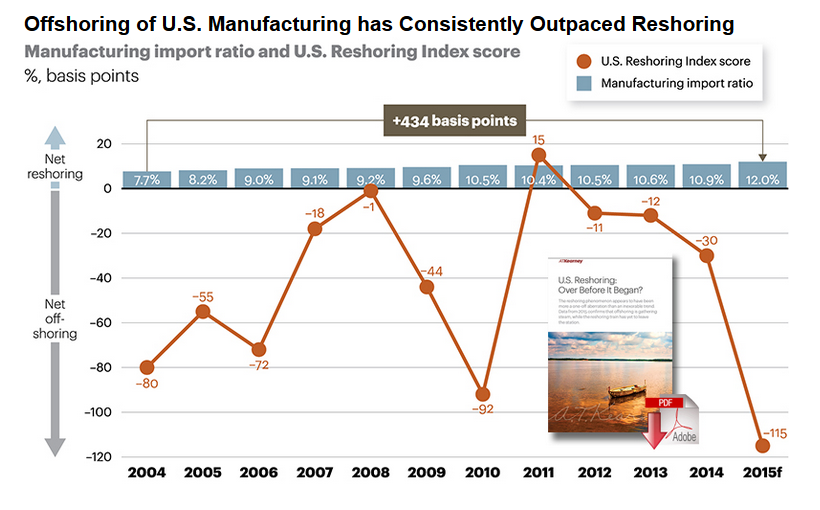

| Reshoring Myth Explodes: Ofshoring Opaces Onshoring Every Year Since 2004 Except 2011 Posted: 21 Dec 2015 11:00 PM PST Reshoring Over Before It Ever Got GoingRecall the hype over reshoring? Manufacturing jobs supposedly were returning to the US in droves from Asia. My view was that although some manufacturing processes returned, not many jobs came back thanks to robots and software automation. That view was far too optimistic. Reshoring Myth and RealityThe second annual A.T. Kearney U.S. Reshoring Index shows that for the fourth consecutive year, reshoring of manufacturing operations to the United States has once again failed to keep up with offshoring. Supply Chain reports 2015 U.S. Reshoring Index Indicates Manufacturing Reshoring Trend Has Subsided. In 2015 the A.T. Kearney U.S. Reshoring Index dropped to -115, down from -30 in 2014, and represents the largest year-over-year decrease in the last 10 years.

Even if the effect of raw material price declines is discounted by, conservatively, holding manufacturing input values constant relative to 2014 while ignoring that same effect on the value of offshore manufactured goods, the U.S. Reshoring Index would drop to -26, still supportive of the view that the widely predicted reshoring trend seems to be over before it started.

Patrick Van den Bossche, A.T. Kearney partner and co-author of the study, stated, "The U.S. Reshoring phenomenon, once viewed by many as the leading edge of a decisive shift in global manufacturing, may actually have been just a one-off aberration. The 2015 data confirms that offshoring seems only to be gathering steam, while the U.S. reshoring train that so many predicted has yet to leave the station."

Industries vulnerable to rising labor costs in China have been successfully relocating to other Asian countries, rather than returning to the United States. They have done so without incurring significantly higher supply chain costs, despite the weaker infrastructure and supporting ecosystems of these new low-labor-cost destinations. Vietnam has absorbed the lion's share of China's manufacturing outflow, especially in apparel. U.S. imports of manufactured goods from Vietnam in 2015 will be nearly triple the level of imports in 2010.

Study Findings

The A.T. Kearney U.S. Reshoring Index and the U.S. Reshoring Database provide a number of insights on the factors driving imports of offshore manufactured goods and manufacturing reshoring. Many of the report insights run counter to the points of view and "hype" regarding reshoring of manufacturing to the United States.

- Surprisingly, some of the top sectors for reshoring from 2011 to 2015 are also sectors that have led the pack in further offshoring over that same period.

- The recent increase of nearshoring to Mexico also seems to indicate that, even if U.S. companies consider leaving Asia, they may choose to stop south of the border.

- The forecast strengthening of the dollar, the oil price slide, the tightening U.S. labor market in manufacturing and the Trans-Pacific Partnership (TPP), if ratified by the U.S. Congress, will likely further weaken the case for reshoring in 2016.

- Although reshoring of manufacturing by U.S. companies is on the decline, non-U.S. companies, including Chinese companies, increasingly invest in establishing or expanding their manufacturing footprint in the United States. The insatiable U.S. consumer market, the stable political and economic environment, and the benefit of tapping into America engineering skills and manufacturing know-how are main draws.

America's Manufacturing Renaissance MythAlso consider The Myth of America's Manufacturing RenaissanceFor the casual observer, it is easy to get the impression that American manufacturing has entered a new and exciting period of revival.

Many in the media, along with consulting firms, think tanks, and economists, now proclaim the emergence of a U.S. "manufacturing renaissance," marked by the "reshoring" of production and the growing competitiveness challenges of many foreign nations vis-à-vis the United States. If only this were true.

The Myth of America's Manufacturing Renaissance: The Real State of U.S. Manufacturing, a new report by the Information Technology and Innovation Foundation (ITIF), assesses the true status of the American manufacturing economy and argues pundits have overestimated the impact of isolated incidents of reshored production and misread or ignored the data.

If there were a true renaissance, we'd expect to see growth in inflation-adjusted manufacturing value added. But in fact 2013 manufacturing value added is 3.2 percent below 2007 levels, with non-durable goods value-added (which includes chemicals and oil and gas) down almost 12 percent. U.S. manufacturers employ over a million fewer workers and there are 15,000 fewer manufacturing establishments since the beginning of the Great Recession. Moreover, America ran a $458 billion trade deficit in manufacturing goods in 2013. Hardly evidence of a renaissance.

And most of the recovery that has occurred has been cyclical in nature. In fact, 122 percent of manufacturing output growth between 2010 and 2013 was in the auto sector, whose growth is due almost solely to a rebound in U.S. consumer demand, rather than reshoring of automobile production.

"Most of the claims for a structural rebirth of U.S. manufacturing are unfortunately based on myths and anecdotes," states Robert Atkinson, President of ITIF and co-author of the report. "Instead, any assessment of U.S. manufacturing should be based on rigorous analysis and review of the official data." Prevailing Wisdom The first article, released December 21, 2015 is far more damning than the second, released January 14. Check out the prevailing wisdom in January: " One thing is clear - optimism about the future of U.S. manufacturing is relatively buoyant, as 68% of the executives surveyed agreed that U.S. manufacturing will experience accelerated growth in the next five years." A manufacturing recession has been upon us for six months. Mike "Mish" Shedlock |

| Reshoring Myth Explodes: Ofshoring Opaces Onshoring Every Year Since 2004 Except 2011 Posted: 21 Dec 2015 11:00 PM PST Reshoring Over Before It Ever Got GoingRecall the hype over reshoring? Manufacturing jobs supposedly were returning to the US in droves from Asia. My view was that although some manufacturing processes returned, not many jobs came back thanks to robots and software automation. That view was far too optimistic. Reshoring Myth and RealityThe second annual A.T. Kearney U.S. Reshoring Index shows that for the fourth consecutive year, reshoring of manufacturing operations to the United States has once again failed to keep up with offshoring. Supply Chain reports 2015 U.S. Reshoring Index Indicates Manufacturing Reshoring Trend Has Subsided. In 2015 the A.T. Kearney U.S. Reshoring Index dropped to -115, down from -30 in 2014, and represents the largest year-over-year decrease in the last 10 years.

Even if the effect of raw material price declines is discounted by, conservatively, holding manufacturing input values constant relative to 2014 while ignoring that same effect on the value of offshore manufactured goods, the U.S. Reshoring Index would drop to -26, still supportive of the view that the widely predicted reshoring trend seems to be over before it started.

Patrick Van den Bossche, A.T. Kearney partner and co-author of the study, stated, "The U.S. Reshoring phenomenon, once viewed by many as the leading edge of a decisive shift in global manufacturing, may actually have been just a one-off aberration. The 2015 data confirms that offshoring seems only to be gathering steam, while the U.S. reshoring train that so many predicted has yet to leave the station."

Industries vulnerable to rising labor costs in China have been successfully relocating to other Asian countries, rather than returning to the United States. They have done so without incurring significantly higher supply chain costs, despite the weaker infrastructure and supporting ecosystems of these new low-labor-cost destinations. Vietnam has absorbed the lion's share of China's manufacturing outflow, especially in apparel. U.S. imports of manufactured goods from Vietnam in 2015 will be nearly triple the level of imports in 2010.

Study Findings

The A.T. Kearney U.S. Reshoring Index and the U.S. Reshoring Database provide a number of insights on the factors driving imports of offshore manufactured goods and manufacturing reshoring. Many of the report insights run counter to the points of view and "hype" regarding reshoring of manufacturing to the United States.

- Surprisingly, some of the top sectors for reshoring from 2011 to 2015 are also sectors that have led the pack in further offshoring over that same period.

- The recent increase of nearshoring to Mexico also seems to indicate that, even if U.S. companies consider leaving Asia, they may choose to stop south of the border.

- The forecast strengthening of the dollar, the oil price slide, the tightening U.S. labor market in manufacturing and the Trans-Pacific Partnership (TPP), if ratified by the U.S. Congress, will likely further weaken the case for reshoring in 2016.

- Although reshoring of manufacturing by U.S. companies is on the decline, non-U.S. companies, including Chinese companies, increasingly invest in establishing or expanding their manufacturing footprint in the United States. The insatiable U.S. consumer market, the stable political and economic environment, and the benefit of tapping into America engineering skills and manufacturing know-how are main draws.

America's Manufacturing Renaissance MythAlso consider The Myth of America's Manufacturing RenaissanceFor the casual observer, it is easy to get the impression that American manufacturing has entered a new and exciting period of revival.

Many in the media, along with consulting firms, think tanks, and economists, now proclaim the emergence of a U.S. "manufacturing renaissance," marked by the "reshoring" of production and the growing competitiveness challenges of many foreign nations vis-à-vis the United States. If only this were true.

The Myth of America's Manufacturing Renaissance: The Real State of U.S. Manufacturing, a new report by the Information Technology and Innovation Foundation (ITIF), assesses the true status of the American manufacturing economy and argues pundits have overestimated the impact of isolated incidents of reshored production and misread or ignored the data.

If there were a true renaissance, we'd expect to see growth in inflation-adjusted manufacturing value added. But in fact 2013 manufacturing value added is 3.2 percent below 2007 levels, with non-durable goods value-added (which includes chemicals and oil and gas) down almost 12 percent. U.S. manufacturers employ over a million fewer workers and there are 15,000 fewer manufacturing establishments since the beginning of the Great Recession. Moreover, America ran a $458 billion trade deficit in manufacturing goods in 2013. Hardly evidence of a renaissance.

And most of the recovery that has occurred has been cyclical in nature. In fact, 122 percent of manufacturing output growth between 2010 and 2013 was in the auto sector, whose growth is due almost solely to a rebound in U.S. consumer demand, rather than reshoring of automobile production.

"Most of the claims for a structural rebirth of U.S. manufacturing are unfortunately based on myths and anecdotes," states Robert Atkinson, President of ITIF and co-author of the report. "Instead, any assessment of U.S. manufacturing should be based on rigorous analysis and review of the official data." Prevailing Wisdom The first article, released December 21, 2015 is far more damning than the second, released January 14. Check out the prevailing wisdom in January: " One thing is clear - optimism about the future of U.S. manufacturing is relatively buoyant, as 68% of the executives surveyed agreed that U.S. manufacturing will experience accelerated growth in the next five years." A manufacturing recession has been upon us for six months. Mike "Mish" Shedlock |

| Happy Winter Solstice! Posted: 21 Dec 2015 06:30 PM PST Reader Mark just pinged me with the message "Happy Winter Solstice! It only gets brighter from here."  I am passing that message on, along with an image of a garden bench, the setting sun and shadows I captured from my front yard (with apologies to readers from down under whose days are getting shorter). Mike "Mish" Shedlock |

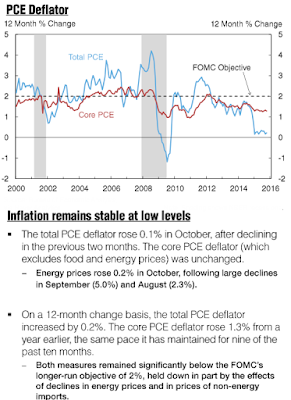

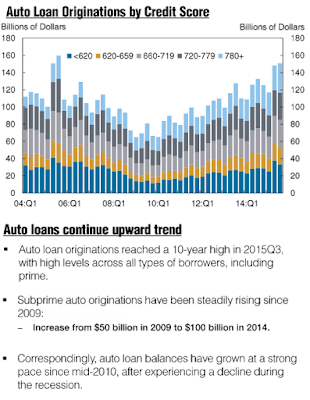

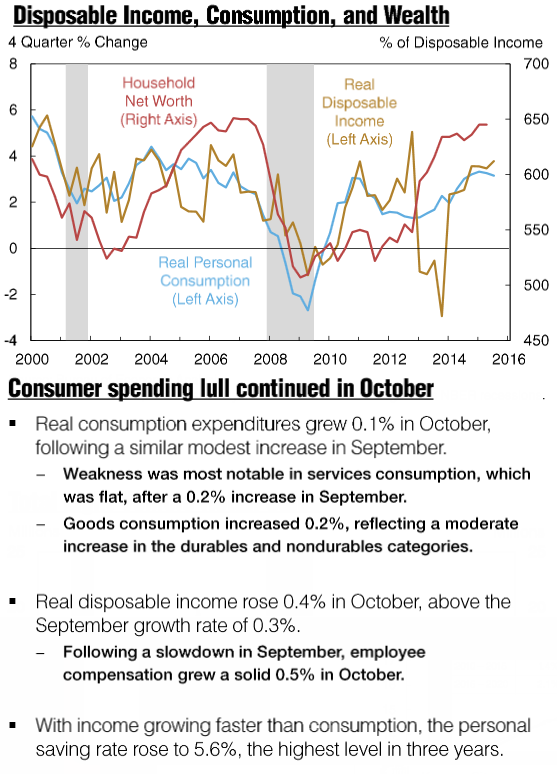

| US Economy Snapshot in Eyes of New York Fed vs. Eyes of Mish Posted: 21 Dec 2015 02:33 PM PST Inquiring minds are investigating a 17 page PDF of the U.S. Economy in a Snapshot by the New York Fed. The document is formatted poorly. Nearly every line is an image, requiring retyping or images snips of what appears to be (and should be) text. Here are some image snips along with my comments. Overview Mish Comment Mish Comment: Manufacturing is in a recession, inventories are too high, consumer spending is weak, autos are unsustainable and employment is a severely lagging indicator. The "fundamentals" are poor and sentiment is essentially useless.  Mish Comment Mish Comment: Inflation expectations are another totally useless idea, at least within normal bounds. At the point of hyperinflation, when people will buy anything to get rid of money, expectations have some meaning. There are signs of wage growth, but that will hurt profit margins and employment as spending stalls. Output, Natural Unemployment Rate Mish Comment: The natural rate of unemployment is that which would exist in a free market without interference from the Fed, from governments, from tariffs, etc. It's downright idiotic to pretend to know what the natural rate is, in any environment, let alone the highly manipulated state of affairs of today. Similarly, it is equally ridiculous to propose potential GDP levels. PCE Deflator Mish Comment Mish Comment: Price inflation (not monetary inflation) is subdued due to lack of demand, overcapacity, debt, beggar-thy-neighbor devaluation tactics, demographics, etc. Falling oil prices are a symptom, not a cause of price deflation. Manufacturing and ISM Mish Comment Mish Comment: The manufacturing recession is far more problematic than the Fed realizes. Disposable Income, Consumption Mish Comment Mish Comment: A rising savings rate is a healthy thing, but the Fed will not see it that way. Motor Vehicle Sales Mish Comment Mish Comment: The missing key words are in quotes at the end of this sentence: Motor vehicle sales are stable at high levels "for now". There is no pent up demand for autos, and autos were one of the few consistent bright spots during the recovery. But inventories are high and rising while sales are weakening. In reality, this spinning top is starting to look rather wobbly. Auto Loan Originations by Credit Score  Mish Comment Mish Comment: Sales are up in every loan category, but growth in subprime is problematic. Also problematic is the trend towards longer and longer auto loans, even on used cars. This sector has either peaked or soon will. Housing Mish Comment Mish Comment: The New York Fed blames " tight mortgage standards". That's a totally superficial analysis. Here are the real reasons. - Thanks to totally misguided Fed reflationary policies, home prices have recovered in most areas. In some areas prices are at new highs. For those most in need of new housing (the millennial generation), home prices are not affordable.

- Many empty-nester and aging boomers want to downsize. That leaves a big supply of upper-end homes for sale, at prices few can afford.

- Many millennials have moved back home to take care of their aging parents.

- Very high student debt levels have caused a delay in marriage and household formation.

- Attitudes have changed. Many kids have seen their parents or their friend's parents endure financial stress or even lose their marriage or homes in the great financial crisis. Millennials are understandably more cautious about taking on high levels of debt.

- Also in the attitudes category is the need to stay mobile. Holding down one or two jobs in the same area for 40 years until retirement is no longer the norm or even the expected. That desire to stay mobile also impedes new home ownership.

Mish Synopsis of New York Fed PresentationDespite weak manufacturing and little price inflation, the New York Fed sees solid fundamentals thanks to solid payroll and wage growth coupled with stable autos and improving housing. The New York Fed did not provide an overall synopsis so I formulated the above for them, from their overview and comments. This is their key sentence from their overview: " The general trend for consumer spending remains fairly solidly based on fundamentals such as healthy income growth, improving labor market conditions, and fairly upbeat sentiment." The New York Fed put emphasis on that statement in bold, I placed it in italics to set it apart from other bold titles. Mish 10-Point Synopsis- Jobs are a lagging indicator. I expect way larger than normal layoffs in January even if seasonal sales come in strong.

- Corporate profits are weakening while wages are ticking higher. That does not bode well for hiring plans.

- Many big box retailers are struggling. That too does not bode particularly well for hiring plans.

- Demographics are poor and outright deflationary.

- Single family housing is slow for the structural reasons outlined above, not cautious lending.

- Auto sales, one of the few economic bright spots in the recovery are as stable as a spinning top that's losing momentum.

- Manufacturing is in an outright recession.

- Inventory levels are high and rising despite weakening sales.

- Junk bonds are a huge warning sign.

- The flattening of the yield curve this early in a rate tightening cycle is a huge warning sign.

My prediction: A recession will arrive in 2016, assuming it has not already started. Mike "Mish" Shedlock |

| In the Wake of Podemos’ Unexpected "Victory"; Unsavory Demands; Expect New Elections Posted: 21 Dec 2015 11:47 AM PST Spanish mainstream political parties are reeling from the unexpected rise of Podemos. The radical left anti-austerity, eurosceptic party was sinking rapidly in the polls with a mere 16% of the projected vote a week ahead of the election. Instead, Podemos received 21% of the actual vote. That was enough for third place, and nearly second. The nationalistic party Ciudadanos fell to a distant fourth from a projected second-place finish. Unexpected "Victory" With that unprecedented final week swing Podemos Declares Victory and an end to Spain's two-party domination. Pablo Iglesias, leader of the anti-austerity Podemos party, emerged as the only true winner of Spain's general election and was quick to claim victory, albeit from third place.

"The era of two parties is done. It no longer exists," Mr Iglesias said on Monday.

Mr Iglesias, who launched the insurgent leftwing party two years ago, set out to break the dominance of the establishment centre-right Popular party and the centre-left Socialists. In the end, his party did better than even the most optimistic polls had predicted but the pony-tailed former politics lecturer will now have to prove himself, not just as a campaigner but as the leader of a large and potentially unruly bloc in parliament.

Podemos won 69 seats in the 350-seat parliament, behind prime minister Mariano Rajoy's Partido Popular (PP) on 123 and the Socialists (PSOE) on 90.

It came within a whisker of the Socialists in terms of share of the vote (21 per cent versus 22) and would have won even more seats were it not for an electoral system that favours parties with well-established operations in rural Spain. Splintered politics.The Podemos "victory" leaves politics in Spain splintered heavily, possibly beyond repair. To highlight the differences, simply take a look at five key Podemos demands that leader Pablo Iglesias laid out today. Five Primary Demands- More proportional electoral system

- Addition of housing, health and education as constitutional rights

- Recognition of the right of self-determination for regions such as Catalonia

- Depoliticised judiciary

- Rules against politicians serving on corporate boards

Points one and four seem reasonable enough. Point two on "constitutional rights" may not look scary at first glance, but details outlined in Incredible Populist Positions in Podemos' "Economic Manifesto"; Populism Explained) show many downright scary, radical socialistic ideas. Coalition ReviewPoint three is totally unacceptable to the other political parties. Ciudadanos seeks to return more power to the central government, not less. Thus, a three-way coalition with the socialist PSOE party, Podemos, and Ciudadanos simply cannot work even though Podemos' other four demand would likely be appeal to the group as a whole. PSOE and Rajoy's PP party not only have huge differences, they lack insufficient votes even if they would agree to work together. No coalition with enough votes to form a majority makes any sense given the huge differences between political goals. Prime minister Rajoy may not even try to form a minority government. That possibility would immediately lead to new elections. But leaders seldom step aside voluntarily, so the most likely outcome appears to be formation of a very unstable minority government that will fail soon enough. Either way, new Spanish elections are on the event horizon. Mike "Mish" Shedlock |

| Record Oil Output From Russia Despite Low Prices Posted: 21 Dec 2015 01:05 AM PST Here's one for the "this was not supposed to happen, and nobody saw it coming" book. Bloomberg reports on the Siberian Surprise: Russian Oil Patch Just Keeps Pumping. In the fight for market share among the world's oil producers this year, Russia wasn't supposed to be a contender.

But the world's No. 3 producer has been pumping at the fastest pace since the collapse of the Soviet Union, adding to the flood on an already-swamped market and helping push prices to the lowest levels since 2009.

Russia's unexpected oil bounty this year is the result not of a new Kremlin campaign but of dozens of modest productivity improvements across the sprawling sector.

With a rise of 0.5 percent in the first nine months of 2015, Russia hasn't boosted production as much as its larger rivals, the U.S. (up 1.3 percent) and Saudi Arabia (up 5.8 percent), according to Citigroup Inc. But having ignored OPEC's calls earlier this year to join efforts to support prices by pumping less, Russia is keeping up with the cartel.

"I know of no one who had predicted that Russian production would rise in 2015, let alone to new record levels," said Edward Morse, Citigroup's global head of commodities research. As recently as April, not even the Russian government thought 2015 would break the record.

One side effect of falling oil prices -- the 52 percent plunge in the ruble over the last two years -- has helped Russian oil producers, chopping their costs in dollar terms since between 80 and 90 percent of their spending comes in rubles.

"I don't know what the oil price would have to fall to for things to change dramatically," Stavskiy said. "We've been through $9 a barrel and production continued, so if something like that happens, we know what to do."

Relatively high taxes on oil have actually sheltered the industry from much of the impact of the drop in prices. The government takes nearly on crude exports everything above $30-$40 a barrel, so companies don't feel much impact until prices fall below that. For the conspiracy-minded, if it takes $30 for Russia to feel pain over oil, we will soon see it. Meanwhile, back in the US, oil production is strong despite total rig counts dropping from 1875 to 709 in the last year. That's a decline of 1166 rigs. In percentage terms it's a 62% drop. Of the 709 total rigs, 541 are oil rigs. Gas rigs count 168. For the week, oil rigs rose by 17 while gas rigs fell by 7. A year ago there were 1536 oil rigs. Thus, oil rig count is down by 995 rigs, a decline of 65%. US rig count numbers compare December 18, 2015 to December 19, 2014 (the last day of the work week). Mike "Mish" Shedlock |

No comments:

Post a Comment