| Fed Openly Discusses "Permanently High Balance Sheet"; Lie Finally Admitted Posted: 14 Dec 2015 07:05 PM PST Merits of Not Shrinking the BalloonWhen the Fed first launched QE, they stated they had the "tools" necessary to shrink their ballooning balance sheet. I quickly made the claim, no thinking person on the planet believed that lie. ZeroHedge made similar comments, as did others. So no one is a genius for predicting today's non-news headline Fed Weighs Merits of Jumbo Portfolio in Post-Crisis Era. Once the Federal Reserve lifts interest rates from near zero, likely this week, the focus will turn to the other legacy of the crisis-era policies: the Fed's swollen balance sheet.

The prevailing view is that the U.S. central bank's $4.5 trillion portfolio, vastly expanded by bond purchases aimed at stimulating the economy, will have to shrink once rates are on their way up, and the Fed will just need to decide how quickly.

Now, however, there is a new twist to the debate, with some policymakers and outside experts saying that there are reasons to keep the balance sheet big.

As recently as September 2014, the Fed pledged to eventually "hold no more securities than necessary," in its "normalization" plan, a level widely interpreted as close to its pre-crisis $900 billion size.

A "permanently higher balance sheet ... is something that we haven't studied that much but I think needs a lot more thought," John Williams, president of the San Francisco Fed, said last month.

It could also give the Fed a permanent policy tool with which to target sectors of the economy and certain parts of the bond market.

For example, the Fed could buy and sell certain assets to stimulate or cool the mortgage market or to affect longer-term borrowing costs, says Benjamin Friedman, former chairman of Harvard University's economics department.

Fed researchers have been studying how many and what type of bonds should be stay on the Fed's books in a "post-normalization world" - an effort one source familiar with the work called a "once in a decade" research opportunity.

Ben Bernanke, who as Fed Chairman unleashed the bond-buying that pushed the balance sheet to its current size, also weighed into the debate downplaying any concerns about the Fed's outsized portfolio.

"The Fed could leave the balance sheet where it is and that wouldn't be a problem," he told New York Economics Club last month, noting its size is "internationally normal" in relation to the economy's output.

One result of the swollen portfolio is the $2.6 trillion in excess reserves that banks now park at the Fed, earning interest that will only rise as rates tick higher.

The idea that the Fed is paying extra billions to the very banks blamed for the crisis could re-ignite criticism from lawmakers already sour on the Fed's aggressive stimulus.

A big balance sheet poses "huge optics problems," says John Cochrane, a senior fellow at the Hoover Institution.

Still, there are obvious financial stability benefits to keeping the balance sheet large, he says.

One thing is clear: the Fed has not shut the door on keeping a bigger balance sheet for longer, or using it as a policy tool on top of its usual lever of setting short-term borrowing costs. Lie Finally AdmittedThe Fed never had any intention of shrinking its balance sheet by any other method than holding bonds to termination over time, if that. Supposedly a "debate" is now on. There is no debate. The Fed will do whatever the hell it wants while labeling the result a new "tool". Anyone who genuinely believes this is some sort of "new twist" should wear a scarlet sweater with the tag "gullible fool" Mike "Mish" Shedlock |

| Trump Warns "Dopey" Saudi Prince "Can’t Buy US Politicians When I Get Elected"; Religious Discrimination of Saudi Prince vs. Trump Posted: 14 Dec 2015 01:06 PM PST Entertainment ValueRegardless of your other opinions on Donald Trump, he is good for at least one thing in what would otherwise be a rather boring election campaign: entertainment. And so it was over the weekend after Saudi prince Bin Talal tweeted to Donald Trump "You are a disgrace not only to the GOP but to all America. Withdraw from the U.S. presidential race as you will never win." Trump, Saudi Prince Exchange Hostile Tweets Trump smacked back Your Days Of Buying Off American Politicians Will Be Over If I Am Elected President. Republican presidential front-runner Donald Trump is returning fire against the Saudi prince who told him to drop out of the White House race.

Trump called billionaire Prince Alwaleed Bin Talal "dopey" and accused him of trying to buy U.S. politicians with "daddy's money" in a tweet late Friday.

"Dopey Prince @Alwaleed_Talal wants to control our U.S. politicians with daddy's money. Can't do it when I get elected," Republican presidential front-runner Donald J. Trump tweeted after the prince told him to end his White House bid. Has Saudi Arabia Taken Any Syrian Refugees?The Independent reports Donald Trump calls on Saudi Arabia to take in refugees after spat with Saudi Prince. Hot on the heels of demanding all Muslims be banned from the US, Donald Trump has called on Saudi Arabia to take in Syrian refugees.

Mr Trump made the demand on Twitter writing: "Has [...] Saudi Arabia, taken any of the Syrian refugees? If not, why not?"

The comment comes after Mr Trump became embroiled in a row with Saudi Prince Alwaleed, the chairman of Kingdom Holding, who branded the businessman was "a disgrace" and should withdraw from the presidential race following his controversial remarks about the apparent threat posed by Muslims. Religious Immigration Bans OK Unless It's Against Your ReligionThe Daily Caller notes the hypocrisy of Saudi Arabia in its post Why Won't The Saudis Who Resent Trump Drop Their Ban On Jews?The online bickering between Republican presidential candidate Donald Trump and his fellow billionaire Saudi Prince Alwaleed bin Talal over Trump's proposal to ban Muslim immigration is seeped with irony: For decades, Saudi Arabia has had a near-total ban on granting visas to Jews.

America's protestations of this blatant bigotry have been largely muted, apparently in deference to the sensibilities our oil-rich ally.

Clearly, the Saudis are not taking a principled stand against religion-based visa discrimination. They think discriminating against a religion is perfectly fine – as long as it's not their religion.

(To be clear, I abhor Trump's proposed policy. That does not detract from the outrageous Saudi inconsistency on the matter.)

The Saudi approach is consistent with Muslim attitudes toward "blaspheming" their prophet. During the 2005 controversy over cartoons depicting Mohammad, Muslims around the world claimed it was wrong to criticize people's religions – but they never objected to images and artwork criticizing Christianity and other non-Muslim religions.

And that's the point. Most Muslim countries and many of their citizens do not share Western-style values of tolerance and respect. They do not tolerate and respect other religions; they just want special treatment for Islam.

The Democrats and Republicans who have been rushing to attack Trump's comments about Muslims who visit America would be wise to condemn religion-based discrimination in all parts of the world. And the Saudis could demonstrate that their protests are based on principle rather than self-interest by changing their visa policies and finally welcoming Israelis and other Jews who wish to visit.

I'm not holding my breath. How this plays out to US voters remains to be seen. Mike "Mish" Shedlock |

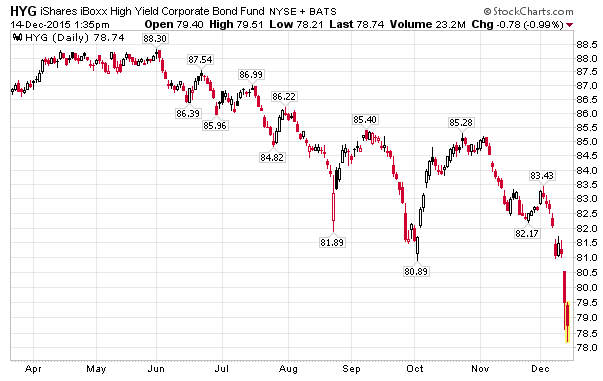

| High Anxiety Liquidity Trap: Selloff in Junk Continues, Follows Largest Drop Since 2011 on Friday Posted: 14 Dec 2015 10:59 AM PST In financial markets rot starts at the periphery and spreads to the core. For weeks, rot has been visible in the junk bond market and that rot has deepened sharply recently. JNK - Barclays High Yield ETF HYG - iShares iBOXX High Yield Corporate Bond Fund HYG - iShares iBOXX High Yield Corporate Bond Fund Liquidity Trap Liquidity TrapA potentially destabilizing run on junk debt has weighed on the bond markets. Investors in one fund are totally locked out of redemptions. Effective yields have soared. Please consider The Liquidity Trap That's Spooking Bond Funds. The debt world is haunted by a specter—of a destabilizing run on markets.

Last week, this took on more form even if there weren't concrete signs of panic. Only one mutual fund manager, Third Avenue Management, has said it would halt redemptions to forestall having to dispose of assets in a fire sale. The rest of the industry has been quick to say that while redemptions are elevated, particularly in high-yield bond funds, there doesn't seem to be a rush to for the exits.

Goldman Sachs, for one, put out a note Friday warning Franklin Resources "is most at risk" given the large high-yield holdings of its funds, poor performance and large outflows. On Friday, its shares fell sharply. Meanwhile, there were unusually large declines Friday in the value of exchange-traded funds that track high-yield debt.

The idea of a "run" on mutual funds might sound strange. Typically, runs are associated with highly leveraged banks engaged in maturity transformation, funding long-term loans with short-term debt. Nearly all the programs designed to avoid destabilizing runs—from deposit insurance to the Fed's discount window to liquidity requirements—are built for banks.

But unleveraged investors, including mutual funds, can also give rise to runs. That is because there is a liquidity mismatch in mutual funds that hold relatively illiquid assets funded by investors entitled to daily redemptions.

Similar to what can happen in a bank run, investors in open-end funds holding relatively illiquid assets have an incentive to withdraw early to avoid being last out the door.

The problem is potentially more acute when it comes to funds that invest in corporate bonds, which don't trade frequently, as opposed to stocks. That is an even greater concern today given questions about bond-market liquidity.

Mutual-fund fragility was highlighted in a speech last year by then-Fed Governor Jeremy Stein and a related paper prepared for a Fed policy forum. Mr. Stein noted fund managers were likely to sell more-liquid holdings to meet the earliest redemptions. This leaves remaining investors even more exposed to illiquid bonds. Panic EarlyThe message here is clear. If you are going to sell be the first. In short, panic before anyone else does. That advice is especially important for junk bond ETF holders as managers tend to sell liquid issues first, presumably holding the most illiquid and likely junkiest of junk on the books. High Anxiety Why Now? Why Now?It is absurd that CCC-rated debt, right on the verge of default would ever yield as little as it did. In regards to that point, I have noted the bubble in junk bonds numerous times over the past couple years. Why this took so long to sink is anyone's guess, but undoubtedly the FED's QE played a part. Bubbles nearly always go on longer than one might think. But here we are. And here's another important point, equity selloffs frequently begin with bond market dislocations or deteriorating equity-market breadth. Be forewarned. Today we see both, at a time the stock market is more overvalued than ever. Further Reading- "War Games" Show Fed Worried About Commercial Real Estate, Interest Rates; Fed Weighs Consequences of "Macroprudential Tools"

- Stocks More Overvalued Now Than 2000 and 2007 No Matter How You Look at Things

In regards to point one, the Fed after warning about "Macroprudential Tools", does not even realize QE and interest rate policy are the bluntest of blunt instruments, both prone to bubble-blowing episodes. Once bubbles get big enough or attitudes change enough, tools no longer work. And the opposite tool (in this case ending QE and hiking rates) might have an oversized effect. In regards to point two, Fed timing could hardly be worse, but the only alternative is even bigger bubbles that would pop on their own accord anyway. Mike "Mish" Shedlock |

No comments:

Post a Comment