Mish's Global Economic Trend Analysis |

- Retaliation and Claims 101: Beneficiaries and the Failure to Think Ahead

- GDPNow Forecast for 4th Quarter Dips to 1.4% Following Weak ISM and Strong Construction Reports

- Manufacturing ISM Contracts; Lowest Reading Since June 2009; Glimmers of Hope Extinguished

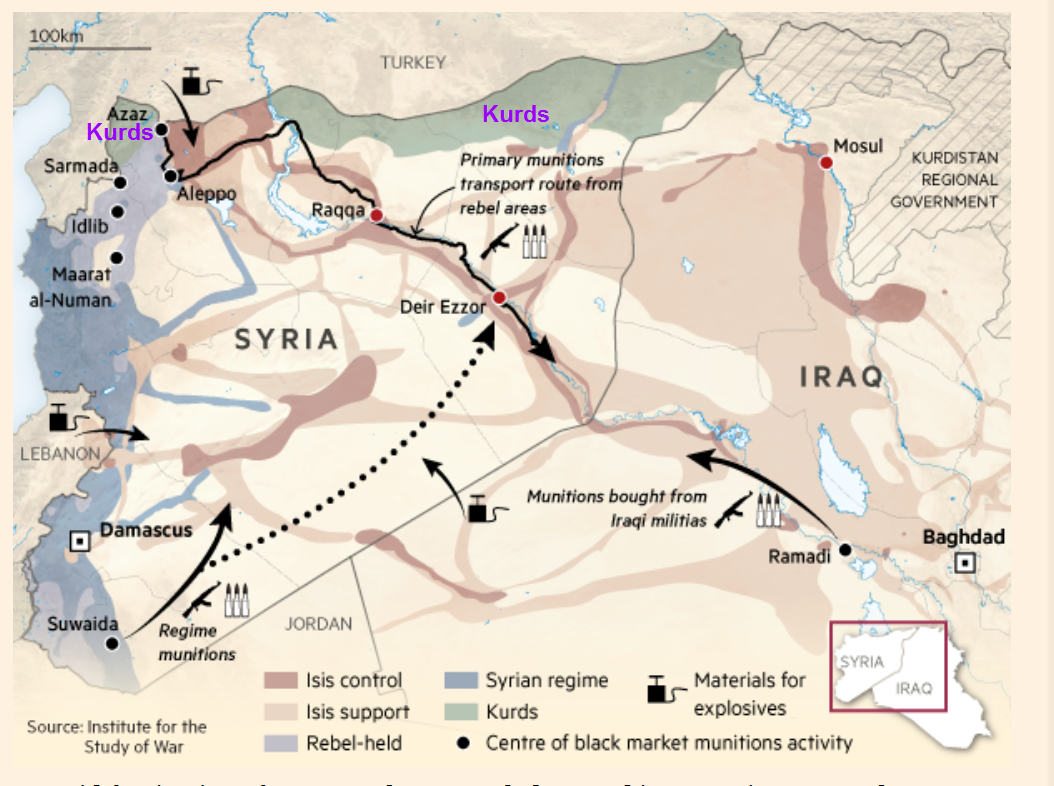

| Retaliation and Claims 101: Beneficiaries and the Failure to Think Ahead Posted: 01 Dec 2015 07:09 PM PST Claims and counterclaims are the order of the day between Turkey and Russia. The US and Syria stand not side-by-side, but rather on each side, most of the time, but not all of the time. Background for this post is the deliberate shooting down by Turkey, a Russian aircraft attacking ISIS and alleged moderate rebels in Syria. At most, Russian aircraft were over Turkey for a matter of seconds. But Russia claims its aircraft were not over Turkey at all. Then came the unbelievable lie Turkey Says It Had Not Recognized the Aircraft as Russian When it Shot it Down. Putin angrily dismissed Turkey's claim as "impossible" and said Russia had provided the US with information on the time and location of its sorties. The Claim Russia claims Turkey shot down plane to protect oil trade with ISIS. The Response Turkish president Recep Tayyip Erdogan responded He Will Resign if Putin Can Prove the Claim. The Counter-Challenge Next, Erdogan Challenged Putin to Resign if he Can't Prove Turkey Buys Oil from ISIS. Alleged Proof Meanwhile, RT claims Russia has 'More Proof' ISIS Oil Routed Through Turkey. The article did not adequately detail the alleged proof. Question of Semantics Without a doubt, ISIS oil is flowing through Turkey. But there's a huge semantics question in play. Does proof require the Turkish administration bought ISIS oil? Or is it sufficient that some smugglers in Turkey do just that? The Need to Think Ahead Who is the winner here? In Turkey was protecting ISIL oil Smuggling; Russia urges Assad-Kurdish Alliance, Yuan Cole at Informed Comment offers an option that I largely agree with, but he did miss one significant aspect. Putin has a much more effective way of bringing the pain to Erdogan.The Beneficiaries The primary beneficiary of this mess is neither the US nor Turkey. Here they are.

The biggest loser is Turkey, arguably followed by the US for its inane backing of alleged moderate Al Qaeda rebels. Of course, the US goal of overthrowing Al-Asad without having any reasonable replacement is so ridiculous, the US is in reality an inadvertent winner. Who Controls What?  The above map ties everything together nicely. It's from the Financial Times article US Urges Turkey to Seal Border with Syria Sealing the border between Turkey and Syria and also between Turkey and Greece is exactly what I have been calling for. Turkey may be unlikely to cooperate because it would rather deal with ISIS than the despised Kurds who may seek their own territory in Turkey. Warmongers Win There is one more winner that needs to be addressed: US warmongers. In response to the shootdown of the Russian aircraft by Turkey, Russia Arms Fighter-Bombers in Syria with Air-to-Air Missiles. Russia announced Monday that a class of its fighter-bombers in Syria has been armed for the first time with air-to-air missiles for "defensive purposes" in a move that posed a potential risk to U.S. and coalition warplanes flying missions against the Islamic State.Tension The Mideast tension between a multitude of players increases the likelihood of an "accident" or an "accidentally on purpose" type of incident between Russian and Turkey or Russia and the US. Warmongers would cheer such events. Finally, I offer an opinion that Turkey did not shoot down the Russian jet over oil per se, but rather because Turkey would rather deal with ISIS than the Kurds. Chancellor Merkel is downright idiotic to be supporting Turkey in this set of circumstances, but here we are. In this aspect, Turkey is a big winner and the EU a big loser if Turkey gets the German/EU concessions it seeks. Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

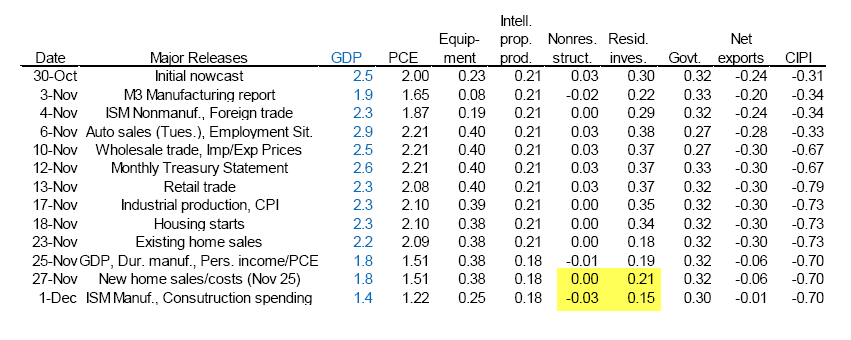

| GDPNow Forecast for 4th Quarter Dips to 1.4% Following Weak ISM and Strong Construction Reports Posted: 01 Dec 2015 11:27 AM PST Construction Spending Hits 8-Year High US News reports US Construction Spending Jumps to 8-Year High, Lifted by Home Building, Federal Government. The construction of single-family homes and apartments climbed 1 percent in October, also reaching their highest level since December 2007. Manufacturers boosted their construction spending by 3 percent. And federal government building soared 19.2 percent, the biggest increase since October 2006.Construction Spending Beats Estimates The consensus estimate for construction spending was +0.6% but the actual month-over-month reading was +1.0%. Construction is one of the highlights of the 2015 economy with spending up a solid 1.0 percent in October for the best rate since May. Despite mixed signals from the housing sector, spending on residential construction is very solid, up 1.0 percent in October for a seventh straight gain and all of them convincing. Year-on-year, residential construction is up 16.6 percent vs 13.0 percent for total spending.Construction Contribution to GDP As noted earlier today, this morning's ISM report was a disaster. (See Manufacturing ISM Contracts; Lowest Reading Since June 2009; Glimmers of Hope Extinguished). But the construction report looked good. Like Bloomberg, I would have expected construction to add to GDP, in isolation. Combined with ISM spending, I would have expected the net result of today's reports to be an overall small minus. Actual GDPNow Forecast Results were dramatically different. GDPNow Forecast Sinks 0.4 Percentage Points to 1.4 Percent  Construction Subtracts From GDP vs. Prior Estimate  Compared to the November 27 report that included new home sales, construction appears to have subtracted approximately 0.09 percentage points and ISM roughly another 0.31 percentage points. Other reports in between may have contributed but those should be the main factors. I have a question into the Atlanta Fed regarding construction contribution to GDP. Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Manufacturing ISM Contracts; Lowest Reading Since June 2009; Glimmers of Hope Extinguished Posted: 01 Dec 2015 09:24 AM PST After flirting with contraction for three months, the Manufacturing ISM fell into negative territory with a 48.6 reading, below the lowest Econoday estimate of 49.7. The Econoday Consensus guess was 50.5, an improvement over the October reading of 50.1 After skirting right at the breakeven 50 line since September, ISM's manufacturing index broke below in November to 48.6 which is more than 1 point below Econoday's low-end estimate for the lowest reading since June 2009. The decline includes a significant dip for new orders which are down 4.0 points to 48.9 and the lowest reading since August 2012. At 43.0, backlog orders are in a six-month streak of contraction. With orders down, ISM's sample cut back on production, down nearly 4 points to 49.2, and cut back on inventories, down 3.5 points to 43.0. Employment firmed but remains soft at 51.3.Glimmers of Hope Extinguished The ISM index came in at 50.2 last month, vs. a consensus estimate of 50.0, providing economists with glimmers of hope. Economists then did what they normally do, which is take the prior reading and expect the next month to be better, explaining this month's consensus guess of 50.5. ISM 2007-2015  That was the lowest reading since June 2009. But don't worry, there's no recession warning here, just glimmers of hope. And with that hope, let's further dive into the numbers straight from the ISM Report.

Key Points

There's nothing in the ISM report to make the Fed want to hike, but the Fed will do what they want. Mike "Mish" Shedlock |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment