Mish's Global Economic Trend Analysis |

- In Rare Agreement with Krugman; Onerous "Bailout" Rates of 6.7% Denied; Don't do Stupid Things; "Tell the EU and IMF to Shove It!"

- Spain, Portugal Deny Need for Bailouts; Swaps Soar on ‘Sacrosanct’ Senior Europe Debt; Bank of China Adviser Tell US to Sell Gold

- Merkel's Dilemma; Eurozone Borrowing Costs Hit Record; Expect Sovereign Defaults

- China's Economic Treadmill to Hell; Shadow Over Asia; What happen WHEN China Slows?

| Posted: 26 Nov 2010 06:52 PM PST News on Ireland is pouring in so fast from all corners it is a struggle keeping up with it. In a Memo to Ireland, Mike Whitney says, "Tell the EU and IMF to Shove It!" and on that score I agree 100% having said the same thing quite some time ago. Some articles suggest the bailout rate will be 6.7%, other stories deny that. Finally, I find myself in rare agreement with Paul Krugman. Let's start there. Agreement With Krugman In one of his longest pieces that I remember, Paul Krugman makes the case Ireland is getting screwed. Please consider Eating the Irish Before the bank bust, Ireland had little public debt. But with taxpayers suddenly on the hook for gigantic bank losses, even as revenues plunged, the nation's creditworthiness was put in doubt. So Ireland tried to reassure the markets with a harsh program of spending cuts."Tell the EU and IMF to Shove It!" Krugman asks "Does it really have to be this way?" Of course it doesn't. In a Memo to Ireland, Mike Whitney says, "Tell the EU and IMF to Shove It!" Irish Prime Minister Brian Cowen is Mahmoud Abbas. He's caved in to the demands of foreign capital and transferred control over the nation's budget to the EU and the IMF.Irish Citizens Sold Down the River in "Firepower of Stupidity" On November 21, in Irish Citizens Sold Down the River in "Firepower of Stupidity" I wrote... Today the Irish Government sold its citizens into debt slavery by agreeing to guarantee stupid loans made by German, British, and US banks. Those loans fueled one of the biggest property bubbles in the world. Ireland has since crashed.6.7% Rate? RTE News reports EU/IMF interest rate likely to be 6.7% The interest rate to be charged on the European Unions/International Monetary Fund package is likely to be 6.7% for nine year money.6.7% rate rejected The Irish Times reports 6.7% rate rejected The interest rate for a nine-year EU/IMF loan would be lower than the 6.7 per cent being quoted in some reports today, a source involved in the talks has indicated.Debt Slaves Forever Fintan O'Toole writing for the Irish Times says The people must act or we will remain irrelevant HAVING AN election after agreeing a four-year deal that will shape all key decisions is like debating which brand of condom to buy after you've become pregnant. It is a parody of democratic choice. Popular sovereignty has almost no meaning in Ireland right now. Its restoration is the precondition for a meaningful election.Don't Do Stupid Things I will tell Ireland the same thing I told Iceland on March 6, 2010: Iceland Rejects IceSave; Does No Mean No? Icelanders overwhelmingly rejected a bill that would saddle each citizen with $16,400 of debt in protest at U.K. and Dutch demands that they cover losses triggered by the failure of a private bank, first results show.In response to the above post I even received a nice Email From Birgitta Jonsdottir, Member of Iceland's Parliament thanking me for my help. ANY Rate is Onerous All these questions "Is the rate 4.7%, 5.2%, or 6.7% and if so for who long and on what portion?" are complete silliness. ANY Rate is Onerous. Except for those who participated in the property bubble (and they will be adequately punished), the people of Ireland are not at fault, at least in general. Should Irish Prime Minister Brian Cowen manage to hang on long enough to get the votes for an onerous bailout, I would encourage Irish voter to elect someone who campaigns on a promise to renege on the deal and default. Irish citizens cannot afford to rescue German, UK, and French banks stupid enough to bet on bubbles in Ireland. It should be the creditors' problem not the problem of Irish citizens. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 26 Nov 2010 09:55 AM PST Not that anyone can possibly believe these stories, but Spain's Prime minister says "says no chance Spain will need bailout". In other humorous news on this Black Friday, Portugal denies the need for a bailout, and the always late S&P drops Anglo Irish Bank six notches to a junk-bond B grade. Topping off the humorous news stories of the day, an adviser for the PBOC tells the US to sell gold to balance its budget. Spain "Absolutely" Rules Out Bailout Spain's Prime Minister says says no chance Spain will need bailout Prime Minister Jose Luis Rodriguez Zapatero said Friday there was no chance Spain would seek a bailout. Asked in an interview on Spain's RAC 1 radio if he ruled out financial help from the European Union, Zapatero said "absolutely."Portugal Denies Bailout Talk The odds Portugal is not in some kind of discussion with the EU regarding bailouts seems rather slim, yet Portugal Denies Bailout Talk The epicenter of Europe's sovereign-debt crisis shifted from Ireland to the Iberian peninsula on Friday, with European Union, Portuguese and Spanish officials scrambling to head off speculation that Lisbon or Madrid could soon be forced to seek help to meet their borrowing needs.My strong conviction is that the more money the EU puts on the table to rescue the PIGS, the more money will ultimately go up in smoke. Anglo Irish Bank Drops Six Notches to Junk-Bond B Grade The never on-time and totally useless rating agency S&P cuts ratings on Irish banks; Anglo deemed junk New York-based S&P said in a statement Friday it was lowering Anglo Irish Bank six notches to a junk-bond B grade. It also cut the ratings on Bank of Ireland and Allied Irish Banks one notch each to BBB+ and BBB, respectively.Swaps Soar on 'Sacrosanct' Senior Europe Debt Bloomberg reports Swaps Soar on 'Sacrosanct' Senior Europe Debt The cost of protecting against defaults on senior notes of European banks is soaring on speculation bondholders will be forced to take losses as governments try to share the burden of taxpayer-funded bailouts.Bank of China Adviser Tell US to Sell Gold Please consider PBOC Researcher Calls on U.S. to Sell Gold, People's Daily Says The U.S. should cut its government spending and sell some gold reserves to balance its budget and fund its recovery, the People's Daily overseas edition reported, citing Xia Bin, an adviser to the People's Bank of China.Here's the punch line, "the PBOC researcher didn't mention whether China would be willing to purchase any gold from the U.S." Ya think not? Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

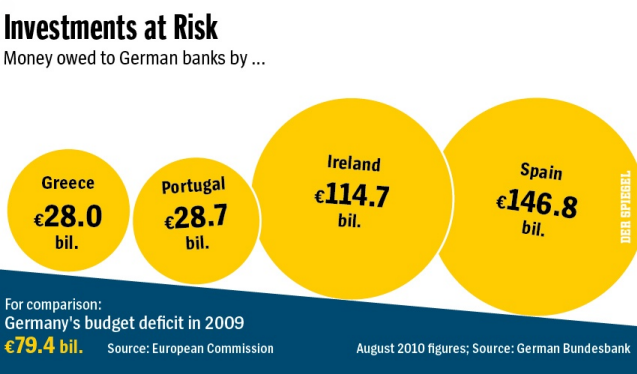

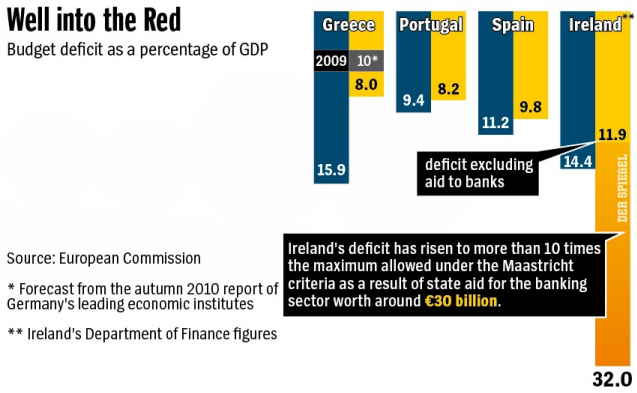

| Merkel's Dilemma; Eurozone Borrowing Costs Hit Record; Expect Sovereign Defaults Posted: 26 Nov 2010 07:58 AM PST The Spiegel Online shows the severe problem facing facing Germany in terms of investments at risk, the enormous amount of money owed German banks by the PIGS (Portugal, Ireland, Greece, and Spain). Please consider Merkel's Dilemma, Chancellor Faces Tough Sell on Irish Bailout For the second time in just a few months, Angela Merkel will have to explain to voters why Germany must bail out a fellow euro-zone member state. Skepticism is growing -- amongst voters, in the media and within her party. Many want to see Dublin raise its low corporate tax.Misplaced Blame on Ireland's Corporate Tax Structure Note the repeated blame placed on Ireland's corporate tax structure. The blame really should be placed on German banks stupid enough to fund Ireland's property bubble. Investments at Risk  Ireland's Budget Deficit 10 Times Maximum Allowed Under Maastricht Treaty  There is much more in that Spiegel Online column, please give it a look. In what way is Ireland responsible for that debt structure? Did Ireland put a bazooka to Germany's head demanding those loans? If not, and the answer is "not", then why should either German citizens or Ireland's citizens have to pay for a bailout of Ireland? German, UK, and US holders of Irish debt (banks) should have to (and will have to) take a big haircut on that debt. It's as simple as that. Eurozone Borrowing Costs Hit Record One look at the above is all you need to understand to figure out this would happen: Eurozone borrowing costs hit record Irish, Portuguese and Spanish bond yields surged to their highest points since the launch of the euro, as traders said even some of the bigger eurozone countries could soon be affected. Matt King, global head of credit strategy at Citi, said the danger was the selling could develop a momentum of its own.Destabilizing Rescue It's clear that Ireland needs many reforms, but raising its corporate tax rate now sure does not appear to be one of them. That low tax rate is the only possible way Ireland can maintain any growth edge that would allow it to dig out of its hole. Moreover, it's important to understand that the alleged "bailout" is nothing more than a moderately-high-interest loan with unsound-strings attached. Those strings are more like anchors. They put added stress on the system. Even if, the ECB comes to yet another rescue for Portugal and Spain (and some complete fools are calling for preemptive ECB action to do just that), the whole structure of these bailouts is destabilizing. What cannot be paid back, will not be paid back. Thus, lending Ireland, Greece, Spain, and Portugal more money under onerous terms is the height of extend-and-pretend stupidity. Expect sovereign defaults. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| China's Economic Treadmill to Hell; Shadow Over Asia; What happen WHEN China Slows? Posted: 26 Nov 2010 12:51 AM PST Last week in his China Financial Markets blog, Michael Pettis raised the interesting question What happens IF Chinese growth slows?. His answer may surprise you, and mine is quite different, even though I agree with most of his discussion. How can that be? Let's take a look at his post. Pettis writes ... Last week I suggested that slowly the consensus is shifting towards a recognition that Chinese growth may slow sharply in the next few years. When I discuss this prospect with analysts and investors, however, they almost always worry about two things. First, since China represents the largest component of global growth, it seems reasonable to expect that a sharp slowdown in China will also mean a sharp slowdown in global growth. Slowing Chinese growth, in other words, should be terrible for the world. Secondly, if growth does slow sharply, this should cause an equally sharp rise in social instability and, with it, rising political instability.Pettis goes on to explain how Japan in 1990 was 17% of the global economy, and every one figured Japan would soon take over the world. Yet in spite of the fact that Japan's growth rate collapsed to 1%, the rest of the world expanded rapidly and there certainly was little social instability in Japan. What Pettis failed to mention is 1990's global economy received a tremendous productivity boost from the interment boom, more than making up for any slowdown because of Japan. Moreover, that internet boom was quickly followed by global housing and credit bubbles, the likes of which the world has never seen. Now we have global headwinds of extremely slow global growth outside of China, with credit contracting in the US for 10 straight quarters, and an increasingly hostile to further deficit spending in the UK and in US Congress. I believe it is very safe to assume we are not going to have another internet revolution or another massive housing boom. History shows, the last bubble is never re-blown. Could there be another boom-causing bubble? Of course, but I sure would not bet on it, or even think it is highly likely. Nonetheless, Pettis cleverly left himself an "out", and it's one I agree with: "...not that they are necessarily wrong but rather that they are not obviously true" Pettis continues .... I think the Japanese story has important implications for our analysis of China. If China indeed experiences a rapid slowdown in GDP growth, the impact on the rest of the world may be far less than we expect. The real key is the evolution of the Chinese trade surplus. If it contracts, it will provide an expansionary boost to the rest of the world, not a contractionary one.Three Key Points From Pettis

Uneven Consequences Point number one is a given. I agree with point number two and three although I can see how many would disagree. The devil of course is in the details, and that's where I possibly differ from Pettis. It's hard to say for sure because he did not expound on country-to-country differences. This is how I see it. China is clearly overheating. When (not if) China slows, that will halt pressure on rising commodity prices. Falling oil prices would help reduce the US trade deficit, especially if grain prices remain firm. Falling energy, copper, and metal prices would help US homebuilders and small businesses hurt in a price squeeze of rising input prices and falling prices of goods and services. The net effect of this would be to strengthen the US dollar, yet help the US economy. Ironically, Bernanke might not see it that way because short-term it might cause the CPI to go negative. Moreover, it might not be good for multinational corporations or the US stock market in general which generally benefits from a falling US dollar. However, long-term it would help rebalance the global economy, and hopefully shut off protectionist trade measures in Congress. That last point is crucial. Everything depends on how fast China slows, and how rambunctious the next Congress is, and whether or not President Obama would veto currency manipulation legislation from Congress. Assuming that Congress does not act to kill global trade (admittedly that's a big assumption), net-net the overall global effect of China slowing would not be a disaster for the world "in general", and in fact, the world would likely benefit. The key words in the last sentence however, are "in general". An additional caveat is: if Congress manages to kill global trade with ill-advised protectionist legislation, the whole world loses. Australia and Canada Will Suffer As noted above, the US would likely benefit from a normal slowdown in China (or a crash not caused by collapsing global trade). However, Australia and Canada with their housing bubbles already poised to implode would suffer mightily if commodity prices tumble. Given that the US and Europe are far more important globally, A slowdown in China might be a net benefit for the world "in general", yet a total disaster for countries overly dependent on continuous strong growth in China. Australia and Canada would be especially hard hit, right at the worst possible time. Why China Will Implode Now that we have addressed what happens WHEN China slows. Let's discuss WHY China will do so. China's Economic Treadmill to Hell Please consider Fortune Magazine's Chanos vs. China The influential short-seller is betting that China's economy is about to implode in a spectacular real estate bust. A lot of people are hoping that Chanos - who called Enron right - is wrong this time.Chanos: China's Treadmill to Hell Video Shadow Over Asia Inquiring minds are reading The Only Question About The China Crash Is When by David Galland, Managing Editor, The Casey ReportHyperinflation in Japan The interview is quite lengthy and extremely good. It covers both Japan and China. It is hard to excerpt because I agree with nearly everything Vitaliy Katsenelson says. I find it interesting that Vitaliy makes a case that Hyperinflation will occur in Japan before the United states. That is something I proposed 5 years ago and have stated a few times since. Vitaliy makes a solid case ... VK: Japan's story is very simple. The economy slowed down in the 1990s. To keep the economy growing, the government lowered taxes and increased government spending, sending budget deficits up. In order to finance those deficits, the amount of government debt has tripled.The interview is well worth a read in entirety with lots of charts and ideas. The one thing Vitaliy doesn't know is the same thing I don't know: When. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment