Mish's Global Economic Trend Analysis |

- US Foreclosure Inventories 7.4 Times Normal and Rising; In OZ 'Low-Doc' Home Owners Hit by Rising Rates; US vs. Australia Progression of Rot

- Buyers' Strike in Low-Yield Corporate Debt; Goldman's Bond Forecast

- Ireland's "String and Sealing-Wax Fix"; Irish PM Loses Confidence of Own Party; European Sovereign Default Risk Hits All Time High

- Failure to Consider Constraints - My Response to "Has Mish Deflated the Inflationistas?"

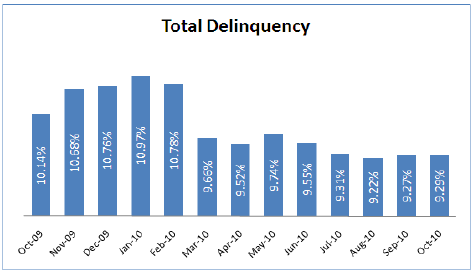

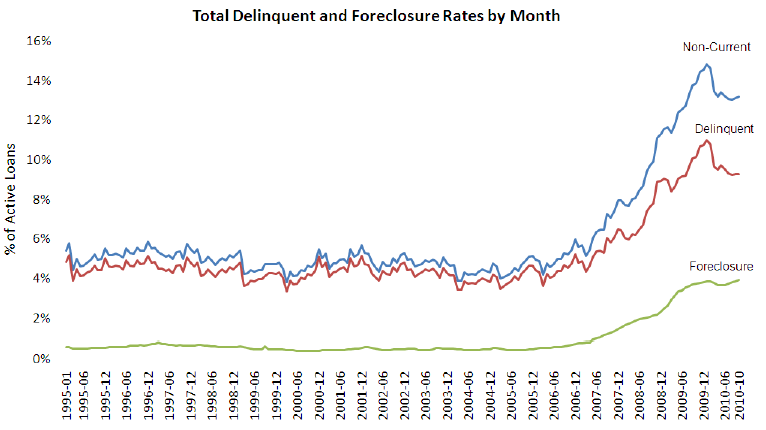

| Posted: 23 Nov 2010 06:40 PM PST It is hard to not laugh out loud at the amazing stupidity of those who say "It's Different Here". Please consider 'Low-doc' home borrowers hit by rising rates A new report shows a sharp increase in the number of 'low-doc' borrowers struggling to keep up with their mortgage repayments as interest rates rise.Progression of Rot Australia is starting to get hard but the important word in this sentence is starting. Rot starts at the edges and the outside periphery (subprime and low-doc), then spreads to the core. The party is now over as I mentioned in Partied Out: A Recap of Australia's Now Imploding Housing Bubble; Property Bull Offers Jeremy Grantham $100m Housing bet, Party is Not Over US Graphs, Statistics Here is a nice set of US stats and graphs from the LPS Mortgage Monitor: October 2010 "Dashboard" that depicts where Australia will eventually head. Total Delinquencies  Delinquencies remain about 2.7 times historical average, foreclosure inventories are 7.4 times and rising.  October Month-End Data: Conclusions

The housing rot in OZ has just started and it's a long way to the core. But it will get there. Australia can look forward to similar stats in years to come. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Buyers' Strike in Low-Yield Corporate Debt; Goldman's Bond Forecast Posted: 23 Nov 2010 01:53 PM PST Investors are starting to balk at buying more long-term corporate debt at record-low yields. Bloomberg reports Microsoft Record-Low Coupon Punishes Investors. Investors that helped companies from Microsoft Corp. to Wal-Mart Stores Inc. sell bonds at record-low borrowing costs are being punished on concern Federal Reserve efforts to stave off deflation will drive up yields.I would suggest the opposite of Goldman's forecast. I expect low-quality junk to get hit, perhaps seriously hit as the recovery stalls. JNK - Lehman High Yield Bond ETF  click on chart for sharper image The JNK ETF is a good proxy for low-quality "junk". Nearly everyone is underestimating the likelihood of a significant selloff in corporate bonds, especially junk, not because of a strengthening economy, but because of a weakening economy and rising default risk. Corporate bonds in general, and junk bonds in particular have been a one-way bet since mid-May. If the corporate bond market cracks, it will take the equities market down with it in a serious way. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 23 Nov 2010 11:12 AM PST News in Europe regarding Ireland, Spain, and Portugal is ominous. Credit Default Swaps (CDS) are soaring in Spain and Portugal. European sovereign risk jumped to an all-time high. Lloyds TSB says "Ireland's debt woes may spread because investors have lost confidence in policy makers". Members of his own party are calling on Irish Prime Minister Brian Cowen to resign. The quote of the day goes to Bill Blain, a strategist at Matrix Corporate Capital LLP in London who said ""Bailouts are nothing but a short-term string-and-sealing-wax fix". With that let's take a look at some specific news. Zero Confidence in Irish Solution Lloyds says Ireland's Woes May Spread on 'Zero Confidence' "The markets currently have virtually zero confidence that the bailout in Ireland will solve the European crisis even though fiscal austerity measures in both Portugal and Spain have been severe and prima facie, sufficient to ease market concerns," Charles Diebel and David Page, fixed-income strategists in London, wrote in an investor note today.Credit Default Swaps Soar in Spain, Portugal In spite of the Irish bailout, Spain, Portugal Bank Debt Risk Soars as Traders Look South The cost of insuring Spanish and Portuguese subordinated bank bonds soared as traders of credit-default swaps turned their focus to southern Europe following Ireland's bailout.Irish Prime Minister Brian Cowen Loses Confidence of His Own Party Members of his Fianna Fail Party may ask Cowen to Resign. Irish Prime Minister Brian Cowen may be asked to resign by some members of his Fianna Fail party as the parliament prepares to pass the country's 2011 budget, a lawmaker in the party said.Ireland Borrowing Costs 5%, Same as Greece Dutch Finance Minister says Ireland to Borrow From EU at Same Rate as Greece Ireland will pay about the same interest rate on emergency loans from the European Union as Greece, Dutch Finance Minister Jan Kees de Jager said.Dilution Concerns Plague Bank of Ireland Over bailout dilution concerns, shares of Bank of Ireland Plunge 31 Percent Bank of Ireland Plc, Ireland's largest bank, fell to a 20-month low on concern that shareholders will be diluted in any government bailout.Rescue Package Set at $114 Billion, 85 Billion Euros The cost of the bailout keeps going up. The original estimate was for a $50 billion bailout. Now, Ireland Said to Need 85 Billion Euros for Rescue European Union officials estimate that a rescue package for Ireland may amount to about 85 billion euros ($114 billion), according to two officials familiar with the talks.A tip of the hat to Bloomberg for every one of the above links. Ireland at Crossroads Here are my thoughts expressed in Irish PM Dissolves Government; Spanish Banks Face Debt Challenge; Greece May "Shut-Down"; Meaning of "Guarantee"; Should Ireland Ditch the Euro? Ireland is at a major crossroads. The fact that Irish Prime Minister Brian Cowen is willing to step down helps.Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Failure to Consider Constraints - My Response to "Has Mish Deflated the Inflationistas?" Posted: 23 Nov 2010 02:16 AM PST I am rather amused by an article on Mises by Robert P. Murphy called Has Mish Deflated the "Inflationistas"? I was aware this article was coming, Murphy told me in advance, and I rather expected some hard hitting piece on inflation (or at least some semblance of inflation discussion) saying why deflationists are wrong, and more specifically why my deflation theories are wrong. Instead Murphy outlines a number of allegedly bad calls I have made on the stock market, the US dollar, and treasuries. I admit I got some calls wrong, and Murphy did too as he admits. Actually anyone who makes short-term calls is bound to get a huge percentage of them wrong. Nonetheless I did call the top of the housing market on time in summer of 2005 as well as numerous real-time updates. For a synopsis of data points, please see Housing Update - How Far To The Bottom? I called the stock market top on the S&P 500 in July of 2007 in Quotes of the Day / Top Call. And no, I did not make numerous top calls on the way up. I was however, a few months and a few percentage points early. The Stock market made a new high in October. On the exact day the market topped, I received an email from someone telling me that he was having turkey for Thanksgiving and I was the turkey. I highlighted a sequence of treasury calls in Daniel Amerman vs. Mish: Reflections on the Great Inflation/Deflation Debate that I am quite proud of, but no I did not get every turn correctly. However, inflationistas have generally been wrong about treasuries for a decade. With most inflationistas screaming a dollar collapse is imminent, I have generally taken positions for a dollar rise when anti-dollar sentiment has been extreme. No my timing was certainly not always perfect, but I stand by the ideas I presented. While everyone was rah-rah on the Euro, I calmly pointed out problems in Greece, Spain, the Baltic states, and European banks that would matter. They did. And I think they will matter again. That I prematurely called the end of the recent bounce in the Euro is of little concern to me. I am not a day trader, or even a short-term trader. I am looking at the global economic picture, with eyes on risk management. Moreover, Murphy took statements out of context. In Time for a Dollar Bounce I said ... The time to be bullish on the Euro was at the 1.18 to 1.20 level, not now (although I suppose the Euro could bounce a bit higher still).In a complete distortion of reality Murphy translated my sentence "the possibility of the US dollar rising to 1.15 or even to parity vs. the Euro is not out of the question." into a short-term prediction the the Euro would soon fall to 1.15 even though I mentioned the possibility the bounce could go on longer, and I gave no timeframe for the drop. Moreover, Murphy fails to point out statements I have frequently made similar to these in a recent interview with Chris Martenson called "Straight Talk" with Economic Bloggers 9. What's the question we should have asked, but didn't? What's your answer?All things considered, I am pretty pleased with my calls, especially on gold, treasuries, and in spite of what Murphy says, the US dollar. Now About That Inflation Discussion?! Robert kicked off his article with a sentence "Over the last two years, I have gotten perhaps dozens of requests to "deal with" the deflationist approach of Mike "Mish" Shedlock." So where the hell was it? My long-term stock market call still stands: the bottom may or may not be in, however, the stock market is not a measure of inflation. Moreover, and although Murphy went to great lengths to point out the rally in equities, I calmly point out Japan had at least six 50% rallies in the last two decades but the Nikkei sits near 10,000 down from a high of 38,000. I still see no reason why the S&P could not or should not do the same. Indeed I did suggest this would play out over as long as another decade so I am not concerned about a single year that does not fit a pattern I suggested. I have also on numerous occasions, although not in the article he mentioned, pointed out alternate possibilities like a stock market that goes sideways for 5 years while earning catch up to valuations. The only statement Murphy made on the alleged topic of his post was that he and Gary North "think Bernanke has the power to raise prices if he so chooses". There was no discussion of ideas involving that belief. All we saw was a stated belief. We did not even see a definition from Murphy about what inflation is. Can Bernanke Force Prices Higher? I say not really, at least without serious consequences. I am not the only one who believes that. Ben Bernanke now believes that. Please consider Bernanke Calls On Congress To Help The Economy -- For At Least The Fourth Time In Five Months. For at least the fourth time since June, Federal Reserve Chairman Ben Bernanke publicly urged Congress to combat the lackluster recovery by increasing government spending, a recommendation that has gone unheeded by lawmakers.So while Murphy and North think Bernanke can force prices higher, even Bernanke finally admits he needs help. This by the way goes along with a statement that I have made numerous times over the years. "The FED can print money but it can not dictate where the money goes." If the Fed could dictate where it went, unemployment would not be near 10%, and prices would be going up 2% annually (Bernanke's inflation target). Rosenberg Says Deflation Coming Interestingly enough, the same day Murphy wrote his piece Dave Rosenberg, who does define inflation in terms of prices says DEFLATION COMING The year started out with the U.S. core (excluding food and energy) consumer inflation rate at 1.8% YoY; now, it is at a record low 0.6%. This has occurred even with massive government stimulus, U.S. dollar weakness, a commodity boom and an ongoing inventory cycle. Imagine what would happen if these developments reversed course. If Bernanke Wants 2% Inflation, Why Don't We Have It? Of course North and Murphy will point out that gasoline prices are soaring and they may claim food prices are soaring too, although I do not believe the latter and I do most of the shopping. Commodity prices certainly did soar. Regardless, that point is it is irreverent because Bernanke does not want oil prices or food prices to rise, he really wants housing prices to rise, and prices of stuff in general to rise. Yet, in spite of $2 trillion in agency purchases to support home prices and home sales, prices are falling and home sales are at all time record lows. Ignoring Constraint After Constraint Murphy ignores constraint after constraint. First off, I do not think Bernanke can cause prices to rise at will, but IF he can, it clearly is not the prices he wants. "The FED can print money but it can not dictate where the money goes, or indeed if it goes anywhere at all." Murphy and inflationistas need to read that sentence 100 times and understand the practical implications of it. Rising commodity prices without a pass-through to consumer prices kills profit margins and especially destroys small businesses. That fact imposes a serious constraint on Bernanke. Lack of Sales Still #1 Problem of Small Businesses Please consider NFIB Report Shows Lack of Sales Still #1 Problem of Small Businesses, Inflation Barely Registers Inflation Is A Non-IssueThe Fed can force prices up? Really? If the Fed could it would, and as I noted above the Fed admitted it cannot without the "help" of Congress. Fed Cannot Give Money Away Here is another constraint on the Fed: Unlike Congress, the Fed, cannot give money away. It simply cannot, at least legally, and that is a statement of fact. Sure the Fed can monetize the debt, and it is doing so right now, but anything in addition to that just may sit as excess reserves. If consumers do not want to spend, and businesses do not want to expand, there is not a damn thing the Fed can do about it. That is a statement of fact as well as a constraint on the Fed, and that is why Bernanke is running around like a chicken without a head right now, getting involved for the first time in history on fiscal stimulus issues. Fed's Obligation is to Banks Although I have pointed out the Fed cannot give money away, the simple fact of the matter is the Fed would likely not do it even if it could. The Fed does not want to wreck the banking system. The Fed is beholden to banks and does not really give a damn about consumers other than they earn enough to remain debt slaves forever. Turning Up The Heat On China Further comments from Bernanke about his struggles to create inflation and spur jobs can be found in Bernanke turns up heat on China currency policy. Federal Reserve Chairman Ben Bernanke put aside traditional central bank niceties and launched a direct attack on the slow pace of China's steps to strengthen its currency.Thus the actions of other governments pose additional constraints on the Fed. By the way, gasoline and commodity prices are more of a function of huge inflation in China, not the US. Both money supply and credit are soaring in china while credit collapsed in the US for 10 straight quarters. Inflation is rampant in China, not here. What About Negative Interest Rates? Gary North has made the claim the Fed could force banks to lend by announcing "from this point on, all money deposited by banks as excess reserves will be charged a storage fee. This fee could be 2%." Really? Perhaps Banks would buy short-term treasuries at 0%. Perhaps they would park the money in gold futures. However, even if the Fed could control those possibilities, there is still one other big constraint: Paying interest on reserves slowly over time helps to recapitalize banks. Force them to lend and losses increase. Bernanke wants to help banks recapitalize. He does not want banks to make poor loans just to make them. That is an obvious constraint that Gary North misses. Moreover there are new Basel capital requirements coming up. And finally, the reason banks are not lending is out of capital concerns. Banks need those "excess reserves" to handle additional (and huge) mortgage-related losses not yet realized. What the Fed Did and Why Inquiring minds may wish to read Ben Bernanke's Washington Post Op-Ed What the Fed did and why: supporting the recovery and sustaining price stability. The Federal Reserve cannot solve all the economy's problems on its own. That will take time and the combined efforts of many parties, including the central bank, Congress, the administration, regulators and the private sector.That's a heck of a lot of help needed. Admittedly the sentence says "solve all the economy's problems", but can the Fed solve any problems including Bernanke's concern over price deflation? Role of Attitudes Inflationistas in general simply do not understand the role of attitudes. If consumers do not want to spend they won't. Boomers are headed into retirement scared half to death. In aggregate they are looking to downsize, not upsize. They have insufficient savings. They no longer want to keep up with the Jones. Consumers are without a doubt cutting back on frivolous expenditures. This puts negative pressure on asset prices as well as the prices of goods and services. More importantly it puts huge stress on the demand for credit by businesses and consumers alike. Global Wage Arbitrage Let's not forget about global wage arbitrage. Even if Bernanke could force up prices, he cannot force up wages. Rising prices without rising wages would increase the number of defaults. State Cutbacks Let's not forget the implications of 6 New Governors Seek to Kill Defined Benefit Plans; 8 of 9 CA Cities Vote to Reduce Benefits; Fraudulent Promises (and what to do about them). We have yet begun to feel the deflationary economic implications of state cutbacks in employment, wages, and benefits. We will. And it is not at all in Bernanke's control. He needs help from Congress. I suggest he may get some help, but nowhere near as much as he needs. When Will the Inflation Genie Get Out of the Bottle? On December 14, 2009, in A Case for the Inflation Camp Robert P. Murphy asks When Will the Inflation Genie Get Out of the Bottle?Murphy's concern is over "excess reserves". My reason for expecting large-scale price inflation is fairly straightforward: I see no coherent strategy for Bernanke to remove the excess reserves from the banking system. ...Misguided Concern Over Excess Reserves Price increases showed up primarily in asset prices (but not housing), and also at the gas pump. However, they sure did not show up in the CPI as noted above. That's besides the point. The key point of discussion is Murphy's misguided notion that excess reserves work their way into the economy 10-times over spawning massive price inflation. That notion, although widely believed, is simply false. According to Money Multiplier Theory (MMT) and Fractional Reserve Lending, excess reserves may be lent out as much as 10 times over and when that happens, massive inflation will result. Money Multiplier Theory Is Wrong In Roving Cavaliers of Credit Australian economist Steve Keen has made a strong case that lending comes first and reserves later. I discussed that at length in Fiat World Mathematical Model. That point alone should seal the hash of the debate but it keeps coming up over and over. So let's try one more time. Please consider BIS Working Papers No 292, Unconventional monetary policies: an appraisal. Note: The above link is a lengthy and complex read, recommended only for those with a good understanding of monetary issues. It is not light reading. The article addresses two fallacies Proposition #1: an expansion of bank reserves endows banks with additional resources to extend loans Proposition #2: There is something uniquely inflationary about bank reserves financing From the article.... The underlying premise of the first proposition is that bank reserves are needed for banks to make loans. An extreme version of this view is the text-book notion of a stable money multiplier.There is much additional discussion in the article but it is clear that Money Multiplier Theory as espoused by Murphy, North and others did not happen in Japan nor is there any evidence of it happening in the US, nor is there a sound theoretical basis for it. In fiat based credit systems, lending comes first, reserves come second, and extra reserves do nothing much except pay banks to sit in cash in cases where interest is paid on excess reserves. Monetary Printing vs. Debt Deflation There is $35 trillion in credit on the balance sheets of banks, little of it marked to market. Yet, in spite of the fact that Money Multiplier Theory is totally bogus, supposedly printing $600 Billion to is going to cause serious inflation. The odds sure don't look very good to me. Practical Constraint Recap

In theory the Fed can cause inflation rather easily. In practice the Fed has to deal with many practical constraints. Murphy can believe what he wants but he sure did not address any issues of substance in his piece. By the way, I want to point out my definition of inflation and deflation once again. Inflation is a net expansion of money supply and credit, where credit is marked to market. Deflation is the opposite: a net contraction of money supply and credit, where credit is marked to market. By that definition, consumer prices and the stock market are symptoms of inflation and deflation not a definition of it. There are many more symptoms. Not all symptoms need be present all the time. Following the Path of Japan I have stated on many occasions that if deflation is defined as an increase in prices, we may or may not see it. By my definition we were in deflation in 2007 through March 2009 and we have probably been in inflation since then. I thought we were slipping back into deflation but the Fed temporarily put a halt to that with QE II. That does not mean the Fed will be successful. Indeed I think they won't be, at least on a permanent basis. I recently discussed this idea just a few days ago in Following the Path of Japan and the Madness of Bernanke Fighting Just That I have been saying for 5 years the US would follow the path of Japan. An interesting chart in the New York Times shows this is indeed what has happened.Bernanke's Deflation Prevention Scorecard In case no one is keeping track, Bernanke has now fired every bullet from his 2002 "helicopter drop" speech Deflation: Making Sure "It" Doesn't Happen Here. Bernanke's Scorecard Here is Bernanke's roadmap, and a "point-by-point" list from that speech. 1. Reduce nominal interest rate to zero. Check. That didn't work... 2. Increase the number of dollars in circulation, or credibly threaten to do so. Check. That didn't work... 3. Expand the scale of asset purchases or, possibly, expand the menu of assets it buys. Check & check. That didn't work... 4. Make low-interest-rate loans to banks. Check. That didn't work... 5. Cooperate with fiscal authorities to inject more money. Check. That didn't work... 6. Lower rates further out along the Treasury term structure. Check. That didn't work... 7. Commit to holding the overnight rate at zero for some specified period. Check. That didn't work... 8. Begin announcing explicit ceilings for yields on longer-maturity Treasury debt (bonds maturing within the next two years); enforce interest-rate ceilings by committing to make unlimited purchases of securities at prices consistent with the targeted yields. Check, and check. That didn't work... 9. If that proves insufficient, cap yields of Treasury securities at still longer maturities, say three to six years. Check (they're buying out to 7 years right now.) That didn't work... 10. Use its existing authority to operate in the markets for agency debt. Check (in fact, they "own" the agency debt market!) That didn't work... 11. Influence yields on privately issued securities. (Note: the Fed used to be restricted in doing that, but not anymore.) Check. That didn't work... 12. Offer fixed-term loans to banks at low or zero interest, with a wide range of private assets deemed eligible as collateral (…Well, I'm still waiting for them to accept bellybutton lint & Beanie Babies, but I'm sure my patience will be rewarded. Besides their "mark-to-maturity" offers will be more than enticing!) Anyway… Check. That didn't work... 13. Buy foreign government debt (and although Ben didn't specifically mention it, let's not forget those dollar swaps with foreign nations.) Check. That didn't work... Now What? I wrote about Bernanke's Deflation Prevention Scorecard in April 2009. Now, Bernanke is squealing like a stuck pig, begging Congress and China to help him produce price inflation in the US Regarding points 8 and 9 above: the Fed did purchase treasuries and agencies, but admittedly without an explicit ceiling. Theory and Practice Murphy claims "Bernanke has the power to raise prices if he so chooses". Can he? With whose help? At cost constraints Bernanke can ignore? In theory, the Fed can cause massive inflation at will. In practice, they can't. As Yogi Berra once quipped "In theory there is no difference between theory and practice. In practice, there is." You can lead a horse to money, you can't make him eat it. That's the very important difference. It's a question of attitudes. The Fed can certainly encourage inflation by offering money at seemingly attractive rates, but it cannot force the issue. Right now, neither consumers nor businesses want the risk. They are too loaded up with debt already, no matter how attractive the Fed wants debt to appear. It's like trying to give a kid one piece of cake too many. At some point, extra frosting makes the cake look less attractive, not more. At that point the kid will not take another bite. That is the point we are at now. The Fed is hoping Congress will eat more cake. It's up to Congress, not the Fed, and I doubt Congress want to eat as much cake as the Fed needs. Not Start of Blog Wars No sports fans this is not the start of blog wars. Although Murphy did an anemic job of covering any issues of merit regarding the inflation-deflation debate in his article, I wholeheartedly endorse his post My Debate Challenge to Paul Krugman in which he challenges Krugman to a debate on Austrian versus Keynesian business-cycle theory. Murphy has over $50,000 in pledges as of a couple weeks ago. The goal is $100,000. 95% of the pledges will go to the Fresh Food Program at FoodBankNYC.org. To make a pledge please click on Murphy-Krugman Debate. Beating Krugman should be easy enough, and the results should be entertaining. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment