Mish's Global Economic Trend Analysis |

- Gaming the Jobs Report: TimTabs +75,000, ADP +43,000, Bloomberg +60,000, Gallup Sees Unemployment Rising to 9.7% to 9.9%

- Trends in Rail Traffic

- Weekly Claims Show Job Stagnation for Entire Year

- October Retail Sales a "Strange Brew"

- 33% Tax Hike Will Hit Illinois; Another Stiffed Illinois Vendor Stops Servicing State; Common Sense in Tucson and Delta Airlines

- Three Reasons QEII Will "Backfire"; Pavlov's Dogs and the "No Choice" Argument Yet Again

- Chicago Natural Resources Expo November 5-6

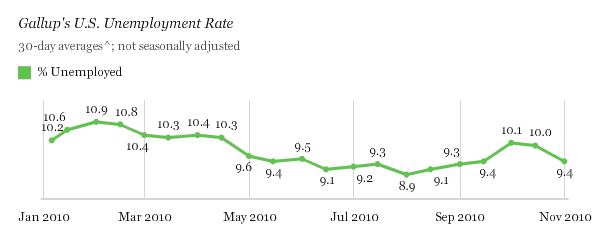

| Posted: 04 Nov 2010 08:52 PM PDT Friday's jobs reports will be out shortly. Here is how some see it, late Thursday evening. Gallup Gallup Finds U.S. Unemployment Likely to Be Up on Friday Gallup analysis suggests the October unemployment rate that the government reports on Friday will be in the 9.7% to 9.9% range. This is despite the fact that unemployment, as measured by Gallup without seasonal adjustment, fell sharply to 9.4% at the end of October -- down from 10.0% in mid-October and 10.1% at the end of September. Most of this drop took place after the official Labor Department measurement period, suggesting the government's October report may not pick up this late-month decline.Gallup was wrong each of the last two months. Do they have it correct this month? ADP The ADP National Employment Report Private-sector employment increased by 43,000 from September to October on a seasonally adjusted basis, according to the latest ADP National Employment Report® released today. The estimated change of employment from August to September was revised up from the previously reported decline of 39,000 to a smaller decline of 2,000. Since employment began rising in February, the monthly gain has averaged 34,000 with a range of -2,000 to +65,000 during the period. October's figure is within this recent range and is consistent with the deceleration of economic growth that occurred in the spring. Employment gains of this magnitude are not sufficient to lower the unemployment rate. Given modest GDP growth in the second and thirds quarters, and the usual lag of employment behind GDP, it would not be surprising to see several more months of lethargic employment gains, even if the economic recovery gathers momentum.ADP and Gallup say the same thing. More jobs, higher unemployment rate. TrimTabs Via email, no link available... Sausalito, CA – November 3, 2010 – TrimTabs Investment Research estimates that the U.S. economy added 95,000 jobs in October, the first monthly increase since May.That low in initial unemployment claims vanished today with an adjusted initial claims total of 457,000, an increase of 20,000 from the previous week's revised figure of 437,000. Bloomberg The Bloomberg Survey average was +60,000. The U.S. jobless rate held at 9.6 percent for a third month in October, according to a Bloomberg News survey before today's Labor Department report. Payrolls likely rose by 60,000, the first increase since May, a separate survey showed.Anything from +40,000 to +110,000 seems like a reasonable guess. I certainly would not be surprised to see a number in the upper end of that range. Stores are hiring, Black Friday sales are starting 3 weeks early, and ISM reports seemed surprisingly strong. However, I do not think positive surprises will hold. TrimTabs says it best "Economic growth is likely to stay sluggish because the private sector isn't able to pick up the slack from waning government stimulus. State and local government budget crises and the weak housing market will be significant drags on growth for a long time." Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 04 Nov 2010 04:27 PM PDT Rail traffic continues to recover, but from very depressed levels as noted on the Railfax Carloading Report. Changes Since 2007  13-Week Moving Average Projections  Railfax has modified their site to use Tableau software. Controls allow you slide bars to see any timeframes you want. Inquiring minds will want to check it out. I selected a timeframe of 2007 on. Interestingly, the top charts shows the recession bottom in summer of 2009 quite nicely. I am a big fan of Tableau Software but that second chart is fantasy material, especially the projection for cyclical traffic. The following table will help put things into perspective.  Total traffic is up 10.4% year to date vs 2009, but down 8.6% from 2008. Autos are up 24.2% vs 2009 but down 25.4% vs 2008. Some 17 months into a "recovery" we are not only below 2008 totals but 2007 totals as well. Moreover, much of the bounce we have seen has been inventory replenishment and the Fed knows it. If the real economy was not fragile as eggshells (broken is actually more like it), there would not be a QEII. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

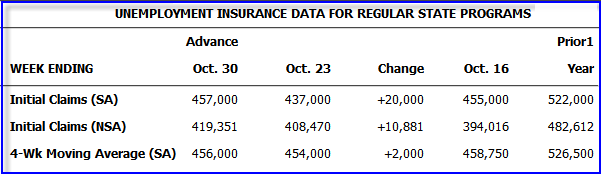

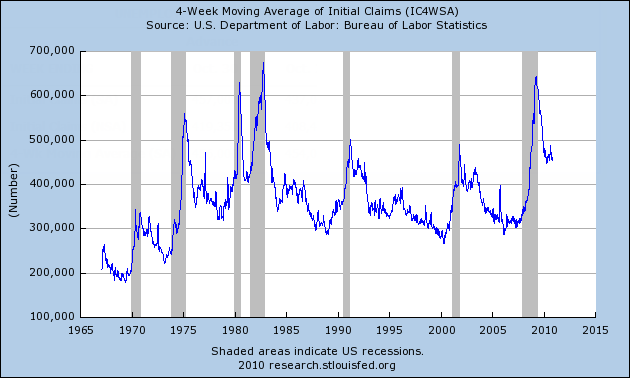

| Weekly Claims Show Job Stagnation for Entire Year Posted: 04 Nov 2010 12:57 PM PDT After movement in both directions over the past couple months, weekly claims are back where they have been for nearly a year, right around the 450,000 mark. Please consider the Unemployment Weekly Claims Report for November 4, 2010. In the week ending Oct. 30, the advance figure for seasonally adjusted initial claims was 457,000, an increase of 20,000 from the previous week's revised figure of 437,000. The 4-week moving average was 456,000, an increase of 2,000 from the previous week's revised average of 454,000.  The weekly claims numbers are volatile so it's best to focus on the trend in the 4-week moving average. 4-Week Moving Average of Initial Claims  The 4-week moving average is still near the peak results of the last two recessions. It's important to note those are raw numbers, not population adjusted. Nonetheless, the numbers do indicate broad, persistent weakness. 4-Week Moving Average of Initial Claims Since 2006  No Lasting Improvement for 12 Months There has been no lasting improvement for nearly a year. Weekly claims have generally been in the 440,000 to 480,000 range with the 4-week moving average practically pinned to the 450,000 mark. To be consistent with an economy adding jobs coming out of a recession, the number of claims needs to fall to the 400,000 level. At some point employers will be as lean as they can get (and still stay in business). Yet, that does not mean businesses are about to go on a big hiring boom. Indeed, unless consumer spending picks up, they won't. Questions on the Weekly Claims vs. the Unemployment Rate A question keeps popping up in emails: "How can we lose 400,000+ jobs a week and yet have the unemployment rate stay flat and the monthly jobs report show gains?" The answer is the economy is very dynamic. People change jobs all the time. Note that from 1975 forward, the number of claims was generally above 300,000 a week, yet some months the economy added well over 250,000 jobs. Also note that the monthly published unemployment rate is from a household survey, not a survey of payroll data from businesses. That is why the monthly "establishment survey" (a sampling of actual payroll data) is not always in alignment with changes in the unemployment rate. At economic turns the discrepancy can be wide. Where To From Here? Four weeks ago the weekly claims print was 475,000. That number will roll off the 4-week moving average next week. Thus any number lower than 475,000 will cause the 4-week moving average to drop. Assuming we get a print of 450,000, next week's 4-week moving average will decline to ... drum roll please ... 450,000. As measured from weekly claims, the economy has been stagnant for a year. However, there is upward pressure on the number in light of cutbacks by state and local governments. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| October Retail Sales a "Strange Brew" Posted: 04 Nov 2010 11:10 AM PDT Retailers report luxury sales are up but so are sales at Walmart and Costco. Meanwhile other stores like JC Penny and Kohl's are using the old standby of blaming the weather for lack of sales. Promotions started early this year because of lack of demand, hardly a sign of strength. Moreover, October is a weak month. Given that sales last year were especially weak, year-over-year comparisons are suspect. Thus, it's hard to make much of anything from retail sales reports in an aggregate sense, but there are some interesting trends at individual store levels. The New York Times reports Retailers Tally a Mixed October as Sales Rose 1.6% At the 28 stores tracked by Thomson Reuters, an index that excludes the nation's largest retailer, Wal-Mart, there was a 1.6 percent increase in sales at stores open at least a year. That met analysts' expectations, and marked the 14th month of increased sales. But the positive results have been compared with months last year that had significant declines because of the economic downturn.Selective Shopping The Wall Street Journal mentions "selective shopping" in Retailers Showing Mixed October Sales Results "There is a market-share war that is heating up as we move into the holiday season and some retailers evidently are already pulling out the big guns, creating winners and losers," said John Long, retail strategist at Kurt Salmon Associates.Explaining the Strange Brew It seems easy enough to figure the surge in luxury spending can be attributed to the stock market rally. However, the good news pretty much seems to end there. Walmart is up but J. C. Penney, Kohl's, Stage Stores, Macy's and Stein Mart all blame the weather. Teen Sales Telling The teen retailer segment was anemic with the exception of Zumiez which reported a 21.5 percent increase. However, last year the store had a decline of 8.9 percent. Perhaps a reflection of age, I have to admit I have never seen a Zumiez store but I certainly have been in many Abercrombie & Fitch, American Eagle Outfitters Inc, and Hot Topic stores (the latter out of curiosity). Given the number of struggling families where every penny counts and given high teen unemployment, one should not be surprised by the poor performance in the teen group (discounting Zumiez as an outlier). Late October Surge The above articles mentioned a surge in late October spending. That surge was picked up in a Gallup survey. However, Gallup claims a pickup in spending in late October is the typical pattern. See Gallup Surveys Shows Anemic October Consumer Spending, No Pickup in Christmas Spending Plans for details. Consumer Squeeze That Walmart and Costco are doing well is a sign of a consumer squeeze, not a sign of strength. All of this points to a mediocre Christmas. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 04 Nov 2010 09:52 AM PDT Illinois has a $13 billion and growing deficit. The current backlog of bills approaches $6 billion. The state has not paid some suppliers for seven months. In response some vendors have stopped doing business with the state. Please consider Another vendor quits doing business with Illinois Records show the Illinois Department of Corrections was forced to scramble this week when a vendor refused to deliver foam food trays to Menard Correctional Center because it hadn't been paid. Industrial Soap Co., which holds the master contract for the foam trays, "will not deliver due to delinquent invoices," prison officials noted.33% Tax Hike Coming to Illinois Illinois voters likely returned Governor Pat Quinn to office. Their reward will be a 33% tax hike, if Quinn gets his way. The election is still undecided 2 days later. Quinn's lead is 16,000 or so out of over 3.6 million cast. Absentee ballots have yet to be counted. However, the math looks improbable for challenger Bill Brady. The problem for Brady is he barely got 20% of the vote in a packed Republican primary. 80% of Republicans wanted someone else. Brady generated little enthusiasm, and none from me, except for one thing: He was not Quinn. For most voters, that was not enough. Chicago voted overwhelmingly for Quinn, 86% to 14% or so. His solution is to the mess is a proposal to raise state taxes by 33%. Congratulations to Delta The Star Tribune reports Delta attendants say 'no' to union Flight attendants at Delta Air Lines narrowly rejected union representation in the first of three votes to organize the majority of employees at the world's second largest airline.Common Sense in Tucson Common sense ruled in Tucson where voters rejected a tax hike give away to public union workers. The Arizona Daily Star reports Tucson City Manager: 400 workers face layoff. A day after a city sales tax hike was soundly rejected by voters, Tucson City Manager Mike Letcher and Mayor Bob Walkup announced an estimated 400 city workers could be laid off.Voters are not necessarily demanding fewer workers, they simply want more for their money. Not a single city worker has to be laid off. All that has to happen is for the unions to lower salaries and pensions to meet the budget. This is not the voters' fault, 100% of the blame for the layoffs go to the unions. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Three Reasons QEII Will "Backfire"; Pavlov's Dogs and the "No Choice" Argument Yet Again Posted: 04 Nov 2010 01:16 AM PDT Dr. El-Erian, CEO and co-CIO of PIMCO states several reasons why QEII will backfire. 1. The Fed is going it alone, without meaningful structural reforms 2. Emerging economies burdened by capital inflows in the wake of QEII will react with currency wars, protectionism, and capital controls 3. Resultant commodity price increases will increase input costs and reduce earnings of American companies The position of El-Erian is interesting given that PIMCO founder, managing director and co-CIO endorsed QEII as discussed in Bill Gross' Arrogant Endorsement of Fed's QE Policy he calls History's Most "Brazen Ponzi Scheme". Unintended Consequences of QEII Mohamed El-Erian addresses the unintended consequences of Fed policy actions and the reasons Quantitative Easing will fail in QE2 blunderbuss likely to backfire. The Fed faces three problems, with its solo role being the first. Having warned in late August in Jackson Hole that "central bankers alone cannot solve the world's economic problems", Ben Bernanke, the Fed's chairman, is now leading an institution that is virtually on its own among US policymakers in meaningfully trying to counter the sluggishness of the US economy and the stubbornly high unemployment.Pavlov's Dogs and the "No Choice" Argument Yet Again Although I agree with the three major points above, I certainly do not concur with El-Erian's opening gambit "Given the high market expectations, the US Federal Reserve had no choice but to announce a second tranche of quantitative easing". Pray tell who set those expectations if not the Fed? Moreover, given the market reacted like Pavlov's Dogs to the announcement, the Fed could have and should have toned down market expectations. Finally given that the Fed produced a bubble in junk bonds and sent commodity prices soaring the Fed had every reason to disappoint the market today. For more on junk bonds please see ...

Intended vs. Unintended Consequences Add a junk bond bubble to the list of consequences (unintended or otherwise). Bernanke is clearly misguided enough and arrogant enough to purposely blow a junk bond bubble as an "intended consequence", even though the housing bubble bust proves without a doubt the asininity of such policies. Thus, it's hard to say if Bernanke wants a junk bond bubble or is merely willing to live with one. Then again, Bernanke is dense enough to not have any clues about what is happening. He did not see the housing bubble, the recession, the huge rise in unemployment, and any number of other things that happened. In fact, he even denied there was a housing bubble. In the academic wonderland in which Bernanke lives, it is perfectly possible he is oblivious to the bubbles he is creating. However, looking at things from every angle, given that Bernanke Admits Targeting Stock Prices, I am leaning towards the first option: Bernanke is misguided enough and arrogant enough to purposely blow more asset bubbles as an "intended consequence", hoping he can deal with them later. Missing the Obvious I touched on the one obvious reason QEII will fail in QEII Announced, Fed Set to Buy $600 Billion in Bonds, Reinvest $250 Billion More; Fed Micromanaged Economy to Oblivion; No Miracles Coming Doubts? What Doubts?No One Has To Do Anything It is disappointing to see El-Erian perpetuate the myth the Fed had to do something when one of the biggest reasons we are in this mess is a activist Fed under both Greenspan and Bernanke felt the need to do something about LTCM, Y2K, the Dot-Com bubble, housing, motherhood, and apple pie. At least El-Erian is not defending what Gross calls a "Ponzi Scheme" to the same foolish extent that Bill Gross did. More importantly, El-Erian makes it clear exactly what some of the consequences are, while the Gross article sounds like "jumping the shark". Structural Reforms El-Erian said "Without meaningful structural reforms, part of the Fed's liquidity injection will leak right out of the US and result in yet another surge of capital flows to other countries." I agree, but I rather doubt we are talking the same language. This country needs to ...

Fed Fights Battle that Cannot be Won, Should Not be Fought Given that Congress is unlikely to do many, if indeed any of those things, the Fed is fighting a battle that cannot be won and should not be fought. We are in this mess because the Fed micro-mismanaged the economy at every critical juncture while attempting to smooth over various fiscal insanities, counter bad Congressional policies, as well as deal with the repercussions of its own monetary insanities, on a delayed chasing-its-tail basis, in a global economy that waits for no one. Is it any wonder the Fed failed in dual mandate of price stability and maximum growth? For more on the silliness of the Dual Mandate as well as a rebuttal to the notion "Don't Fight the Fed" please see Krugman and the Inevitable "I Told You So" - Tim Duy "Bad Things Happen When You Fight the Fed"; Final End of Bretton Woods 2? With that key idea in mind, there are two more structural reforms glaringly lacking in the above list: Abolish the Fed and End Fractional Reserve Banking. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Chicago Natural Resources Expo November 5-6 Posted: 03 Nov 2010 11:40 PM PDT Those in the greater Chicago area are welcome to attend the Chicago Natural Resources Expo on November 5-6 for a discussion about gold, silver, hard assets, inflation, currencies (or whatever else is on your mind) and to meet with various natural resource company executives. For all the deflationists in the crowd, I am once again pleased to announce the magic words: "It's free". Originally known as the Chicago Natural Resource Conference and Exhibition, this is one of the oldest natural resource conferences in the United States. The conference is a semi-annual event and offers opportunities to learn about new and undervalued companies in the natural resource industry.I will be on the panel Friday evening and Saturday afternoon along with Ty Andros, Clyde Harrison, and others. Saturday lunch is free also (but you do have to put up with listening to me on the panel). Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment