Mish's Global Economic Trend Analysis |

- Clarification on Freddie Mac Mortgage Fees; A Look at Why Your Credit Score is Important

- Weekly Claims Sharply Lower to 407,000, Best Performance Since July 2008; Dollar Firm, Treasuries Lower; Looking Ahead

- Freddie Hikes Mortgage Fees .25 Points; Fed Report shows Mortgage Borrowers Deleverage; Mortgage Spreads Highest in Year

| Clarification on Freddie Mac Mortgage Fees; A Look at Why Your Credit Score is Important Posted: 24 Nov 2010 12:03 PM PST I received a couple of emails regarding Freddie Hikes Mortgage Fees .25 Points; Fed Report shows Mortgage Borrowers Deleverage; Mortgage Spreads Highest in Year Dan Hughes at Summit Mortgage writes ... Reuters reporter Al Yoon conflated fee changes regarding Loan-to-Value ratios of 75% with a need for borrowers to get "Mortgage Insurance".In response to that email and after a review of the actual document from Freddie Mac, I revised the title of my earlier post, stripping out the reference to mortgage insurance. I will add an addendum to that post, pointing to this one. Freddie Mac Bulletin Inquiring minds are reviewing the November 22, Freddie Mac Explanation of Service Bulletin 2010-30. Effective date: March 1, 2011 In this Single-Family Seller/Servicer Guide ("Guide") Bulletin, effective for all Mortgages sold to Freddie Mac with Settlement Dates on or after March 1, 2011, we are revising our postsettlement delivery fees ("delivery fees"). For certain Mortgages, we are:

Freddie Mac Fees  click on table for sharper image The main difference from before is the extra .25 point borrowers have to pay if they do not put down 25%. For some credit scores, fees went up by .50 points. There is no reference to Mortgage Insurance. Why Your Credit Score Matters Looking to buy a house or refinance? Take a look down that table and see what happens.

Both people I talked to today said these values are rigid. If you are looking to refinance or buy, and you are close to a major cutoff, small differences in credit scores can be a big deal. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 24 Nov 2010 10:21 AM PST In the best performance since July 2008, weekly unemployment claims fell sharply to 407,000. The 4-week moving average dropped to 436,000. In response, the dollar was firm and US treasuries had a mild selloff. Bloomberg reports U.S. Jobless Claims Decline to Lowest Since July 2008 Applications for unemployment benefits in the U.S. fell more than forecast last week to the lowest level since July 2008, reinforcing evidence the labor market is healing.Seasonal Adjustment Outlier? Before anyone gets too excited over today's numbers, the last paragraph above may help explain what is going on. Retailers have been ramping up with temporary holiday hiring at the fastest clip in years. Whether that translates into long-term employment remains to be seen. Seasonal adjustments have been unusually large recently, for reasons not explained by the BLS. For a better look at what's really happening, please see ...

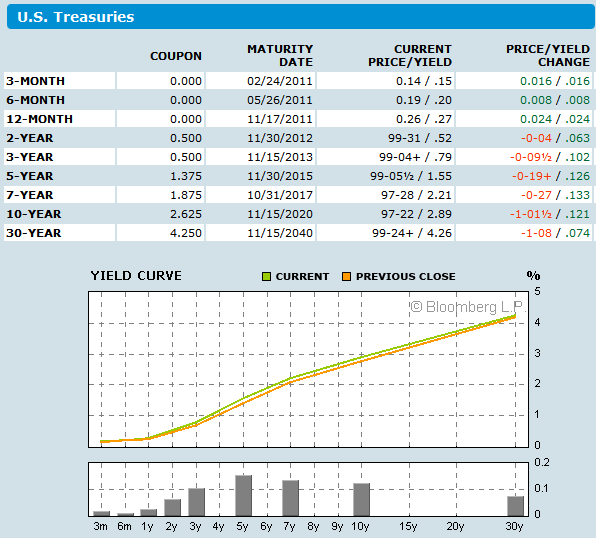

Looking Ahead I suspect things are improving, for now, although not at the rate implied by this decrease, and not enough to put any kind of dent into the unemployment rate. Looking ahead, we have mighty high expectations of Christmas sales, and nearly everyone has failed to factor in the effect of state cutbacks. Moreover, within the next two months, 2 million people are set to use up all of their unemployment insurance benefits, maxed out at 100 weeks. With recent news on jobs, real or imagined, Republicans may be less inclined to extend those benefits in the lame-duck Congressional session. Regardless, structural headwinds are enormous. Yield Curve as of 2010-11-24  Once again we see an unwinding of the QE II sure-thing trade, with the middle part of the yield curve selling off at the fastest rate. 7-Year Treasury yields rose 13 basis points, but 30-year treasury yields only rose 7 basis points. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

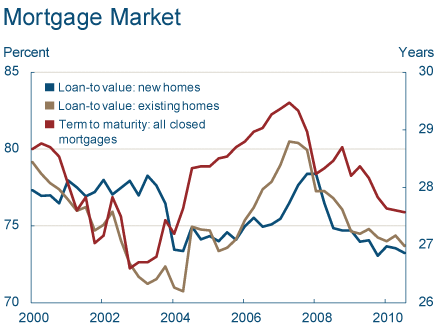

| Posted: 24 Nov 2010 01:05 AM PST Congratulations to anyone who refinanced last month. That may have been the bottom in mortgage rates. 15 and 30-year fixed mortgage rates have climbed by about a quarter of a point from a month ago, and rates will climb another quarter of a point for many borrowers. correction The above sentence was based on statements in a Reuters article confusing the need for mortgage insurance with other changes in Freddie Mac fees. The statement is inaccurate and has been stricken. Please see my post Clarification on Freddie Mac Mortgage Fees; A Look at Why Your Credit Score is Important for details. Expect Fannie Mae to follow. If so, the wave of refinancings we saw this year, may be about over. Please consider Freddie Mac says to hike fees on some mortgages Freddie Mac, the second-largest provider of funding for U.S. home mortgages, will raise some fees on loans it finances, a sign it sees greater risks even for borrowers making regular payments.correction The paragraph in italics above is incorrect as are other paragraphs in the article itself. Once again, please see my post Clarification on Freddie Mac Mortgage Fees; A Look at Why Your Credit Score is Important for details. Mortgage Rates  Mortgage rate table courtesy of Bloomberg. Mortgage Bond Spreads Relative to Treasuries Climb Please consider Low-Coupon Mortgage Bond Yield Spreads Climb to Highest in Year Yields on Fannie Mae and Freddie Mac mortgage securities that guide home-loan rates rose to the highest in more than a year relative to 10-year Treasuries.Mortgage Borrowers Deleverage The Cleveland Fed reports Mortgage Borrowers Deleverage The housing bubble that preceded the last recession left many borrowers overleveraged once the recession struck. According to the Board of Governors, from March of 2000 to September of 2007, the homeowner mortgage obligation ratio, which measures the outstanding value of mortgage payments as a percentage of disposable income, grew from 8.6 percent to 11.3 percent. However, since the peak of the last business cycle in 2007, consumers have begun to deleverage their balance sheets. This trend is evident in the housing market where consumers have been reducing their exposure to mortgage debt by financing more home purchases with cash and reducing both the loan-to-value ratios and the term to maturity of their mortgage debt.Deleveraging attitudes are making Bernanke's life miserable. Debt payback is not what Bernanke wants even though it is the best thing for the economy long-term. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment