Mish's Global Economic Trend Analysis |

| No "Miracle" Cures from Inflation; Impossible to Inflate Out of this Mess Posted: 24 Apr 2011 07:29 PM PDT Inquiring minds are reading The "Miracle" of Compound Inflation by John Mauldin. Here are a few paragraphs worthy of a closer look. Albert Einstein is famously quoted as saying, "Compound interest is the eighth wonder of the world." And compounding is indeed the topic of this week's shorter than usual letter, but compounding not of interest but of inflation.Whoa!

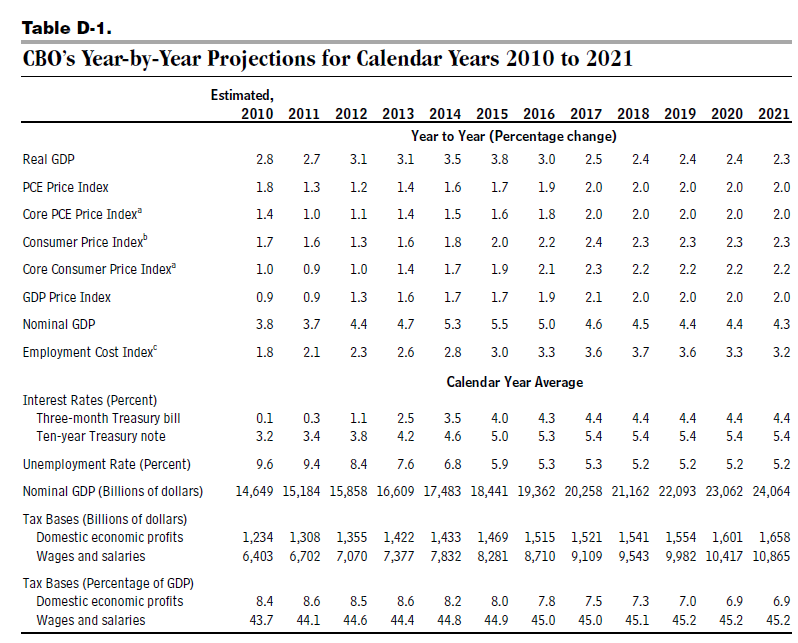

Mauldin is correct about the "insidious nature of inflation". Unfortunately, Mauldin then provides an example that suggests inflation is a "tried and true" way of dealing with debt. Let's quickly dispel such thinking starting with a look at interest on the national debt and health-care costs. Health-Care Costs Mauldin said "Don't even ask about health-care costs." Well we have to ask about them. If health-care costs rise sharply, so will Medicare and Medicaid expenses unless they are capped. Mauldin proposed such a cap to make his "what-if" model work. Unfortunately, it is not rational to assume such a cap, nor is it rational to think other government expenses such as road-work, food stamps, education spending would be capped either. Interest on the National Debt Speaking of caps, there is no way to cap interest on the national debt except by eliminating the debt entirely. I discussed interest on the national debt in Interactive Map: Paul Ryan vs. Obama Budget Details; Path of Destruction Here are the pertinent charts but please take a look at the entire post if you have not seen it. Deficit: Obama vs. Paul RyanCBO Analysis Mauldin continues, and gets back on much firmer ground with a critique of CBO analysis. What the CBO AssumesWhat Happens at "Modest" 4% Inflation? Now that we have interest rate and inflation assumptions from the CBO, let's take another look at what might happen with 4% inflation. The CBO projects the CPI will peak at 2.3% except for 2017 at 2.4% (quite an assumption). The CBO also projects short-term interest rates to be about 2 points higher than CPI, and 10-year rates at 3 points higher than the CPI. Using those guidelines, at 4% inflation, short-term interest rates would be 6%, and 10-year rates would be 7%. National debt will rise to $23-26$ trillion in the Obama -Ryan scenarios shown above. At 4% inflation (and 6% interest rates) what would interest on the national debt be? At 6% interest, interest on $26 trillion would be $1.56 Trillion a year. However, that statement assumes we got to 2021 and then interest suddenly spiked to 6% and all the revenue assumptions held up. It would not work that way in practice. Remember that we are running budget deficits and adding to the national debt under every scenario proposed so far. If we had 4% inflation along the way, interest on the national debt would rise sharply every year and that amount would add to the cumulative debt, as would any revenue misses. If we had 4% inflation, would we have the revenue growth as presumed in Mauldin's "what-if" example? I highly doubt it. However, we can be sure that government expenditures would rise. Also note that even IF revenues rose with inflation, so would government expenditures on health-care, road work, education, food stamps, etc unless one makes irrational assumptions. Thus any scenario that suggests a budget surplus is possible with 4% inflation is preposterous. What About Another Recession? Finally, and as Mauldin correctly pointed out, the chance of a recession in the next 10 years is quite high. Indeed, I think it is likely there are two or more recessions in the next decade. Thus, the CBO estimate, Ryan's estimate, and president Obama's estimate are all unrealistically optimistic. Locking in Long-Term Rates Ironically, the Fed could take advantage of low interest rates now by locking in favorable long-term rates now just as corporations have done. Instead of buying treasuries and bloating its balance sheet, in theory, the Fed could have been selling treasuries, locking in debt at exceptional prices under 4.5% for 30 years, or 10-year debt at 3.4% (and could have done much better some time ago). I said, "in theory" because that action would have reduced money supply, and Bernanke believes tightening money supply in the Great Depression made matters worse. Exit Strategy Will Put Upward Pressure On Yields Today the Fed has a different problem of its own making. The Fed's balance sheet is stuffed with treasuries. Attempts to unload them would put upward pressure on yields regardless of what Bernanke says about his exit strategy (or lack thereof). Impossible to Inflate Out of This Mess The idea that inflation is a "tried and true method" of dealing with debt is complete Keynesian foolishness. Inflation is never a cure, it only seems to work in the short run. Please consider these Statements of Ludwig von Mises regarding Interest, Credit Expansion, and the Trade Cycle. There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of a voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.Tried and True Illusion Careful analysis including a look at interest on the national debt and other government expenditures shows there are no "miracle" cures from inflation, only a temporary illusion of success, much like the illusion that the housing bubble represented a solution to the collapse of the dot-com bubble. Inflation it is the disease. Deflation is the cure, but it sure will not be painless. In the meantime, the Monetarist clowns at the Fed and the Keynesian clowns in government are simply digging a bigger hole, cheering the illusion of success of ever-bigger bubbles. The collapse of the housing bubble should be proof enough that the model does not work, yet Keynesian clowns everywhere persist with proposals that have never worked in practice, and cannot possibly work mathematically. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Collateral Damage: Tenant Victims of Foreclosed Properties Posted: 24 Apr 2011 08:40 AM PDT Preposterous rules in Florida do not allow renters to pay water bills of foreclosed landlords who have closed accounts. The result is many surprised tenants wake up one morning, find their water shut off, and have no way to get it turned back on. Please consider Collateral damage: Tenants of foreclosed properties Whenever Michel Joseph wants to shower, cook or use the bathroom, he has to leave his Little Haiti apartment and drop in on a neighbor who has running water.Imagine wanting to pay money for a service and being unable to do so. Imagine being without water for four months. In other cases, in other states, tenants have been given as little as an hour or less to pack their belongings and leave. Some states have passed laws to deal with these situations but this is 4 years into the crisis. How long does it take bureaucrats to think and act? The answer obviously is 4 years an counting. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment