Mish's Global Economic Trend Analysis |

- Gold - a Flight to Quality

- Economic Turmoil in Europe: Political Backlash and a Euro-Nordic Headache

- Interactive Map: Paul Ryan vs. Obama Budget Details; Path of Destruction

| Posted: 20 Apr 2011 09:40 PM PDT The New York Times reports Gold Tops $1,500 an Ounce in 'Flight to Quality' The list of factors that have supported the price of precious metals in recent weeks is long. It includes worries about the sustainability of European debt levels — and whether countries like Greece will soon default; the threat of a possible downgrade of U.S. credit ratings amid an impasse over raising the debt limit and dealing with the budget deficit; the weaker dollar; rising inflation in many parts of the world and continued unrest in North Africa and the Middle East, which has pushed up oil prices.Orderly Move Higher Unlike other commodities that have skyrocketed and crashed, the climb in gold has been very orderly. It is the only commodity whose long-term trendline is long and unbroken.  Click on chart for sharper image. Gold could take a substantial hit, just as it did in 2008 and still keep its long-term trendline intact. Why is that? The answer is currency debasement. A few charts from Interactive Map: Paul Ryan vs. Obama Budget Details; Path of Destruction will show what I mean. Deficit: Obama vs. Paul Ryan  Interest on the National Debt: Obama vs. Paul Ryan  National Debt: Obama vs. Paul Ryan  National Debt is going to soar in 10 years from $15 trillion to $23-26 trillion if either Obama's or Ryan's plan is enacted. That is currency debasement on a scale never seen before in the US. However, it is not just the US. The UK is a financial basket case and in Europe there is a sovereign debt crisis. In China, credit is expanding at 20-30% a year. Indeed, China is printing money faster than the US. Thus, the idea the Yuan is undervalued is questionable to say the least. For further discussion regarding China and the Yuan, please see Is the Yuan Undervalued? So, why shouldn't gold be rising? If anything, the surprise should be how orderly the rise has been given massive currency debasement everywhere you look. Gold is Money Merrill Lynch analysts wrote "Gold is sometimes a currency, sometimes a commodity and sometimes a store of value." Those Merrill Lynch analysts make a number of mistakes. The fact of the matter is gold is always a currency and always a commodity. I make the case "Gold is Money" in two posts. Money is Always a Commodity Please consider a few re-ordered sentences from Murray Rothbard's classic text What Has Government Done to Our Money? Money is a commodity used as a medium of exchange.What Is The Proper Supply Of Money? Continuing from the book ... Now we may ask: what is the supply of money in society and how is that supply used? In particular, we may raise the perennial question, how much money "do we need"?The above online book found on mises.org is a great read. It is also free. It should be required reading for all members of Congress. Please meet with your legislative representative and get them to read the book. The key point above is that money is a commodity. Yet unlike other commodities, an increase in money supply confers no overall economic benefit. Over time, money simply buys less and less. Those three sentences and one look at the budget charts above nicely explain the rise in gold. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||

| Economic Turmoil in Europe: Political Backlash and a Euro-Nordic Headache Posted: 20 Apr 2011 11:11 AM PDT Dan Steinbock, writer for The Globalist sent an interesting story he wrote regarding the Euro Crisis: Economic Turmoil, Political Backlash in the wake of the Finnish election results and the rise of the "True Finns". What follows is partial excerpt of that story, starting with a section titled "The Euro-Nordic Headache". I am not going to do my normal blockquote so as to make what follows easier to read. Everything that follows is from Dan Steinbock. The Euro-Nordic Headache The [Finnish] election took place only days after Portugal became the third euro member to seek a bailout and market speculation grew over impending debt restructuring in Greece.

With their strong election performance, the True Finns could disrupt efforts to tackle the euro debt crisis because Finland, unlike other euro countries, requires approval from its parliament to participate in EU bailouts.

Even before the election, the largest opposition party, the Social Democrats, led by chairman Jutta Urpiainen, began setting conditions on support for Portugal. Following in their footprints, the conservative Finance Minister Jyrki Katainen and Prime Minister Kiviniemi called for harsher measures in the case of Portugal.

Now Katainen is expected to become the next conservative prime minister, replacing Kiviniemi, whose Center Party plunged from first to fourth place since the 2007 election.

In Brussels and Lisbon, a Katainen-led government would ease angst because it is seen as pro-EU and supportive of the Portuguese bailout. Conversely, with their election gains, the True Finns will seek a majority that allows them to block the euro region's bailout mechanism.

Since the election result means complicated inter-party negotiations for a coalition government, it will be difficult for the Finnish parliament to make a decision on the Portuguese rescue plan by next month, when Lisbon seeks to complete the package.

Further, the government is expected to include at least one anti-bailout party — either the True Finns or the Social Democratic party, which voted against previous rescue packages for Greece and Ireland.

Since EU rules require unanimous approval for each euro bailout fund, Finnish support is vital — it is one of the few remaining AAA-rated euro economies. However, euro officials are exploring options for the Portuguese deal without the Finns, if necessary. After economic turmoil, political shift

In most competitiveness rankings, the Nordic economies are among the global leaders. As small and open economies, however, their prosperity is predicated on the growth of their major trade partners, the large EU economies and the United States. In Finland, for instance, the EU dominates almost 60% of all exports and over 80% of all direct investment abroad.

Amidst the global financial crisis, euro governments saved their banks at the expense of the taxpayers. Now the economic crisis is generating a political backlash — from the small Nordics to the large EU economies.

In 2007, the Danish People's Party received a 13.9% vote share in the parliamentary election. Two years later, the Norwegian Progress Party raked in 22.9%. Last fall, the right-wing nationalist Sweden-Democrats garnered 5.7% of the popular vote.

Germany is amidst seven elections in the 16 federal states, which are hammering Chancellor Angela Merkel's Christian Democratic Union (CDU). The support for its coalition partner, the Free Democratic Party (FDP), has collapsed.

In France, President Nicolas Sarkozy's centre-right Union for a Popular Movement (UMP) party suffered in regional elections last month, amidst a strong performance by the far-right National Front. In Italy, the Northern League, an anti-immigration party pivotal in Prime Minister Silvio Berlusconi's coalition, has seen its support double in the past five years.

In June 2010, elections in Belgium led to a landslide victory for the separatist and conservative New Flemish Alliance in Dutch-speaking Flanders. In Holland, the far-right Geert Wilders could become the next Dutch prime minister after significant gains in the recent regional elections.

In the absence of a comprehensive solution, euro leaders are scrambling to bail out, or bail in, one crisis economy after another. As long as the countries to be rescued have been small — accounting for less than 2.5% of the eurozone's total GDP — the problems have been averted. But after Portugal, the spotlight will shift to Spain, which contributes 11.5% of eurozone GDP.

Unfortunately, the problems are systemic. Neither muddling through the economic turmoil nor nationalist political shifts will resolve the problems. The euro crisis is not just about liquidity — it is primarily about solvency. The advanced economies can live beyond their means some of the time, but not all of the time.

Amidst the broadening political backlash, Europe has few alternatives left. It must move toward deepening integration, or cope with greater fragmentation. The above courtesy of Dan Steinbock and the Globalist. Thanks Dan!Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||

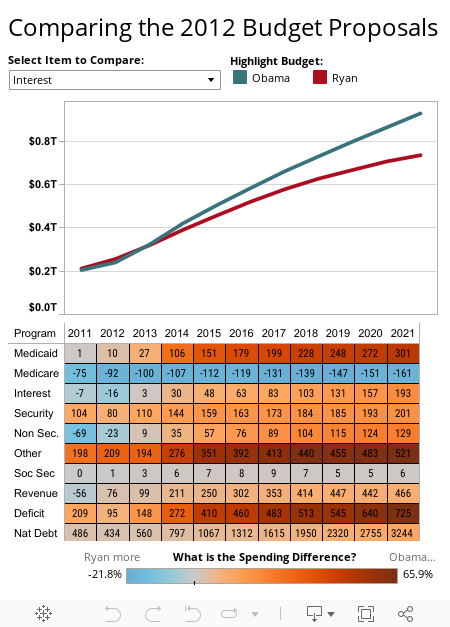

| Interactive Map: Paul Ryan vs. Obama Budget Details; Path of Destruction Posted: 20 Apr 2011 01:59 AM PDT I have been digging into the details of President Obama's budget plan vs. Paul Ryan's budget plan. What I found was so sickening that I asked my friend Ross Perez at Tableau Software for a display. The interactive map below may take a few seconds. It will be worth your wait.  Select from the dropdown box for a list of items you can chart. You can also hover over any of the orange or blue boxes for a popup display comparing the budgetary difference between the Obama and Ryan proposals for that year, for that item. Boxes in blue are years in which Paul Ryan has budgeted more for an item than President Obama. Boxes in Orange are the reverse. Straight Up Comparison Numbers for President Obama come from Whitehouse Budget Summary Tables page 174 (PDF page 6). Numbers for Paul Ryan come from Path to Prosperity Table S-3 on PDF page 64. The category items are identical except Ryan has an extra item for Global War on Terror. To equalize, we added Global War on Terror to Security. Without making any judgment to the contrary, let's assume Ryan and Obama can both "deliver". Here are a few charts depicting the results. You can produce the same charts above via the dropdown boxes and hover functions (minus my anecdotes). Deficit: Obama vs. Paul Ryan Paul Ryan made good headway for three years, then fell flat for another 7. This is no way to shrink the national debt or reduce interest on the national debt as we shall see in a moment. Obama's proposal is abysmal. He made some progress for a few years, then went into reverse. Medicare: Obama vs. Paul Ryan  Amazingly Paul Ryan want to spend more on Medicare than president Obama every year for the next 10 years. To be fair, Ryan takes a big bite out of Medicaid for six years starting in 2016. Security: Obama vs. Paul Ryan  I labeled this as "defense", they both called it "security". Is the "security" label an attempt to make the huge numbers seem more palatable? Regardless, Neither Ryan nor Obama is interested in doing anything about one of the most bloated items on the budget. Moreover, President Obama is the biggest war-monger in history judging from his proposed budget. Democrats should be shocked to see the president propose to spend more than Ryan every year for a decade. I was reasonably confident the president would reduce military spending. He didn't. His scorecard is thus a perfect zero. President Obama has not done a single thing right. It's not easy being perfect, even perfectly wrong. Interest on the National Debt: Obama vs. Paul Ryan The above chart shows the effect of cumulative failures to shrink the deficit. Note that in 2021 president Obama proposes to spend over $900 billion a year on interest on the national debt. This is sickening, not amusing. Paul Ryan would have us spending $687 billion on interest in 2021. His deficit proposal for 2021 is $731 billion. National Debt: Obama vs. Paul Ryan The above chart is where the rubber meets the road. For all the brouhaha surrounding the deficit reduction plans, both are a miserable failure. President Needs a New Head In 2021, under Ryan's proposal, the national debt will soar from $14.973 trillion to $23.105 trillion. Interestingly, that is not that much better than what the president put together as shown above. Ryan needs to reduce more, way more, or raise revenue. There is no other way. I propose a good hard look at military spending. Obama needs a new head. The one he has cannot think at all. His proposal to send the deficit into reverse starting in 2014 and spend close to $1 trillion a year on interest on the national debt is proof enough. Contact Congress Please send your congressional representatives an email or fax and a link to this post and demand they read it. We are on a path to self-destruction even IF we were to pass Ryan's budget. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment