Mish's Global Economic Trend Analysis |

- "The Positive Impact of the Declining Yen Has Yet to be Seen"

- Spanish Firm Markets Mattress With Built-In Safe

- Views from "Out of This World" (a Non-Economic Diversion)

- Record Corporate Insolvencies in Australia

- Fraudulent Guarantees; Fictional Reserve Lending; Comparison of US to Cyprus; What About New Zealand?

| "The Positive Impact of the Declining Yen Has Yet to be Seen" Posted: 20 Mar 2013 11:02 PM PDT Those who thought a declining yen would be a savior to Japan need to reconsider as Japanese February Exports Fall 2.9%. Japan's exports fell more than economists forecast and the nation's trade deficit persisted, underscoring challenges to Prime Minister Shinzo Abe's campaign to revive the world's third-biggest economy."Yet to be Seen" I am laughing out loud at that last sentence. I suggest the "positive impact" will not be seen because there isn't one, at least for the average Japanese citizen. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Spanish Firm Markets Mattress With Built-In Safe Posted: 20 Mar 2013 04:35 PM PDT Putting new meaning to an old phrase (keep your money under the mattress), a Spanish firm touts 'Mattress Savings' the first mattress with built-in safe. "Savings, are better under the mattress". How often have we heard this phrase! The difficult economic situation in recent months and various scandals involving financial institutions have led many to dream about fluffy Spanish euros. Francisco Santos also dreamed, and woke up to make it happen: he created the first mattress with built-in safe.Distrust of banks and governments is widespread and growing (and rightfully so). Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Views from "Out of This World" (a Non-Economic Diversion) Posted: 20 Mar 2013 12:50 PM PDT If you need a break from money supply, jobs, Cyprus, France, Europe in general, or housing (who doesn't) I have a wonderful visual diversion that is literally "out of this world". You can Watch the Aurora Borealis from an International Space Station that captures otherworldly famous lights. The best time to see the aurora borealis here on Earth is during the coldest and darkest nights of the year, so people in the Northern Hemisphere still have a few more nights of ideal viewing. However, here on Earth we only get to see half the show. But luckily for us, the folks orbiting 240 miles above us on the International Space Station have been documenting what we've been missing. The aurora borealis and its southern sister, the aurora australis, are just as breathtaking from above, and the astronauts get a clear view any time of year. These atmospheric light shows are a product of charged particles interacting with the Earth's magnetic sphere and are often tied to solar wind or other sun surface activity. Whichever way you look at it, the phenomenon is surreal. Check out this preternatural light show below.Here are a couple of images. Click on the above link to see the rest.  A southern aurora captured from the International Space Station as it zipped by at 17,239.2 mph. Image by NASA's Marshall Space Flight Center.  This striking aurora ribbon, snapped over the Indian Ocean, was likely caused by a major sun spot event. Image by NASA's Marshall Space Flight Center. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Record Corporate Insolvencies in Australia Posted: 20 Mar 2013 10:09 AM PDT The housing bubble in Australia has popped but the biggest declines are still ahead. Meanwhile other problems have surfaced, as expected in this corner, namely Insolvencies hit record levels in January A total of 628 firms collapsed in January, the highest-ever for what is a traditionally quiet month and a 21.2 per cent increase from the previous year, accounting company Taylor Woodings said in a report released on Wednesday.Optimism is hardly warranted. Australia's fundamentals (a housing-bust economy, a slowdown in mining with falling Chinese demand, overpriced rents, and high labor costs) are simply horrendous. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

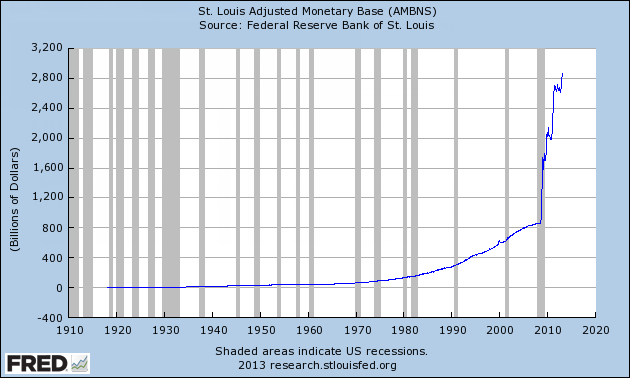

| Posted: 20 Mar 2013 01:24 AM PDT Reader "MB" who lives in New Zealand is concerned about confiscation of deposits. He writes ... Hi MishTheft? A letter to the Reserve Bank of New Zealand states Reserve Bank policy looks like theft. As a super-annuitant who depends on interest from term deposits to top up my pension, I'm horrified to learn that the Reserve Bank will put in place a process by which ordinary bank depositors will, without notification and without their consent, have their savings used to bail out a bank in financial distress.Open Bank Resolution (OBR) Policy To understand what Jill and others are concerned about, let's go straight to the source, the Reserve Bank of New Zealand's Open Bank Resolution (OBR) Policy Why should depositors bail-out banks?The subject of New Zealand is on the verge of going viral. Typically when that happens, the concern is overblown. And that is precisely the case here. Sensible Policy Readers who are unfamiliar with my overall stance on deposit guarantees, especially in light of my posts on Cyprus may be surprised to learn that I commend the Reserve Bank of New Zealand's policy for precisely the reasons it stated: "Deposit insurance is difficult to price and blunts incentives for both financial institutions and depositors to monitor and manage risks properly." Consider a US example. In buildup to the housing bubble crisis, investors flocked to shaky institutions that paid the highest yields on deposits simply because the deposits were guaranteed. The FDIC guarantee enabled hundreds of banks such as now-bankrupt Corus to secure funds used to build condos in Florida and Las Vegas. No one in their right mind would have placed money in Corus and other such banks without those guarantees. In essence, deposit insurance helped fuel the housing bubble. The difference between the policy of New Zealand and what happened in Cyprus is the guarantee itself. Wikipedia has a nice table of 99 countries with deposit insurance. Those without deposit insurance are at least being honest. The problem in Cyprus was the fraudulent deposit guarantee, made by the ECB, and repeated just last month by the president of Cyprus. Fraudulent Guarantees Guarantees in and of themselves are inherently fraudulent by nature. A look at money supply numbers will show why. Base Money  click on any chart for sharper image The Adjusted Monetary Base is the sum of currency (including coin) in circulation outside Federal Reserve Banks and the U.S. Treasury, plus deposits held by depository institutions at Federal Reserve Banks. M1  M1 is narrow money supply. It consists of currency, demand deposits (checking accounts), travelers checks, and other checkable deposits. Travelers checks are actually double-counted but the numbers are so small the error is essentially meaningless. M2  M2 consists of M1 plus savings deposits (which include money market deposit accounts, or MMDAs); (2) small-denomination time deposits (time deposits in amounts of less than $100,000); and (3) balances in retail money market mutual funds (MMMFs). There are better measures of money supply, such as True Money Supply (TMS) and I encourage you to learn about them. I used to maintain charts of TMS (I called it M') but Michael Pollaro does a fantastic job. I used M1 and M2 above because those are the widely reported numbers, and the numbers most economists follow. For the purpose of this discussion, M1, M2, and Base Money supply will suffice. The next chart will help explain why. Total Credit Market  Chart Recap

One Giant Ponzi Scheme Clearly far more money has been lent than exists. How can it possibly be paid back? If it can't be paid back, how good is a guarantee? In 2010 Bernanke proposed ending reserve requirements completely, but long-time Mish readers understand that is the de facto state of affairs already. For example, even the $2.4 trillion in M1 money that is "guaranteed" to be in your checking account and "available on demand" isn't in your checking account at all. It too has been lent. I have talked about this before on numerous occasions but it's worth a review. Please consider my March 23, 2010 post Bernanke Wants to End Bank Reserve Requirements Completely: Does it Matter? What Chaos will Result? There are no reserve requirements on savings accounts right now.Fictional Reserve Lending Should banks (large too-big-to-fail banks) run out of reserves, the Fed is Johnny on the spot, ready and willing to create reserves out of thin air. However, other banks can't count on it. In essence, the system is one giant Ponzi scheme (not just in the US but everywhere), kept afloat by wizards willing to ramp money supply every time big banks get into trouble. An enabling factor to all the bank leverage is Fractional Reserve Lending (which on numerous occasions I have likened to "Fictional Reserve Lending" but is really better thought of as "Negative Reserve Lending". Please see my 2009 post Fictional Reserve Lending And The Myth Of Excess Reserves for further discussion. It's well worth a read. Amusingly, people were arguing at the time such policies would soon cause massive price inflation, but I took the other side of the bet (and still do - for the time being). The Fed, was and still is willing to step in and help any "too big to fail" bank, but numerous small banks went bust in the Great Financial Crisis, and depositors with money over the FDIC limit did on occasion suffer losses. In that regard, the Reserve Bank of New Zealand at least has the courage to tell the truth, with precisely stated reasons: "deposit insurance is difficult to price and blunts incentives for both financial institutions and depositors to monitor and manage risks properly" I am planning a follow-up post on the fraudulent nature of Fractional Reserve Lending, deposit insurance, and related topics, but the five key points for now are as follows: Five Key Points

Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Note: Some ATT users (not a fault of ATT) received timeouts on my "Wine Country Conference" link (see below). If you were one of them, please try again. The problem has been fixed. Wine Country Conference I am hosting an economic conference on April 5 in Sonoma, California. Proceeds go to the Les Turner ALS Foundation (Lou Gehrig's Disease). Please see My Wife Joanne Has Passed Away; Stop and Smell the Lilacs for my association with the disease. To learn about the economic conference with world-class speakers including John Hussman, Michael Pettis, Jim Chanos, John Mauldin, Mike "Mish" Shedlock, Chris Martenson with guest moderator Lauren Lyster and other Special Guests, please visit Wine Country Conference April 5, 2013 |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment