Mish's Global Economic Trend Analysis |

| Posted: 19 Dec 2012 05:07 PM PST "Fiscal Cliff" Talks Turn Sour Yesterday, the sides were so far apart on critical issues that I wondered how a deal could be made in two days. The market saw it otherwise, mainly on hype Obama Offers Concessions Regarding Tax on Wealthy. Today is a different story as "Fiscal cliff" talks turn sour, Obama threatens veto. Talks to avoid a fiscal crisis appeared to stall on Wednesday as President Barack Obama accused Republicans of digging in their heels due to a personal grudge against him, while a top Republican called the president "irrational."Concession Nonsense Reuters writers Matt Spetalnick and Mark Felsenthal and said "Boehner and Obama have each offered substantial concessions that have made a deal look within reach." What "substantial" concessions were those? This is how I stated things yesterday. Significant DifferencesTo be sure, "token" concessions were made, but "substantial" is another matter. White House Said to Tell Business Groups Talks Stall Bloomberg reports White House Said to Tell Business Groups Talks Stall Obama administration officials told leaders of business and financial services groups that negotiations with House Speaker John Boehner have deteriorated in the past 24 hours, a person familiar with the meeting said.Who's Posturing? Obama accused the Republicans of posturing. It's only posturing if the Republicans give in. Perhaps it is Obama who is posturing. Perhaps both sides are posturing. If so, this is another case of the "pot calling the kettle black". Showdown Over "Plan B" Yahoo!Finance reports Boehner Challenges Obama With 'Plan B' Showdown House Speaker John Boehner pressed his backup tax plan Wednesday despite a White House veto threat, saying it will be approved Thursday by the GOP-controlled House.Obama's Fantasyland Statements President Obama is in fantasyland, not only in terms of dollars but also in terms of the negotiation process itself. For starters, on the issue of tax hikes, Boehner would hike taxes on those making $1,000,000 while the president wanted hikes on those making over $400,000. That is a huge difference. The president would not negotiate on the debt ceiling. On the issue of being only "few hundred billion dollars" apart, I rather doubt it. But even if true, Obama would only give in a mere $50 billion on entitlement cuts. Plan "B" is a Sham On the other side of the coin, plan "B" which does not address the revenue side of the equation at all is certainly not fiscally prudent. In fact none of this negotiation is. Unfortunately, there is still time to snatch defeat from the jaws of victory. In this case, victory is letting the fiscal cliff happen. The other alternatives do even less to address out-of-control budget deficits. So, let the fiscal cliff happen. It would be better yet if genuine deficit cuts were added on top of the fiscal cliff, instead of being negotiated away in January. Don't count on that because both parties are more interested in talking about reducing the deficit than actually doing something about it. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific. |

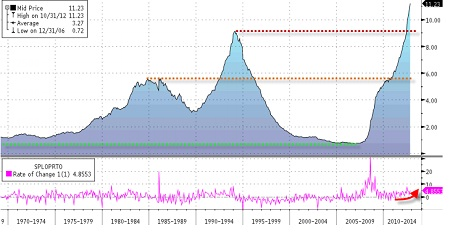

| Posted: 19 Dec 2012 10:31 AM PST Via Google translate El Blog Salmon reports Delinquencies expose the shame of Spanish banks How could it be otherwise, the delinquency has grown back no more and no less than 11.23% during the month of October. The figure represents a new record, exposing the shame of Spanish banks.Also via Google translate from Spanish, the Guru's Blog provides interesting charts and commentary in Banking delinquency rises to 11.23% in October. New record We began to enter the area of record breaking month after month. In October defaults on loans to financial institutions and businesses in October amounted to 11.23% , which marks a new record.The dismal results and conclusions speak for themselves. Does anyone doubt the situation in Spain would be better if Spain had only taken the "Iceland Solution", letting the failed banks fail rather than bailing them out at taxpayer expense? Thanks to El Blog Salmon, Gurus Blog, and Zero Hedge. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Addendum Thanks to Bran for correcting several instances of "million" that should have read "billion" and one instance of "billion" that should have read "trillion". Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific. |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment