Mish's Global Economic Trend Analysis |

- Kyle Bass on the End of the Debt Supercycle and a Coming Massive Devaluation of the Yen; Most Difficult Time to Invest; Belief Bubble

- Nikkei Rises Above 10,000; Yen Drops to Weakest Level Since April 2011

- Boehner Floats Fiscal Cliff "Plan B"; Obama Offers Concessions Regarding Tax on Wealthy

- Normalized Unemployment Rates; Cyclical vs. Secular Forces

| Posted: 18 Dec 2012 11:39 PM PST Late last month, Kyle Bass, managing partner of Hayman Capital, shared his thoughts in a video at the University of Virginia Darden School of Business Investing Conference with Professor Ken Eades. It is a fantastic interview that echoes many of the things I have been saying about Japan for quite some time. Link if video does not play: Conversation with Kyle Bass Interview Snips Ken Eades kicks off the interview welcoming Kyle Bass mentioning that over the past few years his investment thesis has been then same. Eades then asks Bass to recap and review. what follows is Bass' reply. Thematically, the bottom line is the total credit market debt-to-GDP globally is 350 percent. It's 200 trillion dollars worth of debt against global GDP of roughly 62 trillion.Current Account Update Updated current account and trade balances were posted on December 9. Japan's current account balance surprised to the upside, but do not expect it to last. Nasdaq reports Japan Current Account Stronger Than Expected.

TOKYO--Japan's current account surplus fell in October from a year earlier, as the nation's trade deficit continued to expand, while separate revised gross domestic product figures showed that the economy may have already entered a recession.Balance of Trade and Current Account Please consider the trend in Japan's Balance of Trade Japan recorded a trade deficit of 548.90 Billion JPY in October of 2012. Historically, from 1979 until 2012, Japan Balance of Trade averaged 635.3 Billion JPY reaching an all time high of 1608.7 Billion JPY in September of 2007 and a record low of -1476.9 Billion JPY in January of 2012.Balance of Trade Since 2009  click on chart for sharper image Starting in 2011, Japan's balance of trade has been consistently negative. Please consider the trend in Japan's current account. Japan recorded a Current Account surplus of 376.90 Billion JPY in October of 2012. Current Account in Japan is reported by the Ministry of Finance Japan. Historically, from 1985 until 2012, Japan Current Account averaged 1106.53 Billion JPY reaching an all time high of 3287.90 Billion JPY in March of 2007 and a record low of -437.30 Billion JPY in January of 2012. Current Account is the sum of the balance of trade (exports minus imports of goods and services), net factor income (such as interest and dividends) and net transfer payments (such as foreign aid).Current Account Since 2009  The trend in Japan's current account has been in serious decline starting 2011. Japan will be in serious trouble as soon as its current account stays negative. That has not happened yet, but it will. As soon as it does, Japan's debt-bomb goes off. For more on the Yen please consider Spotlight on Japan: Return of 'Abenomics', More Militarism, Tougher China Line; Outlook for Yen and Nikkei For more on the conflict with China regarding disputed islands, please see China Skips IMF Meeting In Japan; Taiwan Claims Islands Too; What's the Dispute Really About? Most Difficult Time to Invest I wish to conclude with the statement by Kyle Bass "As Dick Mayo [Chairman, Mayo Capital and Founding Partner of GMO] said today, it's actually the most difficult time in the world to invest in his lifetime." I endorse that statement 100%. Moreover, I would like to add that many now find investment decisions relatively easy. They look at monetary easing by the Fed, by the ECB, by China, etc., as a perpetual green light. Clearly Kyle Bass does not see it that way, nor do I, nor does John Hussman. Indeed, I believe the only one's who find investment decisions easy are those who do not understand the risks. Belief Bubble As I have pointed out on many occasions, if the Fed could have prevented a collapse in 2008, it would have. If Japan's central bank had an easy cure for deflation, it would have found it long ago. Instead Japan has a massive amount of debt, with nowhere to hide. If the ECB had an easy solution to the crisis in Greece, Spain, and Italy, there would not be endless meetings followed by endless bickering. Yet, for whatever reason, there is a bubble in the belief that central banks are in control. Problem is Debt, With No Easy Cure The problem is debt. As Bass pointed out "the total credit market debt-to-GDP globally is 350 percent. It's 200 trillion dollars worth of debt against global GDP of roughly 62 trillion." The 70-year debt super-cycle is coming to and end. It could have happened last year, or the year before, but it didn't. It may or may not happen in 2013. Those fully loaded in equities are either ignorant of these facts or they do not care. Those of us who are aware, but also aware the end cannot be precisely timed are the ones who look overly cautious. We are the ones who think "this is a difficult time to invest". Prudent to be Patient I am comfortable in my position that better times are ahead for those willing to be patient, even if I cannot precisely say when that will be. In the meantime, I am willing to sit with a position in gold, cash, and various hedges until better opportunities present themselves. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com "Wine Country" Economic Conference Hosted By Mish Click on Image to Learn More  Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

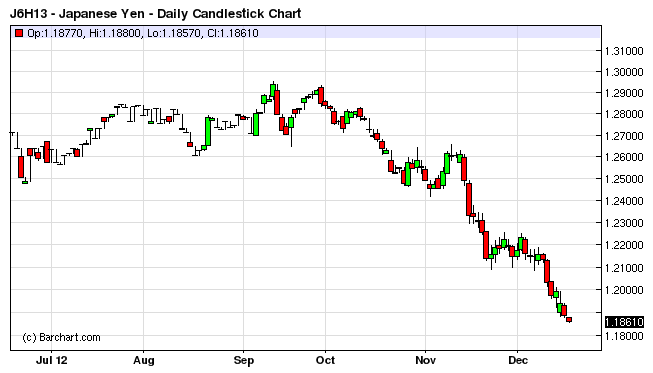

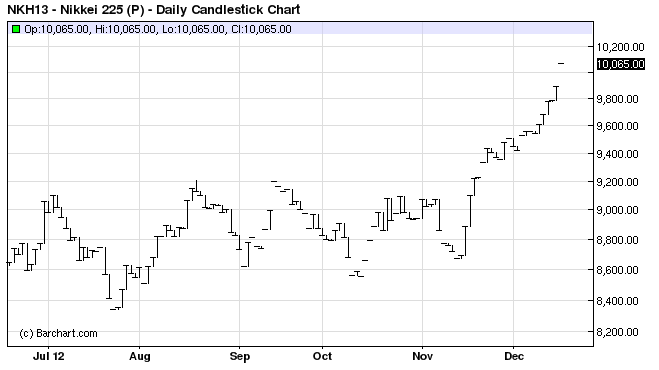

| Nikkei Rises Above 10,000; Yen Drops to Weakest Level Since April 2011 Posted: 18 Dec 2012 05:05 PM PST In a pair of related ideas, the Yen is sinking and the Japanese stock market is on a tear. Today the Nikkei crossed the 10,000 mark once again. Yen Futures Daily Chart  click on chart for sharper image Nikkei Futures Daily Chart  Yen Drops to Weakest Level Since April 2011 Bloomberg reports Yen Falls to August 2011 Low Versus Euro on Stimulus Bets. The yen fell to its lowest level since August last year against the euro on prospects that the Bank of Japan will expand stimulus at the meeting that starts today, its first after the nation's general election.In the race for currency debasement, Japan will soon pass the Fed. Repeating what I said yesterday in Spotlight on Japan Since Mid-November the Nikkei has been on an upward tear. The Yen has been in decline since the start of October. Both trends have favorable fundamentals, and both are worth watching. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Boehner Floats Fiscal Cliff "Plan B"; Obama Offers Concessions Regarding Tax on Wealthy Posted: 18 Dec 2012 09:40 AM PST Boehner Floats Fiscal Cliff "Plan B" Both house speaker John Boehner and president Obama have given ground in the "fiscal cliff" drama. The sides are still far apart but concessions now are steady. The fact there is ongoing movement makes a deal possible. Will we get there? Can Boehner get enough in return on entitlement cutbacks? On that score the president has barely budged, but the stock market sure seems to think a deal will be reached. Please consider Boehner floats 'Plan B' as cliff deadline nears. House Speaker John Boehner on Tuesday floated a back-up plan to raise taxes on incomes of $1 million and above, even as Republicans and the White House were moving closer to a deal to avert the fiscal cliff.The only difference between Plan A and Plan B that I can tell is the offer of tax hikes on those making over $1,000,000. Wasn't that hashed out over a week ago? Concessions From Both Sides MarketWatch notes concessions, Where Obama and Boehner Have Backed Down Taxes: Monday night, Obama dropped his long-held insistence that rates rise for incomes of $250,000 and above. The new target: allowing Bush-era rates to expire for incomes of more than $400,000. The speaker is willing to accept higher rates on $1 million incomes and above. Chances are that neither side is done moving toward the other. Could $500,000 be the sweet spot?Significant Differences

The gaps that still remain are huge. Nonetheless, the stock market acts as if a deal is at hand. Should there be a deal, a sell-the-news event seems likely. Assuming there is a deal (and I am still not entirely convinced there will be one), the only market-favorable fundamental is the Fed, and at some point that will cease to work. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

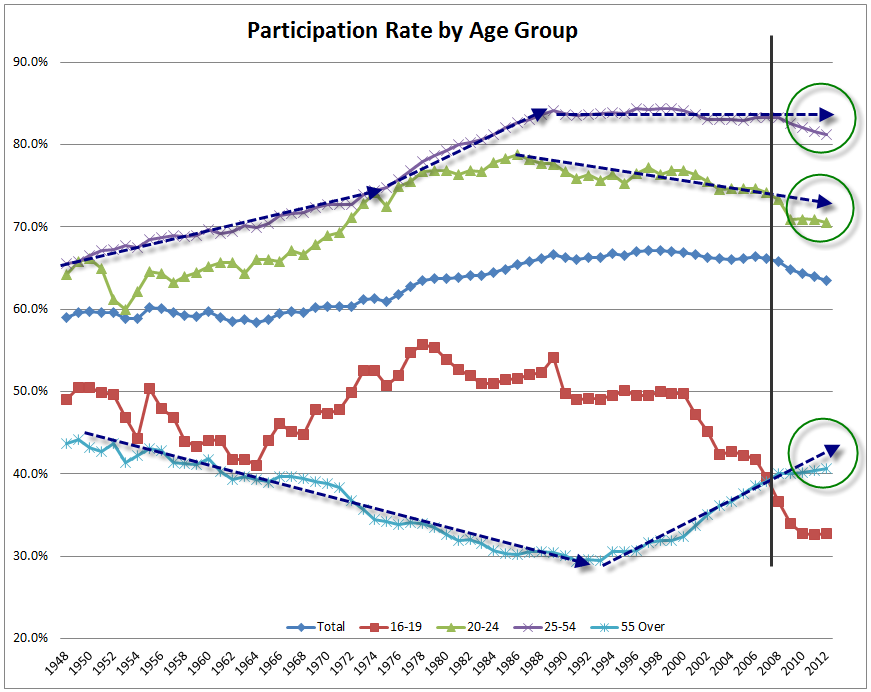

| Normalized Unemployment Rates; Cyclical vs. Secular Forces Posted: 17 Dec 2012 11:58 PM PST Many have heard of normalized P/E ratios based on 10-year earnings averages and the concept of reversion to the mean. To the best of my knowledge no one has attempted to normalize unemployment rates based on demographic trends, although some have attempted unemployment normalizations based on changing definitions of the meaning of unemployment. The following participation rate chart defines the problem. Participation Rate by Age Group  click on any chart for sharper image The above chart first appeared in my post Boomer Demographics and the Unemployment Rate. It is from a series by reader Tim Wallace. (click on link for rest of the series). I added trendlines, a vertical black line, and circles to the chart. Definitions and Notes

Secular Forces The trends in purple (age 25-54), and green (age 20-24) up until 1988-1990 or so reflect the entry of women into the workforce. Starting around 1988 there were abrupt changes in the participation rates of age groups 25-54, 20-24, and 55+. The shift in participation rate of 55+ was especially abrupt. Those shifts reflect baby boomer dynamics. Structural vs. Cyclical Forces A second major shift (marked by the black vertical line), was far more sudden, occurring exactly at the onset of the 2007 recession. The question at hand is whether or not the trendlines at the onset of the recession are still valid. If so there is a pronounced impact on expected participation rates, and therefore unemployment rates (by implication). It's easy to confuse what's cyclical vs. what's secular because the direction of the 55+ trend did not change in 2007, only the slope changed. The direction did change for age group 55+ in or around 1992. Participation Rate Discussion I started work on these ideas much earlier this month with preceding posts as follows:

For example, on December 13, Andrew Wilkinson, Chief Economic Strategist for Miller Tabak & Co. asked the question How Realistic is the FOMC's Unemployment Forecast? Wilkinson notes that if the participation rate rises a mere .5 percentage points employers would need to add 181,000 to prompt the Fed to take away the punchbowl by the end of 2015. If the participation rate were to rise to 65.8 (the average reading since 2000), it would take a whopping 284,000 jobs per month. See my December 12 article for charts on the same lines of thought. A table I posted in 2009 will show why 180,000+ jobs per month is not in the cards. Monthly Job Growth 1999-2009  Chart courtesy of BLS. Annotations by me, numbers are in thousands. The areas in deep blue mark recessions.

Neither the housing boom, nor the commercial real estate boom is coming back. Nor is there going to be another internet revolution. If anything, outsourcing of jobs to Asia is likely to remain intense. Finally, consider all the financial engineering jobs, banking jobs etc, that are not coming back. Lost Bet Returning to the present, Wilkinson states "As you can see there are plenty of moving pieces in projecting advances for the labor market. In plain and simple terms arriving at an unchanged unemployment reading through 2013 might require payroll gains of anywhere between 110,000 and 500,000 depending on how many people you want to involve in the labor market." Yes, I can clearly see that, noting that I lost a bet on it. Although I was certain the participation rate would drop, I never envisioned it would drop this far this fast (dragging the unemployment rate down with it). For details, please see my October 7, 2012 post Lost Bet. Where to From Here? Wilkinson concludes with "In order for the desired unemployment rate to meet the falling projection laid down by the Fed, payroll growth is going to have to start picking up from its present pace. If it does not, the Fed is likely to be highlighting on an ongoing basis the lack of quality in the improving fortunes of the labor market." Assuming "lack of quality" is the same as "falling participation rate", I am in agreement with Wilkinson. Indeed, I will go one step further, suggesting the Fed is likely to miss badly even if payroll growth picks up (which I do not think will happen). Will the Jobless Rate Drop Take a Break? While pondering my thoughts regarding a bad miss by the Bernanke Fed on unemployment projections, please consider an economic research article by the San Francisco Fed, Will the Jobless Rate Drop Take a Break? Looking at secular trends, participation grew rapidly from the mid-1960s through the 1990s as women entered the labor force in higher numbers. As women's participation stabilized and baby boomers began to retire, labor force participation leveled off and in the 2000s began to decline. Young people spent more time in school during this period, further reducing participation rates. On the cyclical side, participation has tended to fall in recessions as workers withdrew from the labor force. This pattern was particularly pronounced during the recent financial crisis.Wilkinson, the authors of the San Francisco Fed article above, and I are all having similar thoughts and concerns regarding the forces in play. Cyclical Forces at Play Please consider this chart from my December 7 article Startling Look at Job Demographics by Age.  Note that age groups 16-19 and 20-24 do not register at all in terms of importance. We can guess whether or not the trend towards more school will continue or even reverse (increased schooling is what is driving the participation rate in those age groups), but what matters is the trend in age groups 55+ and even more so 25-54. For convenience here is the chart I posted at the top of this now lengthy article. Of the three green circles, the ones at the top and bottom are the ones of relevance. Age 55 and Over Discussion The current (since about 1992) trend in age group 55+ will not continue forever. At some point, perhaps age 75 or so, people will stop working whether they want to or not, simply because they will be physically unable. At what age that will happen is debatable, but it will happen at some point even though overall longevity is increasing. Thus, some of that trend change since 2007 may be structural, but the rest is cyclical. Based on the abrupt change at the start of the recession, I suspect most of the trend change since 2007 is indeed cyclical, even though some flattening of the trend should occur later based on physical ability as noted above. The important point is a return to the trendline will increase the participation rate (even if at a flattening rate over time). Age 25-54 Discussion Unlike demographics for students (and the trend for more college education), I see no reason other than an extremely poor job market for the abrupt change in the 25-54 participation rate starting in 2007. Thus, in this demographic, nearly all of the drop in participation rate is cyclical. And that drop is extremely important as the following table shows. Population, Labor Force, Unemployment Rate, Participation Rate (Age Group 25-54)

The average participation rate for 2000-2007 is 83.3. Let's normalize the labor force and unemployment rate for the average participation rate and check out the results. Normalized Labor Force, Unemployment Rate(Age Group 25-54)

Reported vs. Normalized Numbers

At present, the labor force is realistically understated by 2,521,000 minimum and the the economy is currently short 2,361,000 jobs, also minimum. Making adjustments for this demographic group alone, the overall unemployment rate would be 9.2% instead of the reported 7.7%. Moreover, and as noted above, I think reversion to the trendine in the second most important demographic (age 55+) is coming as well, except the 55+ trendline will flatten by natural causes (demographic as opposed to cyclical) over time. Factor in a slight rise in participation rate for the 55+ demographic and the unemployment rate would be close to 10. How Fast Can We Catch Up?

The key word above is "additional" and it ignores the possibility of a move back towards the trendline for age group 55 and over. Conclusion This "normalization" exercise (reversion to the mean demographic-adjusted trendline) shows how small upward changes in the participation rate in age group 25-54 alone will make it near-impossible for Bernanke to hit the Fed's unemployment target by 2015. The above projections do not even factor in the possibility (I think near-certainty) of a recession in the meantime. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com "Wine Country" Economic Conference Hosted By Mish Click on Image to Learn More Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific. |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment