Mish's Global Economic Trend Analysis |

- Questions of the Day: What if the BLS is Wrong About its Labor Force and Participation Rate Projections? How Would it Affect the Unemployment Rate?

- Exit Strategy? What Exit Strategy?

- Mark Carney, Incoming Governor of the Bank of England, Dives Straight Into Monetarist Loony Bin

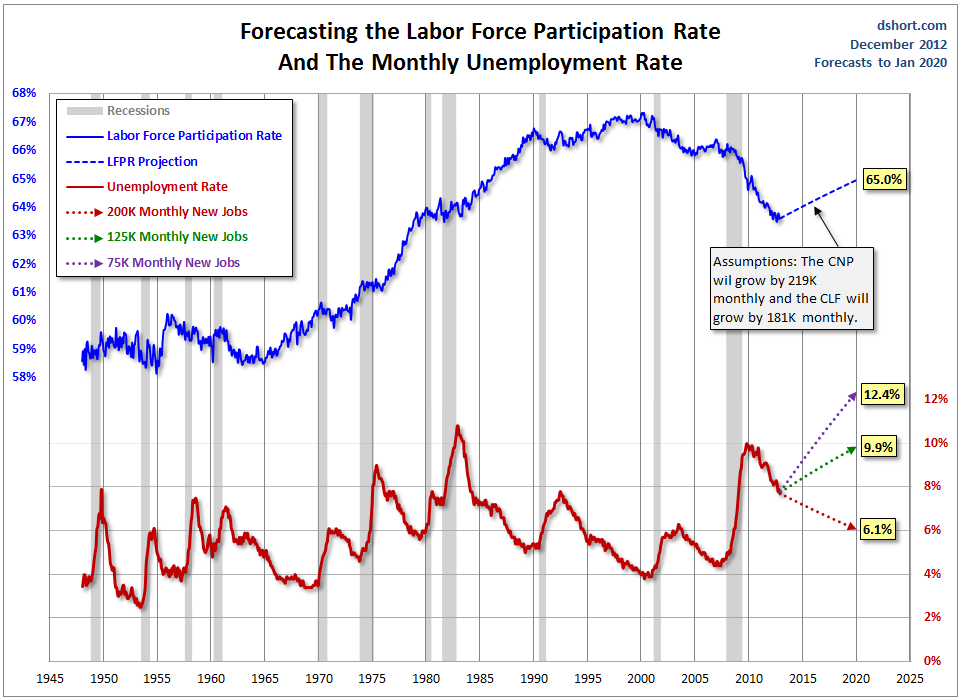

| Posted: 12 Dec 2012 02:08 PM PST On Monday, my "question of the day" was What will the unemployment rate look like for the rest of the decade? Click on the above link to see an interactive map that lets you select the rate of job growth up to January of 2020. The base assumptions for the interactive map regarding the noninstitutional population, the labor force, and the participation rate came from revised BLS projections by Mitra Toossi in January 2012: Labor force projections to 2020: a more slowly growing workforce Note that the accuracy of the unemployment forecast depends on the accuracy of the assumptions. What if the BLS is Wrong? Today we concern ourselves with the question "What if the BLS assumptions are wrong?" We do have to start somewhere, and the assumption for the charts below is that the BLS is right about the size of the age 16 and older noninstitutional population, but wrong regarding the participation rate and the size of the labor force. Certainly boomer dynamics are now understood well enough that the age 16 and older noninstitutional population projections are likely to be quite accurate. How fast baby boomers retire or drop out of the labor force is certainly much harder to predict. Definitions and Notes

As you can see, projecting the population accurately and projecting the labor force accurately are two different things. Starting with the assumption that Toossi is correct regarding the noninstitutionalized civilian population, I asked Doug Short at Advisor Perspectives if he would plot unemployment rates at various rates of job growth with a participation rate of 62.5 (the base Toossi model), as well as participation rates of 60.0 and 65.0. The charts below show startling differences as to what happens if the participation rate changes in those small increments. Model Notes

Unemployment Assuming Participation Rate of 62.5  click on any chart for sharper image At 125,000 jobs a month (and that is a very optimistic forecast in my opinion), the unemployment rate would slowly sink to 6.3% by 2020. Unemployment Assuming Participation Rate of 65.0  The current participation rate is 63.6. A mere rise in the participation rate to 65 would require 200,000 jobs every month non-stop until 2020 to get the unemployment rate to 6.1%. Needless to say, 200,000 jobs a month is not going to happen. At 125,000 jobs a month, every month, the unemployment rate would rise to 9.9%. Is such a scenario all that unlikely? Unemployment Assuming Participation Rate of 60.0  Should the participation rate drop to 60, it would only take 50,000 jobs a month to get the unemployment rate down to 6.5%. How likely is that? The participation rate was 60.2 in December of 1955. The participation rate dramatically rose starting in the mid-60's as women entered the work force en masse. Given that people are living and working longer (the latter because they did not sufficiently save for retirement), will the participation rate drop to 60 again? Consider what I said on May 1, 2008 in Demographics Of Jobless Claims Ironically, older part-time workers remaining in or reentering the labor force will be cheaper to hire in many cases than younger workers. The reason is Boomers 65 and older will be covered by Medicare (as long as it lasts) and will not require as many benefits as will younger workers, especially those with families. In effect, Boomers will be competing with their children and grandchildren for jobs that in many cases do not pay living wages. Theoretically the participation rate could drop that low but the economy will likely be horrific if it does. Moreover, should the rate fall that low, it will be at the expense of a massive rise in those on food stamps and other social safety net programs. Table of Projected Unemployment Rates  Note the peculiarity (and mathematical impossibility) of negative unemployment rates at high levels of job creation coupled with a participation rate of 60. All things considered, Toossi's revised model showing the participation rate slowly dropping to 62.5 seems reasonable, but a rise to 65 is not out of the question. At a participation rate of 62.5 it will take about 100,000 jobs a month through 2020 just to hold the unemployment rate steady. For a look ahead to 2013, please see Small Business Owners' Hiring Intent Plunges to 2008 Lows; Don't Blame Sandy or Fiscal Cliff. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com "Wine Country" Economic Conference Hosted By Mish Click on Image to Learn More  Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific. |

| Exit Strategy? What Exit Strategy? Posted: 12 Dec 2012 10:12 AM PST Today the Federal Reserve issued this Policy Statement Regarding Purchases of Treasury Securities and Agency Mortgage-Backed Securities. On December 12, 2012, the Federal Open Market Committee (FOMC) directed the Open Market Trading Desk (the Desk) at the Federal Reserve Bank of New York to purchase longer-term Treasury securities after the maturity extension program is completed at the end of December 2012, initially at a pace of about $45 billion per month. The FOMC also directed the Desk to continue purchasing additional agency mortgage-backed securities (MBS) at a pace of about $40 billion per month. These actions should maintain downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative.Recall when the Fed pretended it was working on an exit strategy to reduce its balance sheet at the appropriate time? It was a lie then and it's an even bigger, more apparent lie now (which is why you no longer hear Bernanke mentioning it) . The simple fact of the matter is that every Fed asset purchase makes it more difficult to exit. When interest rates do start to tick up (which could be a while based on Fed statements), interest on the national debt would soar if the Fed unloaded treasuries. Likewise, mortgage rates would soar if the Fed unloaded agencies at a time interest rates were creeping up. There never was an exit strategy and there never will be one. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific. |

| Mark Carney, Incoming Governor of the Bank of England, Dives Straight Into Monetarist Loony Bin Posted: 12 Dec 2012 01:56 AM PST Mark Carney, Bank of Canada governor and surprise pick to replace Mervyn King as incoming governor of the Bank of England, dove straight into the monetarist looney bin today with policy proposals. The Telegraph reports Mark Carney hints at need for radical action to boost ailing economies Mr Carney, the current Bank of Canada governor who takes over from Sir Mervyn King next June, said central bankers should consider committing to low interest rates until inflation and unemployment met "precise numerical thresholds", or even changing "the policy framework itself" to stimulate a desperately weak economy.Economic Lunacy Only arrogant fools think they can overpower markets without causing even more severe problems down the road. If fiscal and monetary stimulus worked, Japan would be a glowing success today instead of having a debt to GDP ratio approaching 250%. The US housing bubble is another case in point. By holding interest rates too low, too long Fed chairman Alan Greenspan bailed out banks then deep in hock with nonperforming loans to South America and dotcom companies going bust. The end result was a housing bubble far bigger than the dotcom tech bubble that preceded it. Indeed, Fed policy has spawned bubbles of ever increasing amplitude over time. The only beneficiaries of those bubbles have been the banks and the already wealthy. Carney the "Talented" Speaker Carney is a talented speaker, able to speak out of both sides of his mouth at once, each saying opposite things. In light of Carney's "radical action" statements, please consider Bank of Canada warns of low-rate risk. The Bank of Canada says low-interest policies that it and other central banks have put in place are adding another layer of risk to the already stressed global financial system.Also consider these December 11, snips from the Globe and Mail. "Our current guidance indicates that some policy action may be necessary, encouraging a degree of prudence in household borrowing," Mr. Carney said in his speech, echoing the warnings of the Bank of Canada's last policy statements.Nothing like warning about debt and low interest rates, while pledging to keep interest rates low until artificial central planning targets are met. Carney stated the central bank "would clearly say we are doing so" if it chose to act on consumer debt. Yep, I don't doubt that. Indeed, I suggest that Carney would notify banks in advance of any major policy moves. Goldman Sachs Background Let's back up a bit and look at Carney's background as listed on Wikipedia. Carney spent thirteen years with Goldman Sachs in its London, Tokyo, New York and Toronto offices. His progressively more senior positions included co-head of sovereign risk; executive director, emerging debt capital markets; and managing director, investment banking. He worked on South Africa's post-apartheid venture into international bond markets, and was involved in Goldman's work with the 1998 Russian financial crisis.From a Goldman Sachs and JP Morgan standpoint, Carney is the perfect candidate to head the Bank of England. Who could possibly be better than a currency crank promising clear signals, with a background of advising Russia while betting against it? As a practical matter, however, should Carney actually implement his "radical action" policies, I suggest the UK would quickly be in ruins. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific. |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment