Mish's Global Economic Trend Analysis |

- Graphical Look at Trends in Weekly Unemployment Claims

- Philly Fed Rises But Details Very Weak; Future Expectations Plunge

- Brookings Institute On Looming Fiscal Cliff: Little Room for Optimism

- China’s Economy Slows, Power Output Falls to Four-Month Low but Premier Upbeat on Economy; Enormous Headwinds

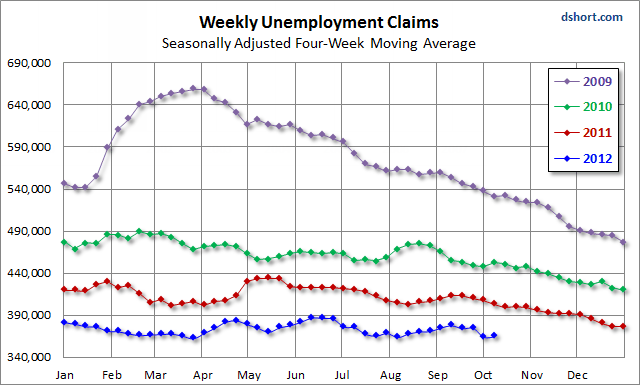

| Graphical Look at Trends in Weekly Unemployment Claims Posted: 18 Oct 2012 08:34 PM PDT As expected, weekly unemployment claims bounced sharply higher this week, up a whopping 46,000 from last week's revised figure of 342,000. Last week, recall that the Labor Department reported a four-year low of 339,000 first-time claims. It was not a real number. As I noted a week ago in So Much For Today's Surprising "Drop" In Weekly Jobless Claims; California Forgot to Report 30,000 Claims ... I still think Friday's jobs report will be revised away, but I am positive today's "surprising" report will be (for the simple reason California forgot to report 30,000 claims).Economists were thus expecting about 370,000 claims this week, but amusingly claims shot all the way back to 388,000. So much for conspiracy theories regarding unemployment claim numbers. To better understand real trends we need to look at the 4-week moving averages of claims to help smooth out things like weather-related incidents (and California ineptitude). 4-Week Moving Average Trends 2009-2012  To put trends into a visual perspective, I asked Doug Short at Advisor Perspective for a year-by-year breakout, as shown above. Note that weekly claims headed sharply lower in April of 2009 two months prior to the official end of the recession. There was a slow but relatively steady improvement in 2010, and a choppier improvement in 2011. In 2012, there is has been no improvement since mid-February, and minimal improvement since the start of the year. Weekly Claims 2005-2008  The four-year moving average of claims was 331,000 when the recession started. It is 365,500 today. At no point has the 4-week average of claims dropped below 360,000 since early 2008. Where To From Here? If you are expecting a big jump in weekly claims prior to the recession, I doubt you get it. Indeed, if you stake the claim as I have, that the recession has already started, you already didn't get it. Moreover, corporations are running pretty lean employee-wise and housing starts are bottoming (if not already bottomed), so one should not expect to see a similar spike in claims as we saw in mid-2008 and 2009. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

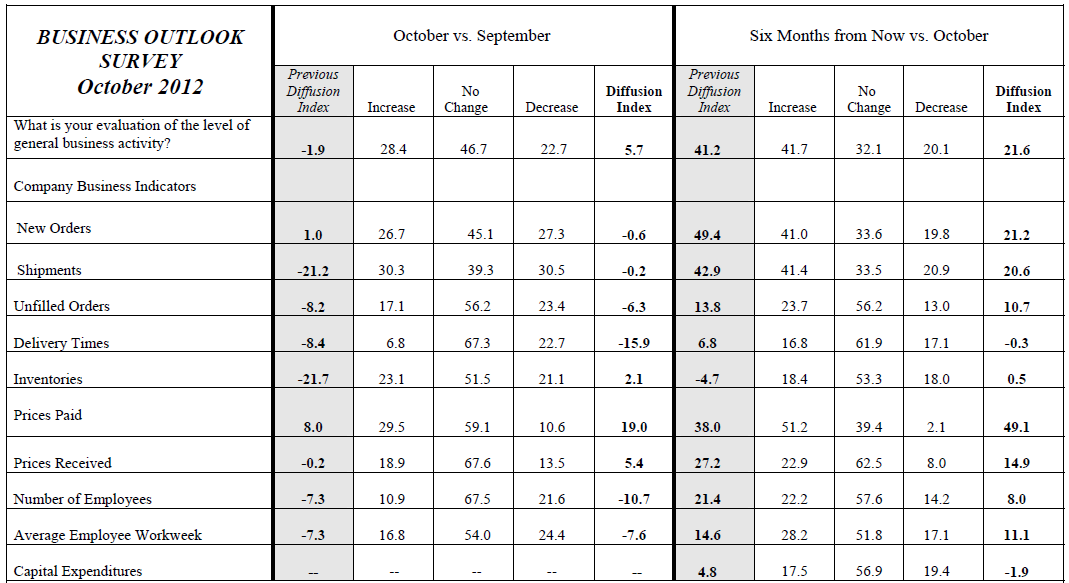

| Philly Fed Rises But Details Very Weak; Future Expectations Plunge Posted: 18 Oct 2012 12:38 PM PDT Inquiring minds digging into the latest Philly Fed Manufacturing Report will quickly discover the rise from last month is really a mirage.  click on chart for sharper image Index and Details The previous overall diffusion index rose from -1.9 to +5.7. However ...

6-Month Expectations I recently said expectations looking six month out were wildly optimistic and they were (and still are).

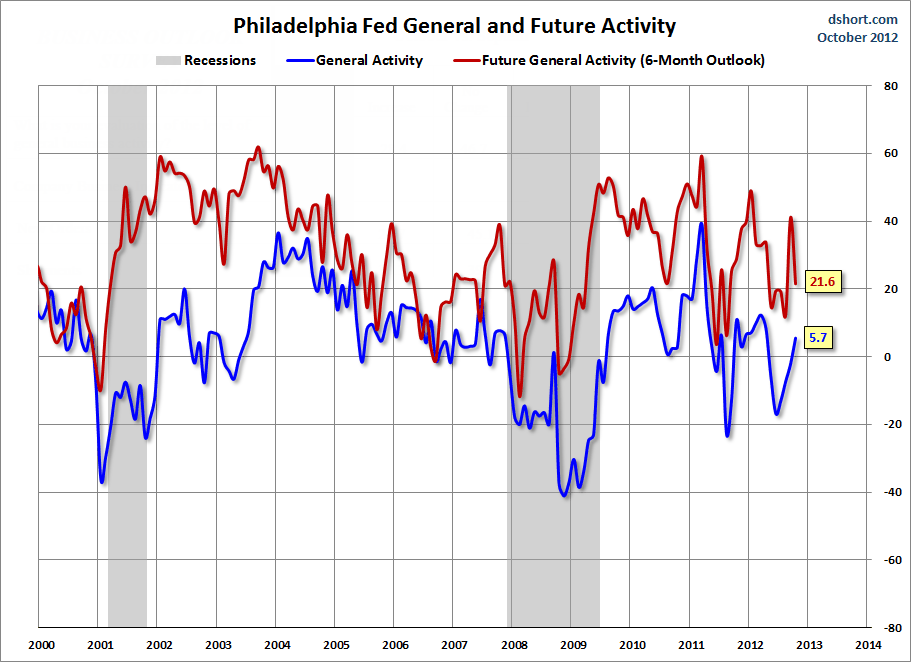

Doug Short at Advisor Perspectives has an interesting series of Philly Fed Charts. For example, here is a graph of current vs future expectations.  click on chart for sharper image Doug writes "The average absolute monthly change across this data series is 7.9, which suggests that the 7.6 point change from last month is not highly significant .... The latest Future reading has shown a substantial decline of 19.6 points following last month's 28.7 point surge." This was a very weak report but billed as "stronger than expected". Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Brookings Institute On Looming Fiscal Cliff: Little Room for Optimism Posted: 18 Oct 2012 09:46 AM PDT Brookings Institute Senior Fellow Ron Haskins discusses the Looming Fiscal Cliff in the following video. About 30 seconds in, Haskins' stated "the fiscal cliff is kind of the opposite of Keynesian economics". I was thinking here we go again, another person thinks we cannot do anything about this "now". Having played it entirely, it is clear Haskins is not supportive of the Keynesian view, rather, he is disgusted as to why we are where we are, blaming Congress, the president, an partisan politics. He failed to address the role of the Fed or fractional reserve lending, but he is against can-kicking exercises. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Posted: 18 Oct 2012 01:25 AM PDT A rally in Asia is underway this morning as Wen Jiabao, China's premier is upbeat on China's economy Wen Jiabao, China's premier, has given his most optimistic assessment of the Chinese economy since the start of the year, saying that it had stabilised and that the government's target of 7.5 per cent annual growth was well within reach.Power Output Drops As Growth Slows 7th Quarter Bloomberg reported China Power Output Falls to Four-Month Low Amid Slowing Economy China's power output in September fell to the lowest level in four months as economic growth slowed for a seventh quarter.Enormous Headwinds China has massive property bubbles, an infrastructure building bubble, and is overly committed on exports with the EU in a massive recession and the US in recession as well (at least by my estimation, slowing by other estimates). Moreover, numerous shadow-banking and ponzi loan schemes have collapsed this year. Worse yet, the bubble-busting collapse of shadow-banking schemes is likely just getting started. In response, China has announced various infrastructure stimulus measures, but all that does is prolong the inevitable collapse in the unsustainable infrastructure-building model. Infrastructure building in China is already at the point of malinvestment. The projects will never be economically viable. China's move to a consumption model away from exports and fixed investment is going to be painful. The collapse of shadow banking and the breakup of state-owned-enterprises will be key issues in the coming decade. Power Struggle of a Different Order Yet, China can stimulate for a while just as the US can and did (increasing headaches down the road), but do not expect much more with a major regime change coming up. Please consider the New York Times article In China, a Power Struggle of a Different Order. As the Communist Party in China prepares for a once-in-a-decade leadership transition next month, it is also planning to take a giant step — to break up the monopolies enjoyed by its gargantuan state-owned enterprises.The NYT article is well worth a read in entirety. It discusses many of the issues and battles raised long ago by Michael Pettis at China Financial Markets. Huge Battle Brewing Pettis has been on top of the SOE issue for quite a long time. Here are a few more links worth reviewing regarding the battle looming over the SOE breakup as well as future expected growth of China.

Whether or not China meets its full-year (revised lower) target is essentially irrelevant. What happens over the next few years is what matters. And on that score I think China bulls will be shocked how anemic Chinese growth will be. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com "Wine Country" Economic Conference Hosted By Mish Click on Image to Learn More  Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment