Mish's Global Economic Trend Analysis |

- Swedish Finance Minister Expects Greece to Exit Euro Within Six Months; Comments From Saxo Bank

- Recovery, Monetary Policy, and Demographics: NY Fed vs. Mish Analysis

- Charting Errors in BLS Participation Rate Projections

| Swedish Finance Minister Expects Greece to Exit Euro Within Six Months; Comments From Saxo Bank Posted: 15 Oct 2012 06:00 PM PDT Anders Borg, Sweden's finance minister, has warned it is 'probable' that Greece will leave the common currency. As European Union leaders prepare for a summit next week devoted to saving the euro, Swedish Finance Minister Anders Borg said Greece may quit the common currency within the next six months.Comments From Saxo Bank Steen Jakobsen, chief economist for Saxo Bank in Denmark pinged me with with an email about Borg this morning ... If Anders Borg is saying this – people needs to listen – he is by far the most pragmatic FM in the world, and very unemotional. This is major sign of the upcoming trouble for Greece and reconciling a deal where Germany and Austerity North gets something, and Club Med lead by Monti and Hollande continues to be non-accountable.Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||||||||||||||

| Recovery, Monetary Policy, and Demographics: NY Fed vs. Mish Analysis Posted: 15 Oct 2012 11:13 AM PDT Fresh on the heels of my 3:38 AM post Charting Errors in BLS Participation Rate Projections came an interesting speech by William Dudley, president of the Federal Reserve Bank of New York. Please consider these snips from Dudley's speech today The Recovery and Monetary Policy. My remarks will focus on the economic outlook. I do this with some trepidation, of course. In the private sector there are two adages about forecasting that underscore the need to be humble in this endeavor: First, forecast often. Second, specify a level or a time horizon, but never specify both, together.NY Fed vs. Mish Analysis I have talked about all of the reasons cited by Dudley on this blog, numerous times, many before the financial crisis even hit. Yet, we all have our misses, for me it was the stock market, not the economy that is in question. The financial recovery was far greater that I imagined in the face of what I thought was rather easy-to-see reasons why the real economy would not respond well to unprecedented stimulus globally, not just in the US. Others have had misses as well. The group that was furthest off in projections were the staunch inflationists and hyperinflationists. Once again I though inflation was an easy call. Credit, except for student loans and other government-sector credit has gone nowhere. As measured by credit (subtracting government sector loans), inflation is barely positive. As measured by prices, I happen to think inflation is a bit higher that the Fed states, especially when it comes to food and energy. Regardless, inflation is nowhere near out of control and hyperinflation calls look rather silly. By the way, there is much more to the above article including four other exhibits and corresponding discussion. Inquiring minds may wish to take a look. Reflections on Stimulus First, please note that stimulus measures are actually way larger now than anyone talks about. For a discussion please see US Runs 4th Straight $1 Trillion-Plus Budget Gap; More Stimulus? You Already Got It; Welcome to Slow Growth. Simply put, trillion dollar deficits are nothing but monstrous (and misguided) Keynesian stimulus proposals. All the more reason for the Fed, to be puzzled over the weak recovery. I have written about this numerous times before, but here are a few of them.

Where To From Here? The Fed has not helped the real economy much, even if it has helped financial assets. The thing is, recovery of financial assets has minimal correlation to consumer spending. In contrast, rising home prices do. People make all kinds of home improvements if they think they will "get their money back". However, consumers have rightfully thrown in the towel on such thinking. Businesses did not hire in response to stimulus as I expected and I still do not think they will. Why should they? The problem is lack of customers, not ability to get loans. Moreover, Obamacare is a real drag on business hiring. For a discussion, please see Is Obamacare Responsible for the Surge in Part-Time Jobs? What About Obama's Defense Layoff Suspensions? I wrote about Obamacare about a week ago and received numerous responses from people that their businesses are indeed acting the way I said they are. I will have a follow-up shortly. In general, businesses are running pretty lean. Should consumer spending pick up in a big way, perhaps there will be a spurt in hiring. However, tax hikes starting in 2013 will be a drag on spending. Businesses, already lean, may have little room to fire. The choice then would be to fire workers (who would then have no money to spend, or keep the workers and take a big profit hit). Alternatively, there are half-way measures of reducing hours across the board. Many think the US is heading for recession. I think the US is in one already, as of June. Regardless, corporate profits will have only one way to go if the recession strengthens in a major way. Can the stock market stay elevated in the face of priced-for-perfection results, demographics, and structural forces at play? I do not think so, but that is what I have thought for the last year and a half. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com "Wine Country" Economic Conference Hosted By Mish Click on Image to Learn More  Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||||||||||||||

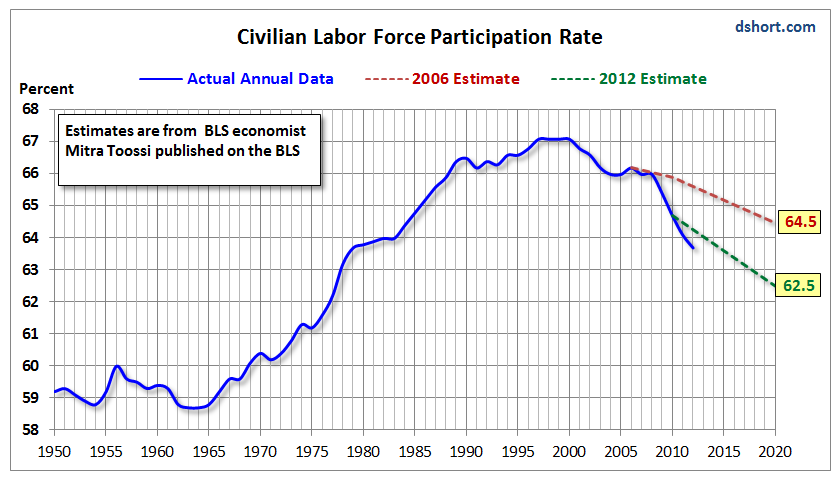

| Charting Errors in BLS Participation Rate Projections Posted: 15 Oct 2012 01:38 AM PDT The following graph plots labor force participation rates by BLS economist Mitra Toossi in November 2006 with new projections for the participation rate as of January 2012:  click on chart for sharper image Chart Data Mitra Toossi in November 2006: A new look at long-term labor force projections to 2050 Mitra Toossi in January 2012: Labor force projections to 2020: a more slowly growing workforce I asked Doug Short at Advisor Perspectives to plot the difference as a follow-up to my post About That "Expected" Drop In Participation Rate. As you can see, the participation rate is plunging even faster than the recent January 2012 projections.

76% of Decline In Participation Rate Since 2006 Was Unexpected The current participation rate is 63.7. In 2006, Toossi estimated the participation rate would be 65.6, a drop of .6 percentage points from 66.2. Instead, the participation rate fell by 2.5 percentage points. Mathematically, 76% of the decline since 2006 was "unexpected" (1.9 of 2.5). 56% of Decline Since 2000 Was Unexpected In 2000 the participation rate was 67.1. Using that favorable starting point, Toossi expected a total drop of 1.5 percentage points. The actual drop was 3.4 percentage points. Even by the most favorable method, only 44% of the total decline in the participation rate was expected by the BLS. Thus, no matter how one slices or dices the data, there is no realistic way to say the decline in the participation rate was expected. Not even half of it was, by the most liberal interpretation. Regardless, now that we have BLS projections for labor force and participation rates, there are some interesting things we can do with those projections (such as figure out how many jobs it will take to reduce the unemployment rate to 5%, hold it steady, etc.) I hope to have an interactive graph of that idea shortly. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com "Wine Country" Economic Conference Hosted By Mish Click on Image to Learn More Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment