Mish's Global Economic Trend Analysis |

- Unions vs. Banks: Reader Question Regarding Greek Privatization

- Greek Sovereignty Massively Limited; You Cannot Roll Over What You Do Not Have; Railing Against the Truth; EU Seeks to Curb Big Three Rating Firms

- "Hamster Wheel Economy"

- Portuguese 10-Year Government Bond Yield Soars to 13.05%; Italy, Portugal, Ireland, all Fresh New Highs; Focus On the "Unsaved"

- Services ISM "Unimpressive"

| Unions vs. Banks: Reader Question Regarding Greek Privatization Posted: 06 Jul 2011 11:14 PM PDT Reader Jeddy spots what he thinks is a conflict in my typical "privatization" message and inquires Hello MishHello Jeddy, thanks for asking. There is no conflict. I am indeed in favor of privatizing government services. I am not in favor of doing so under duress for the explicit purpose of raping taxpayers for the benefit of banks. I have many times been accused of being a shill for banks. The idea is preposterous. No one has railed against bank bailouts more than I have. Rolling List of High Profile Fraud Targets This list is incomplete. I have stopped updating it, it got so long.

I am not in favor of bailouts. Nor I am in favor of privatizing government services under duress for the explicit purpose of raping taxpayers to benefit of banks. Greece desperately needs reform. Its pension structure and union protectionism must change. The same is true in the United States. Unions attack me for that position. However, I am not willing to rape Greek citizens for the benefit of French banks to achieve that end. Sadly, that is exactly what is happening. Unions should take a hit and so should banks. Anyone taking that stance is attacked from both sides, and I have a ton of emails to prove it. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||||||||||||||||||||||||||||||||

| Posted: 06 Jul 2011 03:51 PM PDT Jean-Claude Junker, the man who says "When it becomes serious, you have to lie", apparently has had a sudden splash of honesty, stating Greek sovereignty to be massively limited. Greece faces severe restrictions on its sovereignty and must privatize state assets on a scale similar to the sell off of East German firms in the 1990s after communism fell, Eurogroup chairman Jean-Claude Juncker said.Massive Loss of Sovereignty is an Insult If I was Greek, I would take a statement regarding massive loss of sovereignty as an insult, not help. Thus, true to form, in aggregate, Juncker's statements are a collective lie. EU Seeks to Curb Big Three Rating Firms Bloomberg reports EU Seeks to Curb Big Three Rating Firms After Portugal Downgrade. European policy makers lashed out at rating companies after Moody's Investors Service cut Portugal's debt to junk, reviving calls to curtail their clout.Truth Not Appreciated I agree with Schaeuble regarding the need to "break up" the rating agencies. I have spoken about this many times. The key article is Time To Break Up The Credit Rating Cartel. Everyone readily accepted lies about US housing debt that anyone with an ounce of common sense could have spotted an ocean away. However, I have to laugh at the irony and motivation of Schaeuble's proposal. The fact of the matter is Moody's , Fitch, and the S&P are finally telling the truth about something. Greek Banks Ready for Debt Rollover Please consider Greek Banks Ready for Debt Rollover as Investors Meet to Discuss Aid Plan Greek banks are willing to roll over their government bonds as part of a European Union aid plan, Finance Minister Evangelos Venizelos said, as debt-holders meet in Paris today to discuss their role in rescuing the country.Incredibly Funny For Multiple Reasons The above story is incredibly funny for more than one reason. For starters Venizelos' statement regarding the "absolutely the voluntary character of this procedure" is straight out of the Jean-Claude Juncker "lie when it's serious" playbook. Venizelos goes on to say he wants to "take the opportunity but not the risk." Everyone knows there is nothing "voluntary" about the debt rollover proposal. The idea is so preposterous even the rating agencies cannot stomach the lie. More importantly ... You Cannot Roll Over What You Do Not Have The Wall Street Journal reports Greek Rescue Snarled by Sales Europe's hopes for a significant contribution by private bondholders to a new bailout for Greece are fading, as it becomes clear that banks have sold off a substantial proportion of their Greek government-bond holdings despite pledges by some of the institutions not to do so.Pledge Not to Dump as Long as it Made Economic Sense Banks dumped some Greek debt and lightened their load. Pray tell what's wrong with that? Everyone should be happy about this, except perhaps banks that were not smart enough to dump when the dumping was good. Could that be French banks by any chance? Pondering the After the Dump Options The chain of amusement continues as Bankers Ponder Greek Debt Options. Bankers on Wednesday wrapped up their latest meeting on a private-sector contribution to alleviate Greece's debt crisis, and the chairman of BNP Paribas SA said they were now pondering a range of options.Stiffing the Taxpayers Please notice the key sentence "The banks are trying to figure out a way to participate in a deal to repackage Greece's debts so that European taxpayers don't have to supply all the funds—but they want to do so in a way that avoids Greece being declared in default." Why should taxpayers have to supply any funds? Was it taxpayers that made stupid bets or banks? Those who made stupid bets should pay for them. Betting on Bailouts As I see it, the secretive dumping transferred some of the risk to hedge funds and others betting precisely on a guess that taxpayers will indeed pony up 100% and debt will be paid back. This takes us back to my June 27 article Leading German Economist Buys Greek Bonds On Belief in "Boundless Stupidity of German Government", Says Bailout Programs Will Exacerbate Problems Stefan Homburg, a leading German economist believes the bailout of Greece is exactly that wrong thing to do and will exacerbate bankruptcy problems.The only thing that makes any sense is a full and complete default. To any extent banks dumped bonds, the better off they will be in a default situation. Make the speculators and the banks not bright enough to dump foot the bill, not taxpayers. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||||||||||||||||||||||||||||||||

| Posted: 06 Jul 2011 11:50 AM PDT Trimtabs says the U.S. economy added 171,000 jobs in June. However, real wage and salary growth is -2.0% year-over-year when adjusted for 3.6% inflation and 2% payroll tax cut. Via Email ... The U.S. economy added 171,000 jobs in June, reports TrimTabs Investment Research. The June gain follows increases of 127,000 in May and 181,000 in April.Going Nowhere Fast Despite the alleged "improvement" in jobs, TrimTabs describes the economy as a "Hamster Wheel Economy" -- the hamster runs faster and faster in its wheel but goes nowhere. Don't Count on a Big Rebound The "rebound" in employment will only cheer the markets if there is a significant rebound. Last month the BLS report was +54,000 jobs. I except to see a rebound above that anemic total. However, I will take the "way under" line on Trimtabs +171,000 jobs estimate for Friday's jobs report. Anything under +125,000 and the unemployment rate is likely to tick up, perhaps significantly. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||||||||||||||||||||||||||||||||

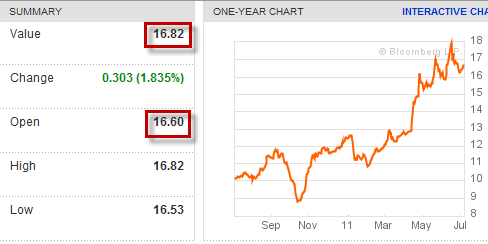

| Posted: 06 Jul 2011 09:41 AM PDT By now, everyone knows that "Greece is Saved" even though 2-year government bonds are trading today at 28.3%, up from 26.62% at the open. Let's turn our attention away from Greece to the "Not Saved Yet" group of countries including Spain, Portugal, Ireland, and the big Kahuna, Italy. Portugal 10-Year Government Bonds - 13.05%  Ireland 10-Year Government Bonds - 12.43%  Greece 10-Year Government Bonds - 16.82%  Spain 10-Year Government Bonds - 5.61%  Italy 10-Year Government Bonds - 5.12%  Please note that 10-year yields in Italy are now approaching 10-year yields in Spain. Also note that yields are not up across the board in Europe. Germany 10-Year Government Bonds - 2.93%  Today's Scorecard

I don't know about you, but I am sure glad "Greece is Saved". I look for equally impressive results when Portugal, Ireland, Spain, and Italy are "saved". Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

| ||||||||||||||||||||||||||||||||||||||||||

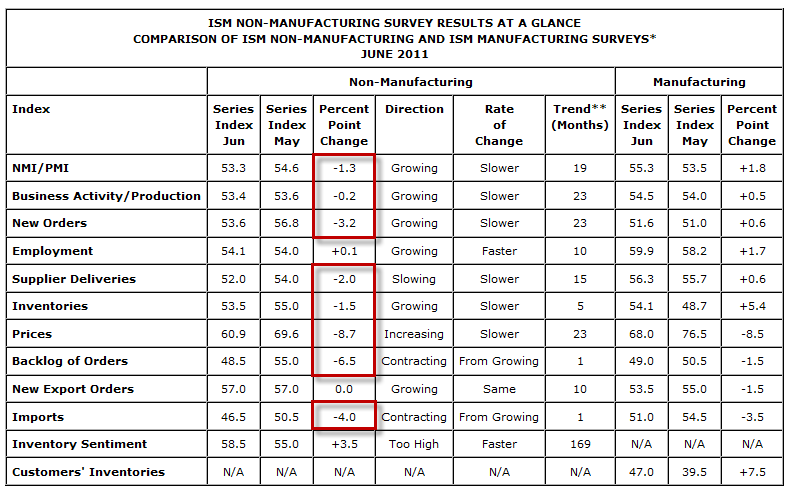

| Posted: 06 Jul 2011 08:23 AM PDT Manufacturing rebounded last month largely on the "strength" of inventory rebuilding, but the services ISM came in weaker than expected. Nigel Gault, chief U.S. economist at IHS Global Insight, summed things up nicely in one word "unimpressive". Please consider the June 2011 Non-Manufacturing ISM Report On Business®  click on chart for sharper image Expectations were for 53.7, the index came in at 53.3. This was not a disaster, it just was not very good. Employment was the one bright spot, but it was up a statistically meaningless .1. Backlog of orders is contracting, as is the backlog of manufacturing orders. I expect more weakness coming in both the services ISM and the manufacturing ISM in the months ahead. Inventory rebuilding will not sell cars, boats, or durable goods in general. In case you missed it, please see Manufacturing ISM Weaker Than it Looks; Digging Into the Numbers; Inventory Restocking Accounts for Much of the Rise Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment