Mish's Global Economic Trend Analysis |

| Posted: 04 Jul 2011 11:52 AM PDT Before receiving the next bailout tranche, Greece May Have Missed June Primary Balance Target Greece is at risk of missing a key budget target in June, European Union experts said in a report, a sign of the uphill struggle the country faces as it tries to get its deficit reduction plans back on track.Spoon Feeding will Continue Regardless of Shortfalls Short of telling the ECB, EU, and IMF to go to hell, nothing will stop the Plan to Spoon-Feed Greece to Death The original bailout was 110 billion Euros, now it takes another $85 billion (and counting). When the fire sale of Greek assets does not bring in enough money, the banks and IMF will place even harsher terms on Greece.French Plan to "Save Greece" Constitutes Default The New York Times reports S.&P. Warns Bank Plan Would Cause Greek Default Greece risks being judged in default on its debt obligations if banks are forced to bear part of the pain, Standard & Poor's said Monday, suggesting that current proposals for rescuing the euro zone's weakest member may have to be reconsidered.Rating Agency Rollover Default Conditions

Point number one deals with the "voluntary" nature of the dealing. If banks roll over debt under duress, fearing bigger losses if they don't, the rating agencies will not consider that a "voluntary" rollover. Even if a voluntary rollover can be constructed, condition number two must still be satisfied. I fail to see how that is possible, at least without destroying Greece. Making Sense of the French Rollover Plan There is a nice article on Zero Hedge by Peter Tchir of TF Market Advisors called Making Sense of the French Rollover Plan The French proposal is slightly complex at best and convoluted at worst. Before digging into the specifics, let's look at what a true rollover would look like. If Participants agreed with Greece to extend the maturity AND reduce the coupon AND do it immediately, that would be a clear example of a rollover that benefited Greece.We need to stop right there. What Tchir says is true, but since when is the plan to benefit Greece? Moreover, even if the plan was to benefit Greece, notice the key phrase "the Participants would have made a sacrifice. " A sacrifice implies "investors receive less value than the promise of the original securities". That in turn implies default, at least to the rating agencies. Tchir continues ... The French proposal, as we will see, potentially does not satisfy any of the 3 aspects listed – it is not immediate, the coupon will be higher than existing debt, and the maturity extension is linked to taking some debt out of the market, so it's not as clearly a benefit as the headlines make it seem.The rating agencies have taken the position (right or wrong), that if a rollover is done under duress, the rollover is not voluntary. However, Tchir goes on to say "The Rating Agencies can be largely ignored". The plan as it stands is complicated. Tchir does his best to explain it by comparing the rollover to 30 year mortgages. The Participants are not lending to Greece for 30 years, the duration is much shorter, and the coupon payments start out potentially high, and become usurious in the later years.Greece has had no say in this for the simple reason the plan is not to save Greece, but rather save the French banks who are most on hook should Greece default. It will be interesting to see if the plan changes now that the S&P has warned the French plan for Greece constitute default. Even if the plan is modified, I do not see how it can be modified to meet the "voluntary" rollover criteria of the rating agencies. Unless Tchir is correct that the rating agencies truly are irrelevant, something has to give. Actually, something has to give anyway. The situation in Greece is so dire, and the economy, politics and riots so messy that Greece is going to default sooner or later anyway. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

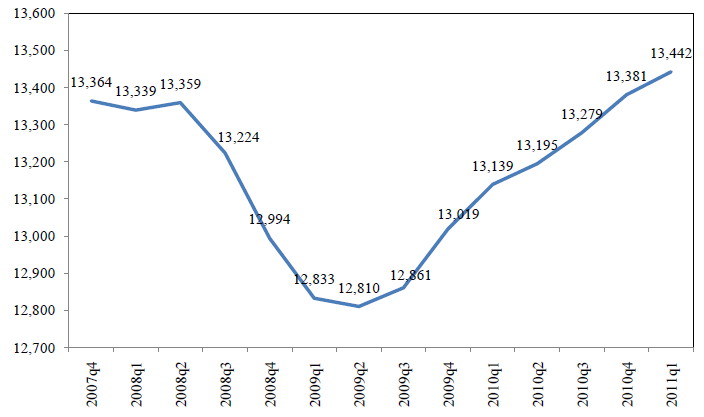

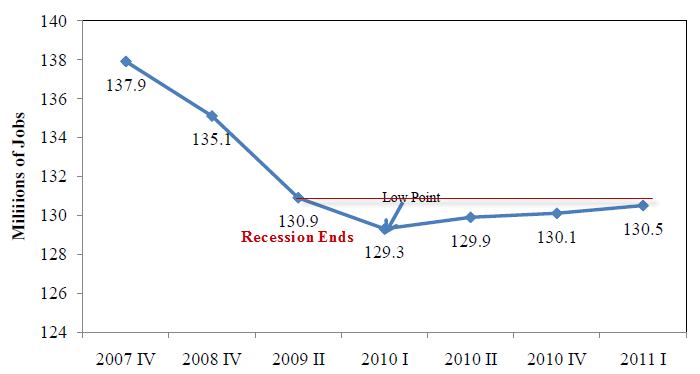

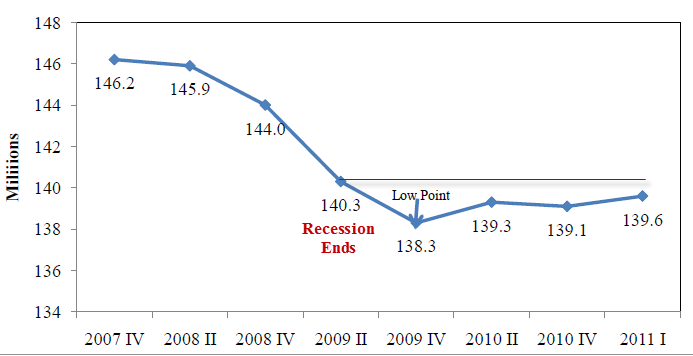

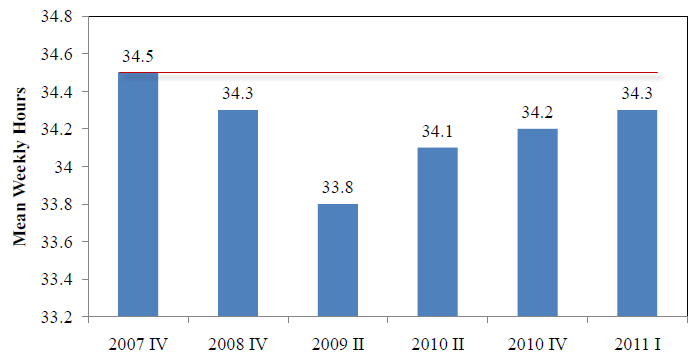

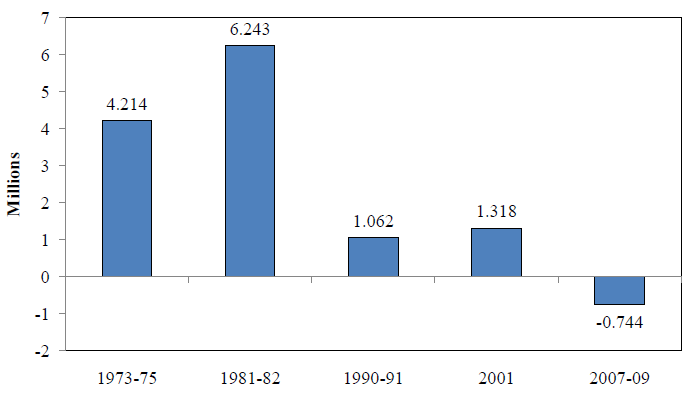

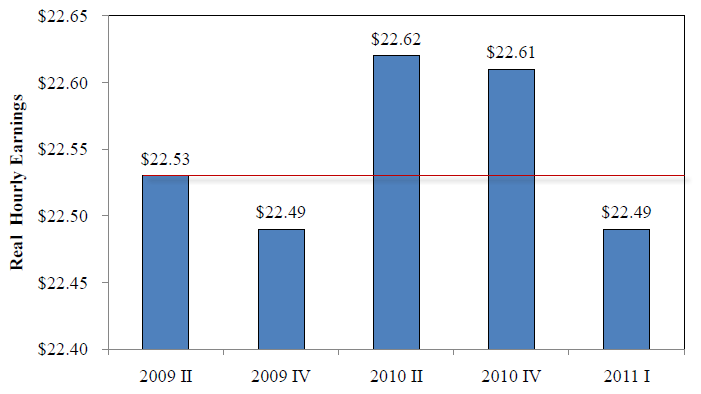

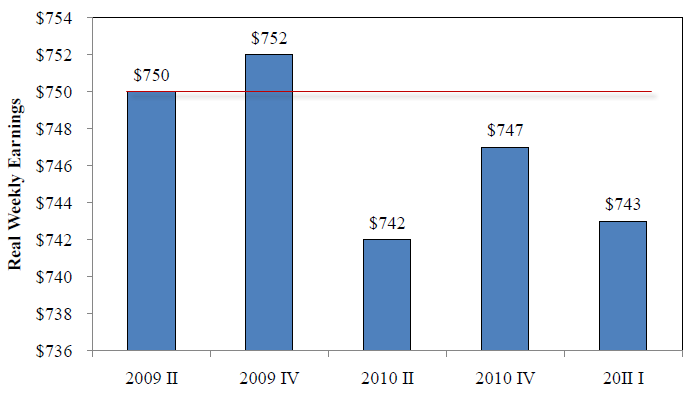

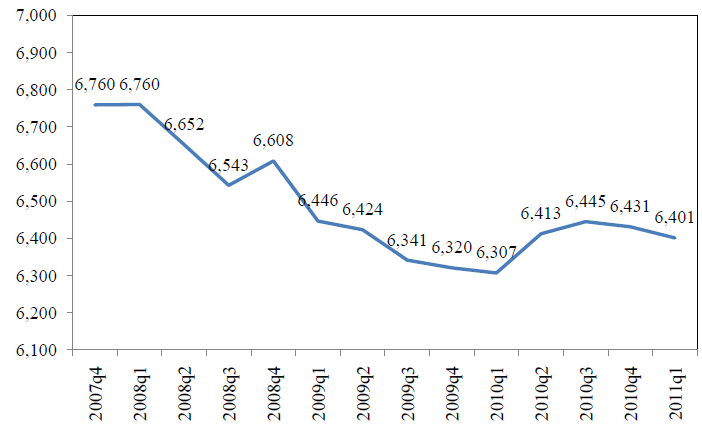

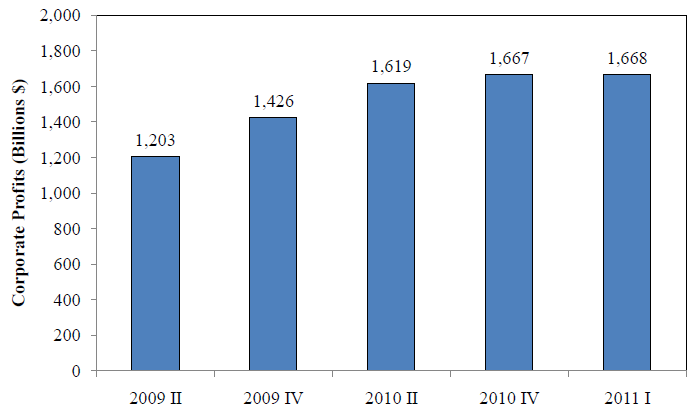

| "Jobless and Wageless" Recovery in Pictures; Trends in Jobs and Wage Growth Posted: 04 Jul 2011 09:51 AM PDT Please consider a collections of charts from The "Jobless and Wageless" Recovery from the Great Recession of 2007-2009. Annotations in red (where present)are by me. GDP 2007 Q4 - 2011 Q1  GDP made a new high but look at the amount of US fiscal stimulus from Congress, monetary stimulus from the Fed, and global stimulus especially China, that it took to achieve that. Nonfarm Jobs  Total Civilian Employment  By the "end" of the recession the US economy shed 7 million nonfarm jobs and 6 million civilian jobs. Since the official end of the recession, there has been a small net loss of both nonfarm jobs and civilian jobs. Mean Weekly Private Sector Hours  Mean weekly hours have risen by .5 hours since the recession ended but are still .2 hours below the start of the recession. Change in Civilian Jobs vs. Prior Recessions 7 Quarters Later  Private Sector Real Hourly Earnings in Constant 201o Dollars  Thanks to the Fed specifically and central bankers in general, real wages are below where they were when the recession ended. Real Median Weekly Earnings Full-Time Wage and Salary Employees in Constant 2010 Dollars  Trends in Annualized Wage and Salary Accruals CPI-U Adjusted 2010 Dollars  Annualized Value of Corporate Profits in Constant 2010 Dollars  Snip from the report .... "To date, through the first quarter of 2011, the nation's recovery from the 2007-2009 recession is both a jobless and a wageless recovery. Aggregate employment still has not increased above the trough quarter of 2009, and real hourly and weekly wages have been flat to modestly negative. The only major beneficiaries of the recovery have been corporate profits and the stock market and its shareholders. Most holders of savings and money market accounts also are net losers due to declining real interest rates which have been in negative territory for many interest bearing and money market accounts." There are more charts, tables and commentary in the 23 page PDF report. Given the global economy is clearly weakening (disregarding inventory building and the latest US manufacturing ISM numbers), there is every reason to believe the jobless, wageless, "state of affairs" will last. Notice I called it "state of affairs". The recovery, if that is what one wants to call what we had, is on its last legs. For a look at the latest manufacturing ISM numbers and trends in other countries, please see Manufacturing ISM Weaker Than it Looks; Digging Into the Numbers; Inventory Restocking Accounts for Much of the Rise Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment