Mish's Global Economic Trend Analysis |

- Value Traps Galore (Including Financials and Berkshire); Dead Money for a Decade

- S&P Reconfirms Greek Debt Restructuring Likely a Default; Forget About "Voluntary Restructuring"

- When was the Housing Peak and How Far to the Bottom?

| Value Traps Galore (Including Financials and Berkshire); Dead Money for a Decade Posted: 20 Jun 2011 05:33 PM PDT "Smart Money" sees A Bargain in Berkshire Shares A 52-week low, a long track record, and a modest valuation -- even Buffett would buy, writes Dave Kansas ...Berkshire shares look remarkably cheap. Berkshire hit $109,925 on Wednesday, its lowest level since June 2010. They have since recovered a bit to trade above $112,000, but the shares are still down about 14% since a Feb. 28 high of $131,300. Berkshire's shares haven't traded below $100,000 since January 2010. Berkshire's B shares, which trade at about $75, have performed in similar fashion.Buffet Already Bought Of course Buffett would buy. He already did. The mistake is thinking that "values" of the past decade constitute real value that the market will recognize anytime soon. Take a look at Citigroup. Yahoo Finance reports Citigroup Trades at Price/Book of .64 Lovely. Had you bought at price to book of 1.0 (a tremendous "value" to many) you would be 36 percent in the hole. Take a look Bank of America. Yahoo Finance reports Bank of America Trades at Price/Book of .50 Had you bought Bank of America at "book value" you would be down 50%. Had you bought Citigroup near its peak you would be down 90% or more with a 0% chance of ever getting even. Value Trap Does "book value" constitutes real value? How much of the book value of Citigroup and Bank of America is based on nonsensical not marked-to-market holdings? Ask the same of Berkshire. Even if you conclude Berkshire constitutes real "value", what if the market does not recognize that "value" for a decade or even two? That question may sound silly but it is not. Many stocks in the Japanese Nikkei index trade at or below book value and have for years. Please consider the following chart of the Nikkei. Nikkei Chart Since 1989  click on chart for sharper image The Nikkei peaked above 38,000 in 1989. Two decades later it sits below 10,000. Like the results? Of course you don't. Yet, I would rather place my bets on companies following a 20-year washout than on financial, insurance, or reinsurance businesses (or other value traps) that the market might not recognize for decades, if indeed ever. Sentiment Matters Based on "value", Japanese stocks were cheap in 1995, cheaper in 1999, even cheaper in 2005, and preposterously cheap now. On a similar basis, Berkshire shares may be "cheap" now but why should anyone care if the market may not recognize that for another decade? The first problem is finding something that is genuinely cheap. Citigroup and Bank of America looked "cheap" all the way down. The second problem is book values may be overstated. Does anyone really believe the book value of Citigroup or Bank of America? On the same basis, why should anyone believe the book value of Berkshire? The third problem is timing what is genuinely cheap. The third problem pertains to PE compression cycles. What was "normal" for the past decade has nothing to do with "normal" at all. PE ratios expanded to enormous heights and now we are in a period of PE contraction. Thus, assuming one does believe Berkshire is undervalued (I don't) , is there any reason to suspect the market will recognize that "value" anytime soon? Negative Results For Another Decade If you think Berkshire is a scorching buy, please consider the following:

Count me in the group that says earnings estimates are horrendously overstated and unsustainable. However, let's assume I am wrong about earnings. Assume Berkshire is a "screaming buy" based on earnings or other metrics. What difference does it make if it takes the market 10 years to recognize that point of view? Reversion to the Mean My point is that not only will earnings revert to the mean, but so will P/E valuations. That is a double whammy to stocks in general and applies to Berkshire as well. If "either" earnings or valuations revert to the mean, it spells problems for equities at current valuations. Berkshire, Bank of America, and Citigroup are all dead money "value traps" and may be for a decade just as Intel and Cisco were after the dotcom bust. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| S&P Reconfirms Greek Debt Restructuring Likely a Default; Forget About "Voluntary Restructuring" Posted: 20 Jun 2011 01:46 PM PDT Unless this is a planned setup of some sort, forget about this mad dash by EU officials and the ECB to come up with a "Voluntary Restructuring" plan that will not constitute a default. For the nth time, the S&P has reconfirmed Greek debt restructuring likely a default "Past experiences show that restructuring the debt of a country, whose creditworthiness is rated at CCC like Greece is currently, tend not to be voluntary and investors must sustain losses," Moritz Kraemer told Die Welt in an article due to be published on Tuesday.From the point of view of default, it may not matter what agreement anyone pulls out of their hat at the last second. Before a ruling by the S&P would even matter, Greek Prime minister George Papandreou must first survive a vote of confidence. Second, the Greek parliament must agree to conditions set by the IMF and EU. However, whether or not Papandreou survives a vote of confidence likely does matter. If Papandreou does not survive, the odds of an very disorderly event in the near-term go way up. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

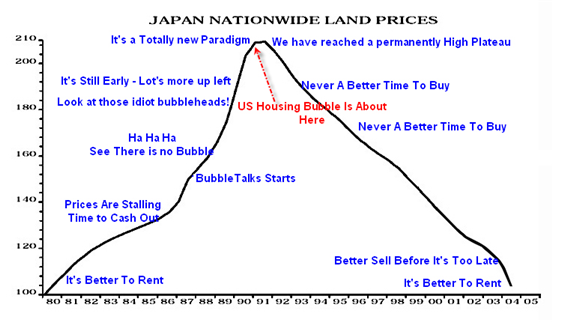

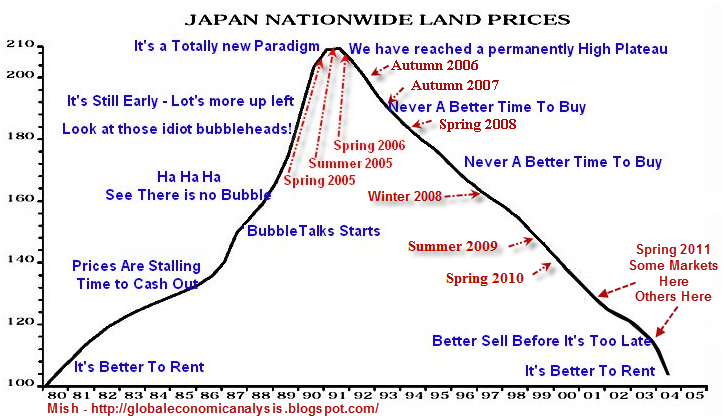

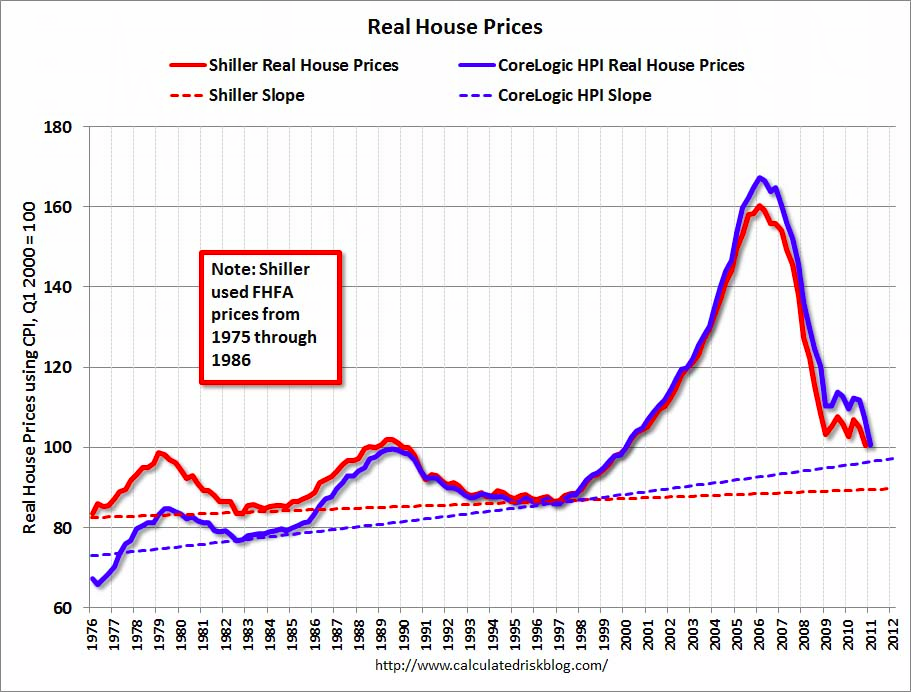

| When was the Housing Peak and How Far to the Bottom? Posted: 20 Jun 2011 10:32 AM PDT Have housing prices bottomed? If not, when will they? Barry Ritholtz at the Big Picture Blog has recently chimed in on that question, and in response Calculated Risk chimed in. Barry posted this projection in Case Shiller 100 Year Chart  click on chart for sharper image Based on the Upward Slope of Real House Prices Calculated Risk does not think home prices will fall as Barry suggests. I've argued that "In many areas - if the population is increasing - house prices increase slightly faster than inflation over time, so there is an upward slope for real prices."Japan Nationwide Land Prices I have been following a different kind of model. Flashback March 26, 2005: It's a Totally New Paradigm  Here are some excerpts from that post.

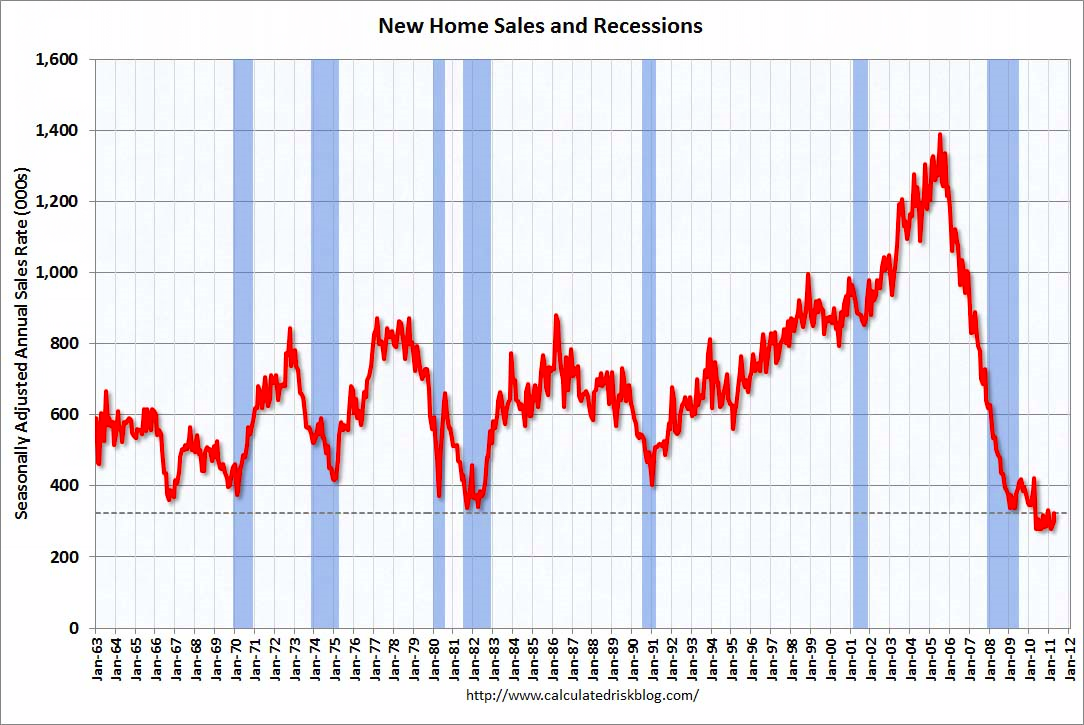

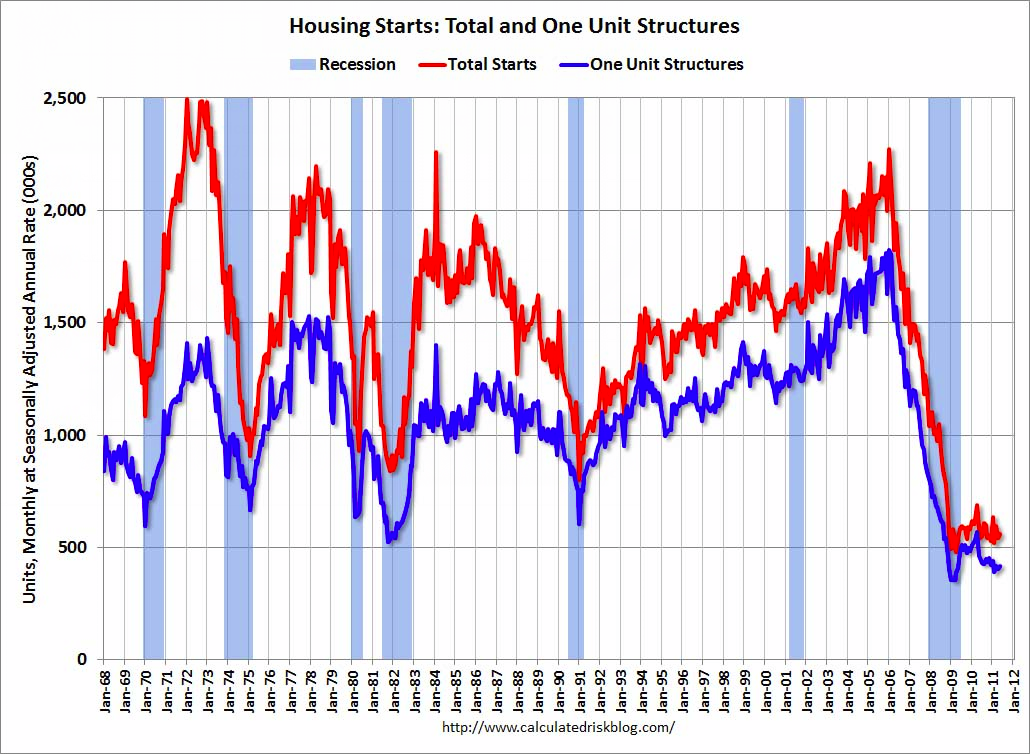

I called the top of the housing bubble in summer of 2005 based on the Time Magazine Cover "Why We're Going Gaga Over Real Estate" and have been updating the chart ever since, in real time. When was the US Housing Peak? Case-Shiller has the peak in summer of 2006. I have it in summer of 2005. Case-Shiller is a lagging indicator. It uses a three-month moving average published with a two month lag. Moreover, Case-Shiller only looks at home resales, not condos. Resales did not catch the action in cash back schemes, incentives, and fraud. In summer of 2005 the condo market bit the dust in many places. Also home builders started discounting heavily. Those discounts did not show up in prices for many months, but rather in incentives such as "free" three-car garages, free granite counter-tops, free cars, etc. Finally, there were massive fraudulent schemes starting in 2005 that overstated home prices, notably cash back to buyers at closing. Thus, contract prices did not reflect real costs to buyers for numerous reasons, and Case-Shiller did not pick up on that immediately. Where Are We Now?  I think housing in some areas is very close to a bottom. Others areas have more to drop. Based on inventory, shadow inventory, and boomer demographics, home prices are not going up significantly for a long time yet, perhaps a decade, even if they have already bottomed. There is certainly no reason to rush. Finally, anyone with any uncertainties regarding their employment has no business even thinking about buying now. Flashback October 27, 2007: When Will Housing Bottom? The following charts are from a friend who goes by the name "BC".Please compare the above projections with recent charts by Calculated Risk. New Home Sales  Housing Starts  Humorous Look at 2008 Bottom Calls While searching for my housing bottom link from 2007, I stumbled across Rebuttal To SmartMoney Housing Bottom Call from May 2008. Donald Luskin at SmartMoney is making a case that Housing Prices Near or at BottomClick on above link for my rebuttal.Today home prices have fallen so much, mortgage rates are so low, and personal income is so high — that homes are more affordable today than at any other time, ever — with mortgage payments on the average home eating up about 40% of income. When I proposed 2012 as a possible bottom way back in 2007, many people thought I was out of my mind. Certainly Luskin must have felt that way. Well, here we are, six months away, prices falling fast, and the economy likely headed for another recession. 2012 may still be an optimistic target for a bottom but we are certainly closer to the bottom now than we were than we were in 2007 or 2008. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment