Mish's Global Economic Trend Analysis |

- Shanghai Prepares for Property Tax to Curb ‘Speculative’ Buying; China Addresses Symptom NOT Problem

- MP3 of My WLS AM Saturday Evening Session on Quinn and Illinois Taxes

- Baby Steps or Simply Mush from Christina Romer Regarding "What Obama Should Say About the Deficit"

| Shanghai Prepares for Property Tax to Curb ‘Speculative’ Buying; China Addresses Symptom NOT Problem Posted: 16 Jan 2011 06:08 PM PST China's problem is rampant growth in money supply. Instead of curbing the problem, China prepares to address the symptoms, city by city it appears. Please consider Shanghai Prepares for Property Tax to Curb 'Speculative' Buying Shanghai, China's financial center, will this year prepare for a trial property tax, becoming one of the first cities in the nation to introduce the measure aimed at curbing "speculative" investment.Unworkable Measures 1. Offering subsidies to control housing prices adds to the demand for houses. 2. Taxing houses to curb prices is complete silliness if you are just going to turn around and subsidize the tax. 3. Even without the subsidy, the problem is not prices. Rapidly rising home prices are a symptom of too much credit. In case you missed it, please see Chinese Bank Lending Spree Continues; $75 Billion New Loans First Week in January Alone; Inflation Gone Amuck China's official inflation is 5%. Unofficially, estimates are 10% as noted in China's Foreign Exchange Reserves Jump by Record $199 Billion; Cost Push Inflation from China? Don't Count On It!You cannot fight problems by attacking the symptom. It is tantamount to putting a person in a meat cooler to fight a fever. In this case, excess credit will go somewhere else. Perhaps more commodity speculation. Chinese Pig Farmers Speculate In Copper This story is a little dated as it is from September 17, 2009, but it exemplifies the problem with fighting symptoms. Please consider China's Pig Farmers Amass Copper, Nickel Pig farmers and other speculators may have amassed more than 50,000 metric tons, Jeremy Goldwyn, who oversees business development in Asia for London-based Sucden, wrote in an e- mailed report after a visit to China. That's about half the level of inventories tallied by the Shanghai Futures Exchange, which stood last week at a two-year high of 97,396 tons.Also see Pig Farmers are Making Brent Nervous, from November 11, 2009. Before getting into to the relationship between copper and pork products, I want to draw your attention to what makes me nervous, have a look at these photos from China. They are excerpted from a China Central Television Channel (CCTV) program documenting private speculation and hoarding of metals throughout the country. According to an associate of mine at an Asia-focused hedge fund who was just in China, "It's pervasive; people are piling this stuff up in their backyards."Michael Pettis on Lending Quotas Inquiring minds are reading China's lending quota? by Michael Pettis. It seems to me that if Beijing wants GDP growth in 2011 to come in at the expected 9%, the amount of new investment in China – which is determined in large part by the banking system – is really not something they can decide today. It is going to be whatever it needs to be given developments in household consumption growth and the trade surplus.China is overheating, it needs to slow the growth of credit. Instead, it is hell-bent on idiotic measures that cannot possibly work. So, China is going to overheat until it implodes. In the meantime everyone is going gaga over China's growth and growth targets that are not possibly sustainable. How do we know that? Easy, China's property bubble and inflation problem (massively understated at that), tells us all this "growth" is nothing but malinvestment, quite similar to the "growth" the US saw in its property bubble. We know how that ended, and it will end the same way in China, Australia, Canada, the UK, and India as well. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| MP3 of My WLS AM Saturday Evening Session on Quinn and Illinois Taxes Posted: 16 Jan 2011 04:00 PM PST Saturday Evening I was on "The Eddie & JoBo Show" WLS 890 AM talking about the Quinn recall and Illinois taxes. I have an MP3 of the session. Click here to Download and Listen. The segment is about 14 minutes long and was a lot of fun. Play it to the end. It goes on for about a minute after the stated cutoff. They took one ad-hoc call that's pretty funny. For more on the Quinn Recall please see

Please click on the first link in the above list to volunteer help. Also pass a link to this post to your friends and have them do the same. Illinois Pension Funding Worst In Entire U.S. To gain an understanding of the sorry state of Illinois pension funds please see Interactive Map of Public Pension Plans; How Badly Underfunded are the Plans in Your State? Once the map pops up, click on Illinois. Taxpayers ought to be scared to death by Illinois pension plan funding with governor Quinn at the helm. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Baby Steps or Simply Mush from Christina Romer Regarding "What Obama Should Say About the Deficit" Posted: 16 Jan 2011 01:41 PM PST Christina Romer is the out-going Chair of the Council of Economic Advisers in the Obama administration. She is now member of the President's Economic Recovery Advisory Board. She has an Op-Ed economic view in the New York Times, What Obama Should Say About the Deficit. This year, instead of being on the floor of Congress with the rest of the cabinet, I will be watching on television with the rest of the country. Instead of knowing what is coming, I can write about what I hope the president will say. My hope is that the centerpiece of the speech will be a comprehensive plan for dealing with the long-run budget deficit.So far so good. Romer is saying all the right things. That is the Romer we knew and loved. However, watch the article morph into compete mush in a matter of sentences. She continues... So what should the president say and do? First, he should make clear that the issue is spending and taxes over the coming decades, not spending in 2011. Republicans in Congress have pledged to cut nonmilitary, non-entitlement spending in 2011 by $100 billion (less if recent reports are correct). Such a step would do nothing to address the fundamental drivers of the budget problem, and would weaken the economy when we are only beginning to recover.Did you catch that? Romer did not name one cut! Instead she called for ...

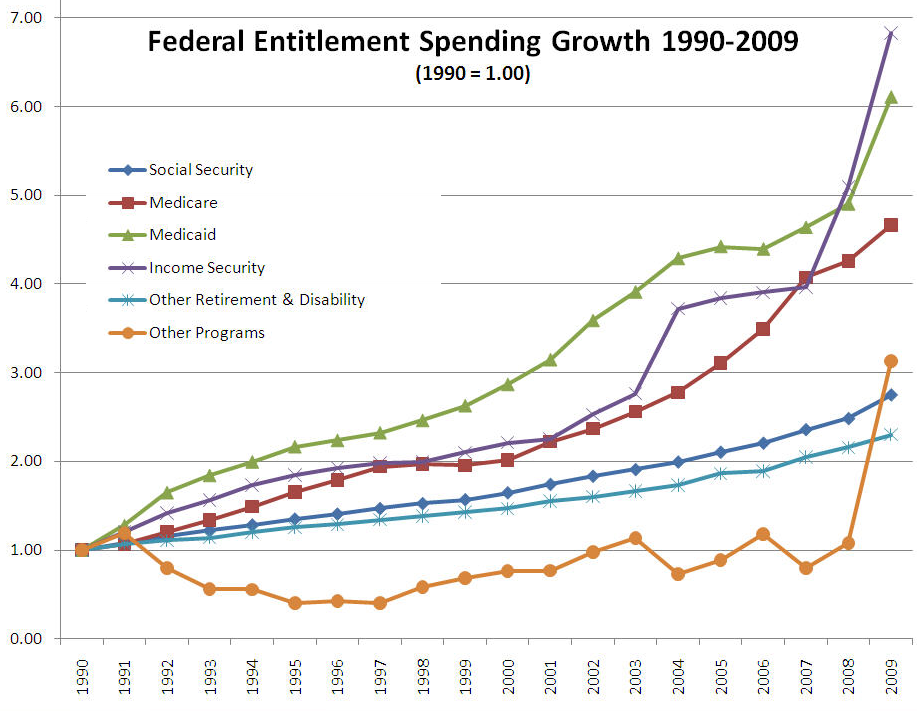

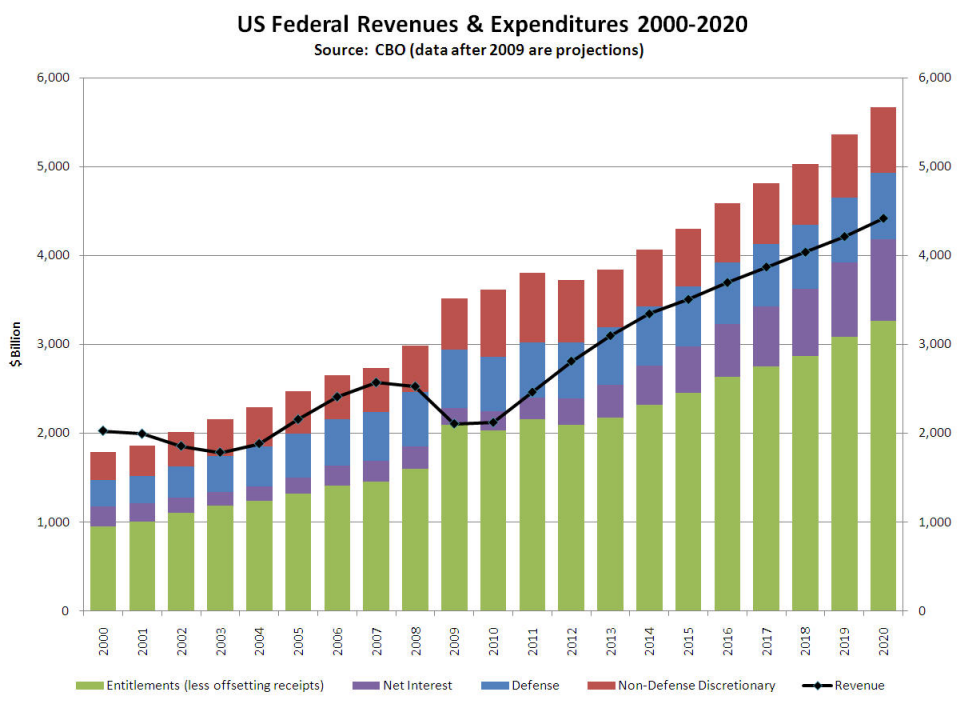

Complete Mush For starters, the Independent Payment Advisory Board would be another totally useless board that will cost taxpayers money because the study would be tossed in the gutter by Congress before anyone even reads it. We know that simply from the title of it (see word #3). Sadly, Romer tells the President what he needs to do in plain simple English then drafts a proposal for a speech that calls for nothing of the kind. Since when is a slowing of growth called a "cut". Since when is a "cap" a cut? Worse yet, note the proposed cap is on "nonmilitary, non-entitlement spending". It is mandatory we CUT military spending and she cannot even mention cap except for piddly nonmilitary, non-entitlement spending. Budgetary Delusions: Federal Deficit Charts from CBO Budget Projections Let's review Budgetary Delusions: Federal Deficit Charts from CBO Budget Projections Can the budget deficit be solved by cutting earmarks? How about cutting 100% of all federal non-defense discretionary expenditures?That chart is from reader "David" and is based on budget projections from the CBO. The main point is from now until 2020, we could eliminate 100% of all federal non-defense discretionary expenditures and still run a deficit. Romer's proposed "cut" is to cap it. Meanwhile check out the following chart. Entitlement Spending Growth  click on chart for sharper image Both charts are from David who posts on the No Money No Worries blog. Mind To Mush Romer's mind has clearly gone to mush. Let's see if we can figure out when that happened. In 2007 her mind appeared to be in working order. I make that claim based on a review of The Macroeconomic Effects of Tax Changes, an article regarding "Exogenous Tax Changes" classified as "any tax change not motivated by a desire to return output growth to normal". Here are a few select quotes. Exogenous Tax Change Effects

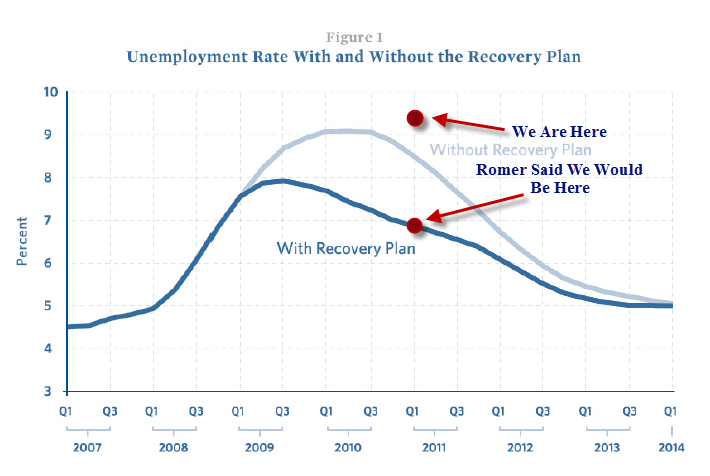

Romer's Conclusion Our baseline specification suggests that an exogenous tax increase of one percent of GDP lowers real GDP by roughly three percent. Our many robustness checks for the most part point to a slightly smaller decline, but one that is still well over two percent. Second, these estimated effects are substantially larger than those obtained using broader measures of tax changes, such as the change in cyclically adjusted revenues or all legislated tax changes. This suggests that failing to account for the reasons for tax changes can lead to substantially biased estimates of the macroeconomic effects of fiscal actions. Third, investment falls sharply in response to exogenous tax increases. Indeed, the strong response of investment helps to explain why the output consequences of tax changes are so large. Fourth, the output effects of tax changes are highly persistent. The behavior of inflation and unemployment suggests that this persistence reflects long-lasting departures of output from its flexible-price level, not large effects of tax changes on the flexible-price level of output.Romer on the Unemployment Rate Please consider Figure 1 from The Job Impact of the American Recovery and Reinvestment Plan by Christina Romer, January, 9, 2009.  As Figure 1 shows, even with the large prototypical package, the unemployment rate in 2010Q4 is predicted to be approximately 7.0%, which is well below the approximately 8.8% that would result in the absence of a plan.Mind Mush Disease Romer's mind appears to have turned to mush sometime slightly before or slightly after she was appointed as Chair of the Council of Economic Advisers. Either way, we can see that Romer's mind is still mush after she left that position. Proof if the New York Times column she just wrote. Then again, it's fair to point out she is now member of the President's Economic Recovery Advisory Board. Perhaps that explains the continued progression of MMD "Mind Mush Disease". Regardless, somehow, somewhere along the way, she started thinking that slowing growth was the same thing as a cut. Somehow, somewhere along the way, she started thinking that "capping" nonmilitary, non-entitlement spending" would make a difference. For the sake of macroeconomists everywhere, we must answer the crucial question "Did Romer's mind turn to mush slightly before she was appointed (explaining why she was appointed), or did her mind turn to mush after she was appointed? Either way, the safe thing for economists to do is refuse such appointments. Then again, if all economists acted on that simple principle, only those whose minds are already mush would accept such appointments. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment