Mish's Global Economic Trend Analysis |

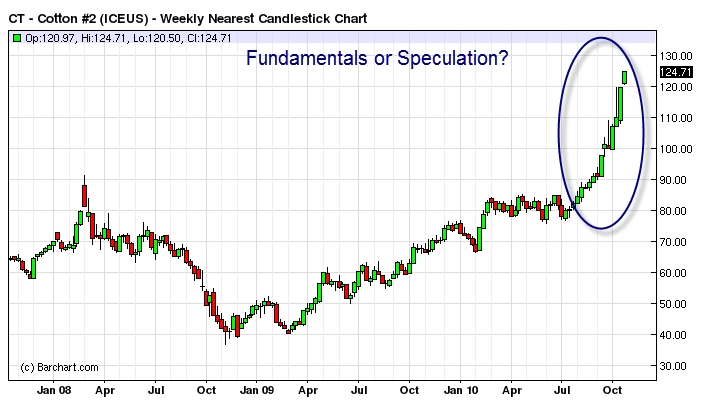

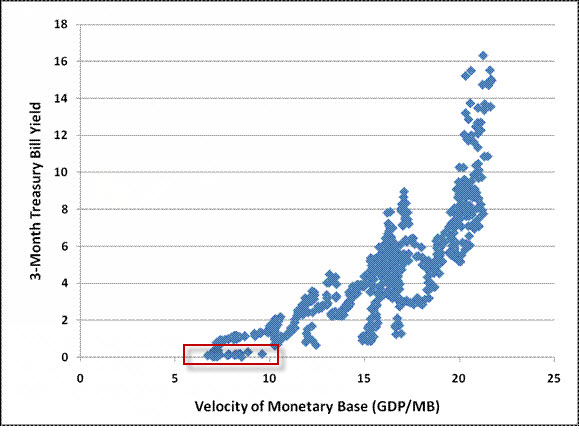

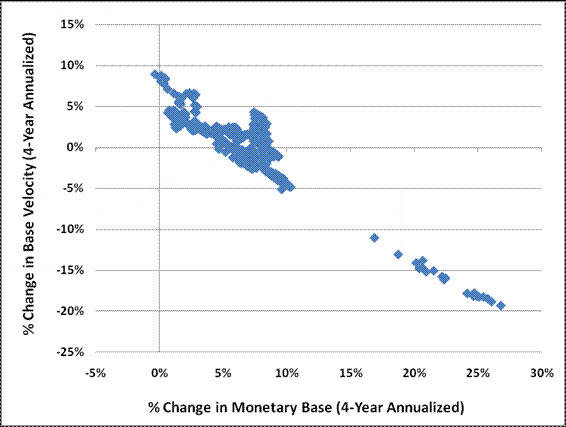

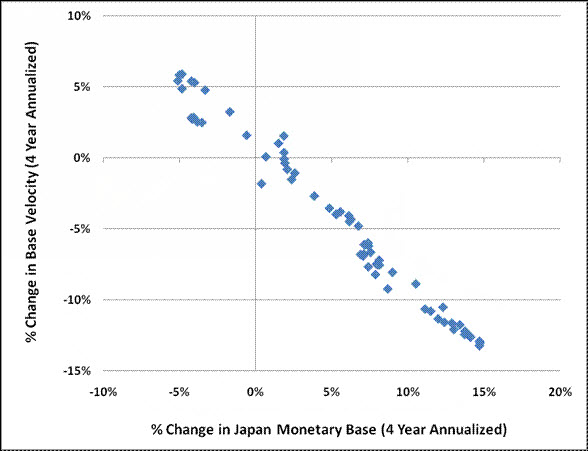

| Liquidity Traps, Falling Velocity, Commodity Hoarding, and Bernanke's Misguided Tinkering Posted: 25 Oct 2010 11:19 AM PDT John Hussman has an interesting post this week on the misguided policies of the Bernanke Fed and how quantitative easing promotes commodity speculation and hoarding but does nothing for the real economy. Please consider Bernanke Leaps into a Liquidity Trap The belief that an increase in the money supply will result in an increase in GDP relies on the assumption that velocity will not decline in proportion to the increase in money. Unfortunately for the proponents of "quantitative easing," this assumption fails spectacularly in the data - both in the U.S. and internationally - particularly at zero interest rates.That is a decent sized snip, but I assure you there is much more in the article to merit a complete read. Commodity Hoarding Commodity hoarding and speculation and credit growth is rampant in China, as noted in Massive Inflation in China, US Inflation Nonexistent I also happen to have had an email exchange with someone in the apparel industry regarding cotton over the past few days. "AI" Writes ... Mish,Definition of "Factory" Since "Factory" was in quotes, I had to ask exactly what that meant. "AI" responds ... A factory can be an actual production facility or it could be a sourcing agent who outsources production to various facilities. The term is often used interchangeably so I felt the quotes were needed. The same can be said for cotton as it is sometimes used when people are referring to fabric/piece goods. The hoarding example I provided was for actual fabric.Apparel Price Increase Looms? "AI" thinks a huge price increase looms. I am not so sure. Prices can only rise if consumers are willing to pay that price. Are they? For how long? As for hoarding, there is always the risk of a price collapse. Given the fragile state of the economy, a sudden collapse in the price of cotton or commodities cannot be ruled out. Cotton Weekly  Charts like that seldom turn out well for buyers at these prices. Liquidity Trap? I agree with what Hussman is saying about liquidity traps in general and how this "pushing on a string" cannot work. However, the entire notion of a "liquidity trap" is a Keynesian construct that implies "something" must be done. In reality, the best thing to do is nothing. Eventually prices will fall low enough where real demand will pick up. The speculators (in this case the banks), would have been wiped out and the bondholders (mainly the wealthy), would have taken a hit. Sadly that is not what we did. We did not even do the second best thing of funding genuine infrastructure needs. Instead, we bailed out the banks at taxpayer expense, paved a bunch of roads at huge expense that did not need paving, and gave money to states that squandered much of it on public unions. In short, it would be hard pressed to find a policy response worse than what we did. QE cannot work as the charts from Hussman proves. Yet Bernanke is committed to a policy of more of the same from the Fed. Meanwhile, Congress is apt to head the other direction (thankfully) and tighten up, even though Krugman is screaming his fool head off. Please see Krugman and the Inevitable "I Told You So" - Tim Duy "Bad Things Happen When You Fight the Fed"; Final End of Bretton Woods 2? for more detail. The only remaining question is how big various commodity, stock market, and corporate bond bubbles get in the meantime, before things blow sky high once again. Risk is enormous and growing. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

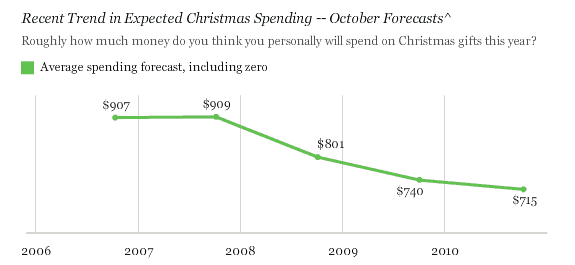

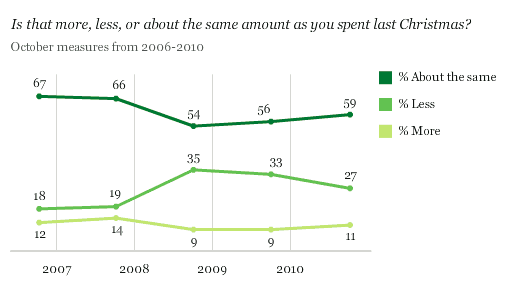

| Gallup: Consumers Plan on Spending Less this Christmas Posted: 25 Oct 2010 08:44 AM PDT A new Gallup poll says Consumers Issue a Cautious Christmas Spending Forecast Gallup's initial measure of Americans' 2010 Christmas spending intentions finds consumers planning to spend an average of $715 on gifts, roughly on par with the $740 recorded in October 2009.Retail Key Unknowns We don't know three things yet. 1. What's Priced In 2. Actual Spending 3. What Type of Stores Will Do Best This is the third consecutive decline. On that basis any decline is significant. However, the final poll in December is a better forecast than this poll. Perhaps people will feel better (or worse) after the mid-term elections. Certainly we are going to see sweeping changes, with Republicans highly likely to take the House, and a decent outside chance of taking the Senate as well. Given the rebound in the stock market, there is a decent chance of a pickup in luxury items. In aggregate, however, the easy guess right now is flat +- 1% for overall spending. Consumers are still tapped out and in need of deleveraging.  Projections Not In Line With Hiring Plans Gallup projections are not in line store hiring plans. Note that Stores Plan Increased Hiring While Offering Increasingly Large Discounts. If stores hire a lot of temporary help, expecting a better season than happens, profits will suffer, especially if there are increasingly large discounts. One key question is "What's Priced In?" We may not know that until January, but I suspect a lot more is priced in than flat +- 1%. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment