Mish's Global Economic Trend Analysis |

- Japanese Politicians fed up with Deflation, Challenge BOJ Independence

- Analysts Cut S&P 500 Profits Forecast; Earnings Estimates Still Overly Optimistic; Stocks Not Cheap

- Factory Orders Drop More Than Expected, Treasuries Rally

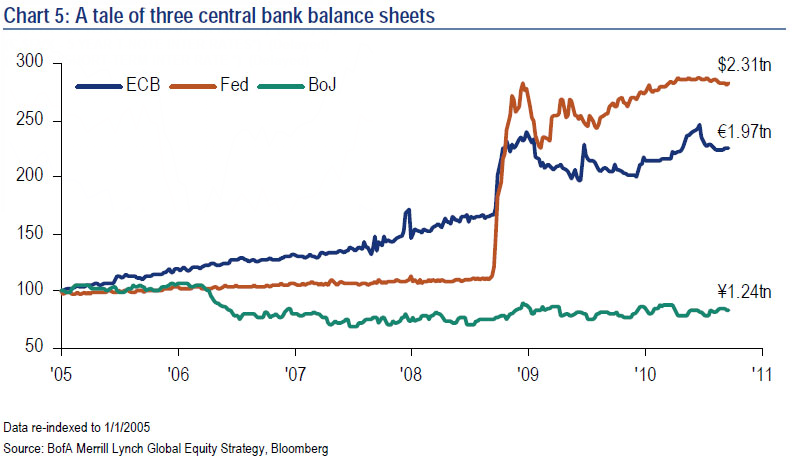

| Japanese Politicians fed up with Deflation, Challenge BOJ Independence Posted: 04 Oct 2010 09:15 PM PDT Things are simmering once again in Japan. The Yen is approaching all-time highs and Japanese politicians have had enough of deflation. Another round of quantitative easing is now on the front burner. MarketWatch reports Bank of Japan may buy asset-backed paper Japan's central bank may announce plans to buy asset-backed securities when it issues its policy decision later Tuesday, the Nikkei business daily reported. The newspaper had reported earlier in the week that the Bank of Japan may expand its low-interest loans to financial institutions. But in the report Tuesday, the Nikkei said "a growing number of board members argue that the bank should go further" and begin buying securities backed by loans to small and medium-sized enterprises. The report, which didn't cite sources, said such a move would be aimed at making more funds available to the private sector.BOJ Independence Under Attack Bloomberg reports BOJ Independence Challenged as Deflation Continues Increasing risks to Japan's recovery prompted what may become the biggest threat yet to the Bank of Japan's independence as politicians seek to redress its failure to end the deflation entrenched in the economy since 1998.Bank Balance Sheets Compared ZeroHedge Asks Is The BOJ Preparing An Imminent Announcement Of Its Own Latest (And Certainly Not Greatest) QE? The BOJ's balance sheet, which has been relatively flat when compared to peer central banks, especially since FX interventions will likely be sterilized, is about to explode and the JPY will plunge once the carry traders reorient themselves to shorting the original carry currency of choice.Politicians Know This Time is Different! It's hard not to laugh out loud at the sarcasm in the last paragraph above. Not only did QE fail to do what the Bank of Japan wanted (raise prices), QE has also failed to stimulate bank lending as Bernanke wants. Moreover, Japan's currency intervention efforts have not accomplished anything, ever. But yeah... this time is different, because .... politicians know better! By the way, this exercise in stupidity by all the central banks in question, shows just how hard it is to destroy a currency, even when you try (except against gold of course). Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| Analysts Cut S&P 500 Profits Forecast; Earnings Estimates Still Overly Optimistic; Stocks Not Cheap Posted: 04 Oct 2010 12:28 PM PDT Bloomberg reports S&P 500 Profits Cut for First Time in Year by Analysts. For the first time in more than a year analysts are cutting their forecasts for Standard & Poor's 500 Index earnings, jeopardizing gains from the biggest September rally since World War II.Earnings Estimates A Mirage It's important to understand why earnings have gone up: Trillions of dollars of stimulus worldwide that is not sustainable. Bank earnings estimates have been inflated by massive extend-and-pretend games encouraged by the Fed with a blind eye from the FASB. Moreover, the FASB has delayed mark-to-market accounting rules and has still not forced banks to bring SIVs and off-balance-sheet assets back on the books. Those assets are held at inflated values. It is disgusting to hear those like Michael Levine of OppenheimerFunds Inc. says "equities are cheap". Equities only look cheap if you use absurd forward earnings estimates, and ignore future writeoffs and other "one-time" items that seem to have a way of recurring with remarkable regularity. Stocks Not Cheap Stocks are not cheap an besides, share prices are not always a direct function of earnings. I talked about that in Sure Thing?! Earnings vs. Share PricesFancy Numbers "You need pretty fancy GDP numbers to get to $95 a share in earnings next year," said Robert Doll, vice chairman of New York-based BlackRock Inc., which oversees $3.2 trillion. "Our view is that they're still a little too high, and that nobody believes them." Robert Doll is half-right. He's right in that "You need more that fancy earnings to get to $95 a share". He's half-right because the consensus believes. Bear in mind we could still see a bit of earnings expansion, but with the inventory replenishment and stimulus coming to an end, and with consumers heading back into a shell, it will not be sustainable. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

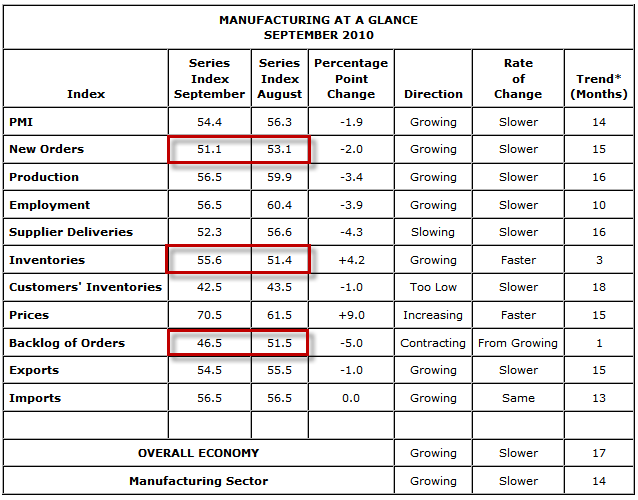

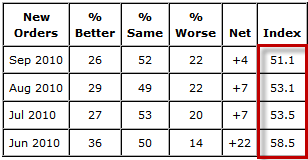

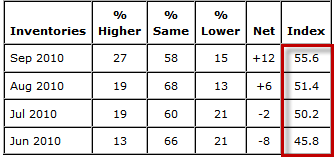

| Factory Orders Drop More Than Expected, Treasuries Rally Posted: 04 Oct 2010 10:42 AM PDT Curve Watchers Anonymous notes the rally in treasuries continues in the wake of the third decline in four months in factory orders and expectations of renewed Quantitative Easing by the Fed. Yield Curve July 2008 - Present  click on chart for sharper image Two-year (not shown above) and five-year treasuries are at record lows. Factory Orders Drop More Than Expected The Wall Street Journal reports Factory Orders Decline U.S. factory orders dropped more than expected in August, marking the third decline in the last four months.That is a very weak report with inventories rising and nearly everything important falling or flat. Durable Goods Drop Should Not Have Surprised Anyone The drop in durable goods may have surprised some but it is consistent with my July 7th post Expect Second-Half Housing and Durable Goods Crash This should have been pretty easy to figure out. If people stop buying houses, and they have, then people will not be buying many appliances for the houses they did not buy. Moreover, autos are big ticket items and with sentiment souring on job prospects, one might have anticipated the auto recovery (as weak as it was), would also stall. Rear View Mirror Look Please note that today's report is a look in the rear view mirror. Today's factory orders report reflects August data. October ISM Recap - Looking Ahead Let's recap a few charts from Manufacturing ISM Expands, Rate Slows, Internals Weak September ISM Manufacturing at a GlanceMore Downward Surprises Coming Today's Factory Orders report (for August) along with the October ISM report (September data as shown above) is further evidence the glowing September ISM report (August data) was an outlier. Expect to see more downward surprises as the vast majority of economists do not understand the implications of the recent ISM data, or the meaninglessness of the Fed's renewed quantitative easing plans. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com Click Here To Scroll Thru My Recent Post List Mike "Mish" Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

|

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment