Mish's Global Economic Trend Analysis |

- GDPNow Forecast Plunges to 0.9% Following Advance Report on US Balance of Goods

- Three Month Treasury Yields Turn Negative; Long End Flattening; Economy Strengthening or Recession Warning?

- Pro-Independence Parties in Catalonia Unite to Form Government; Showdown with Madrid Coming Up

- ISM Flirts with Contraction, Export Orders and Backlogs Contract for 4th Month

| GDPNow Forecast Plunges to 0.9% Following Advance Report on US Balance of Goods Posted: 01 Oct 2015 05:58 PM PDT The past few days have seen significant swings in the Atlanta Fed GDPNow Forecast.  We are right back to the initial forecast in August. What Happened?

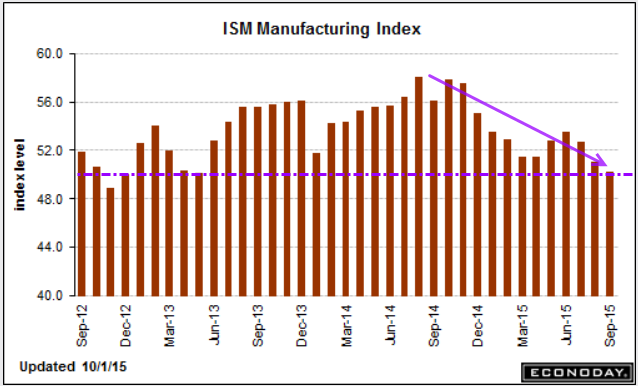

ISM Discussion See my discussion ISM Flirts with Contraction, Export Orders and Backlogs Contract for 4th Month. Advance Trade Numbers Let's investigate the Census Report Numbers to see what's behind the 0.7 percentage point plunge on September 29. The following table I put together will help visualize what happened. Numbers are in millions of dollars. Pay attention to the seasonally adjusted numbers.

Notes:

For the deficit to widen, exports fell, imports rose, or both. Certainly manufacturing exports fell for the 4th consecutive month as noted by the ISM report. Recall that imports subtract from GDP and exports add to GDP. GDP Revisions On September 25, the BEA upped the Second Quarter GDP estimate from 3.6% to 3.9% based on "an upturn in exports, an acceleration in PCE, a deceleration in imports, an upturn in state and local government spending, and an acceleration in nonresidential fixed investment that were partly offset by decelerations in private inventory investment and in federal government spending." Evolution of First Quarter 2015 GDP

GDP Quarter by Quarter

If those numbers hold, the average is about 1.8% annualized. Anyone think downward revisions coming? Question number two: Anyone think the Fed will hike if 3rd quarter GDP is close to or below 1%? Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||

| Posted: 01 Oct 2015 12:05 PM PDT Curve Watcher's Anonymous points out 3-month treasury yields dipped briefly negative on several days recently. Yield on the 3-month bill was negative again today. Here is a table I put together with Treasury Yield Quotes from Bloomberg. Treasury Yields vs. Month and Year Ago

One could also use US Department of Treasury Daily Treasury Yield Curve Rates to produce an end-of-day view as opposed to the intraday snapshop above and chart below. Yield Curve vs. Month Ago and Year Ago  click on chart for sharper image Long End Flattening The time line is not to scale, but the above chart still tells the correct story. In particular, note a negative rate at the front end and the flattening at the long end of the curve vs. a month ago and a year ago. Economy Strengthening? Three month treasuries should not be negative in a rate hike environment. Yields at the short end of the curve, from 6-months to 2-years are slightly higher than a year ago, an indication of anemic hikes. But if hikes are coming, rates should not be lower than a month ago. The yield on 6-month treasuries actually declined 19 basis point in past month. Are hikes really coming? Recession Warning None of this should be happening in a rising rate environment with an allegedly strengthening economy. In fact, action at the long end of the curve coupled with negative yields at the very front end is outright recessionary behavior. Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||

| Pro-Independence Parties in Catalonia Unite to Form Government; Showdown with Madrid Coming Up Posted: 01 Oct 2015 10:54 AM PDT Pro-independence parties in Spain won an outright majority in the Catalonia regional election. The open issue was whether or not the two parties could come to terms and form a government. Election Final Results  Note that prime minister Mariano Rajoy's PP party only got 8.5% of the vote. Suppress people long enough, and radical parties eventually take over. Prior to the election, the leaders of CUP stated they would not work with Artur Mas, the leader of Junts pel Sí (Together for Yes). Today they worked out their differences and will form a coalition regional government. Shared Power El Pais reports CUP Proposes a Presidency with Shared Power in Catalonia. The number two of the CUP in the Catalan elections, Anna Gabriel, proposed Thursday that the new Government would have a "coral presidency", with "three or four profiles with a weight equivalent" to share power, without demanding the political "burial" of Artur Mas. The shared government alternative would unlock the choice of Catalan president, and allow an active role for Artur Mas. CUP Platform CUP is a Popular Unity Candidacy. The CUP platform is what I would call radical leftist. The CUP broadly refers to their economic model as socialist. Their political program calls for a "planned economy based on solidarity, aimed towards fulfilling the needs of the people", and defends the nationalization of public utilities, as well as transportation and communication networks. They also call for a nationalization of all banks receiving government bailouts and consider the public debt "illegitimate".Showdown with Madrid Coming Up The socialist ideas of these groups cannot and will not work. Nonetheless, they are going to try. Reuters reports Victorious Separatists Claim Mandate to Break with Spain. Both groups stated they would "unilaterally declare independence within 18 months under a plan that would see the new Catalan authorities approving their own constitution and building institutions like an army, central bank and judicial system." A serious showdown with Madrid is around the corner. Already, Madrid preemptively acted as noted in Spain's Secessionist Party Leaders to be Charged with "Act of Disobedience" Mike "Mish" Shedlock | ||||||||||||||||||||||||||||||||||||||||||||||||

| ISM Flirts with Contraction, Export Orders and Backlogs Contract for 4th Month Posted: 01 Oct 2015 09:40 AM PDT The ISM is positive at 50.2, but barely above the 50.0 break-even mark, and a bit below the Bloomberg Consensus Estimate of 50.5. The ISM index, like nearly all other September indications, is pointing to trouble for the factory sector. At 50.2, the index is at its lowest point since May 2013. New orders, at 50.1, are at their lowest point since August 2012. Backlog orders, at a very low 41.5, are in their fourth month of contraction and won't be giving manufacturers much breathing room to keep up production. Export orders, at 46.5, are also in their fourth month of contraction and are a key factor behind the general weakness.The ISM Peaked in September of 2014  Together with the various regional reports, manufacturing is clearly in recession. When was the last time the Fed hiked with such weakness? Mike "Mish" Shedlock |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment