Mish's Global Economic Trend Analysis |

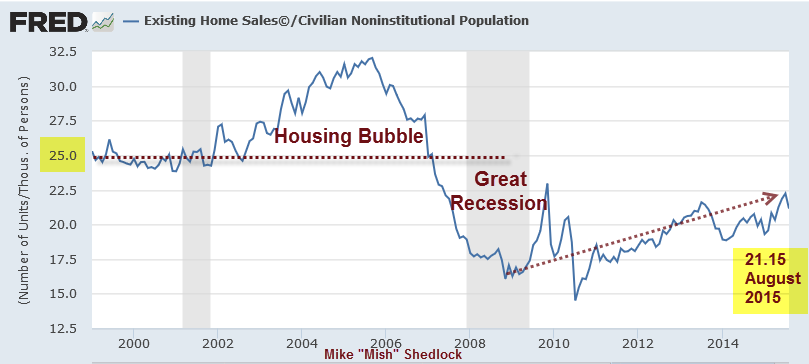

| Posted: 21 Sep 2015 12:56 PM PDT Existing Home Sales Decline More Than Expected Existing home sales in August dipped 4.8% month-over-month to a seasonally adjusted rate of 5.31 million units. Although a decline of 1.7% was anticipated, the actual number was below any estimate in the Bloomberg Consensus Range of 5.4 to 5.6 million. Though slowing in August, existing home sales are still healthy and trending higher. Existing home sales came in at a lower-than-expected 5.31 million annual rate in August which is the lowest since April. July was revised down just slightly but is still an 8-year high at 5.58 million. At 6.2 percent, growth in year-on-year sales is the lowest since February. The year-on-year median price, up only 4.7 percent to $228,700, is the lowest since August 2014. The report cites no special reasons behind August's softness, but notes that it follows prior strength, in fact six months of strength.Still Healthy? What caught my eye in the analysis was the statement by Bloomberg that sales were "still healthy and trending higher." Let's investigate that claim two different ways. Existing Home Sales in Number of Units  click on any chart for sharper image For several years prior to and shortly after the 2001 recession, existing home sales were trending at about 5.2 million units at a seasonally-adjusted annualized rate. During the bubble years, existing home sales rose as high as 7.26 million homes in September of 2005. In July of 2010, sales fell to 3.45 million units, less than half of the peak bubble rate. Home sales are now back to about where they were between January 1999 and August 2002. Existing Home Sales in Number of Units Population Adjusted  In the above chart, I take the civilian noninstitutional population into consideration. The civilian noninstitutional population is defined as people 16 years of age and older residing in the 50 States and the District of Columbia who are not inmates of institutions (penal, mental facilities, homes for the aged), and who are not on active duty in the Armed Forces. On a population-adjusted basis, the number of units sold per thousands of people was pretty steady at about 25 units from 1999 to August 2002. It hit a bubble peak of 32 in September of 2005 and crashed to 14.5 in July of 2010. For August, the number is 21.15 per 1,000 people, a significant gap to years just prior to the housing bubble. Trending Higher or Chopping Around?  In the second chart I was pretty generous to Bloomberg in reference to the idea that existing home sales are trending higher. There was certainly a clear trend between July 2010 and July 2013. Since then, existing home sales have mainly been chopping around sideways. It's often easy to play games with trend lines to support one's view. Mike "Mish" Shedlock |

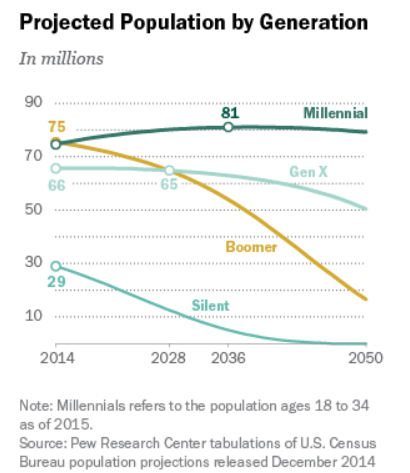

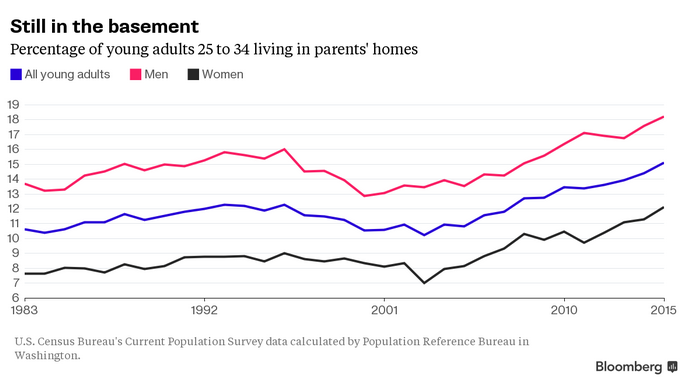

| Posted: 21 Sep 2015 06:07 AM PDT Millennials Overtake Boomers According to Pew Research Millennials will overtake Baby Boomers this year. This year, the "Millennial" generation is projected to surpass the outsized Baby Boom generation as the nation's largest living generation, according to the population projections released by the U.S. Census Bureau last month. Millennials (whom we define as between ages 18 to 34 in 2015) are projected to number 75.3 million, surpassing the projected 74.9 million Boomers (ages 51 to 69). The Gen X population (ages 35 to 50 in 2015) is projected to outnumber the Boomers by 2028.Why are So Many Millennials Still in the Basement? Bloomberg has some interesting charts and commentary in its report Here's Evidence That Millennials Are Still Living With Their Parents. In 2015, 15.1 percent of 25 to 34 year olds were living with their parents, a fourth straight annual increase, according to an analysis of new Census Bureau data by the Population Reference Bureau in Washington. The proportion is the highest since at least 1960, according to demographer Mark Mather, associate vice president with PRB.Goldman Sachs just touched on the reasons. I think we can do much better. Let's expand the list. Eight Reasons Millennials Living With Parents

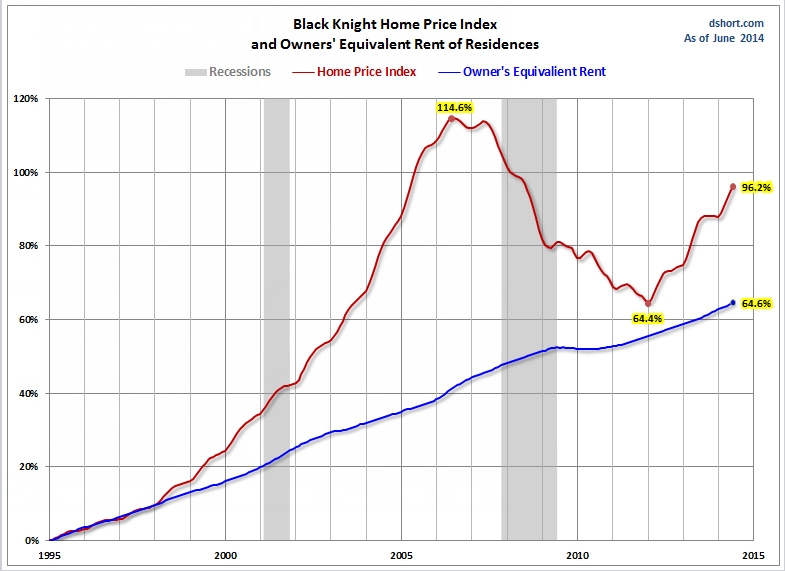

Student Debt Problem number 1, student debt is well understood. But note that the trend towards living at home started rising sharply in 2000, well before the 2007 recession and well before the current student debt crisis. We must go well beyond student debt to explain the trend. Tuition The trend towards living at home took a sharp jump higher just as tuition costs, went through the roof.  Chart from Doug Short's Thoughts on Student Debt. What else happened in the 2000-2002 time frame? The answer is home prices went through the roof. Real Home Prices  The above from Doug Short at Advisor Perspectives. Home Prices vs. Owners' Equivalent Rent  The above chart from my article Housing Prices, "Real" Interest Rates, and the "Real" CPI. Now let's look at real earnings, not just jobs. Here are some snips from my article Real Median Earnings for Men at 1971 Level, Women at 2001 Level Earnings of Men vs. Women - Fulltime Workers  Earnings Progress

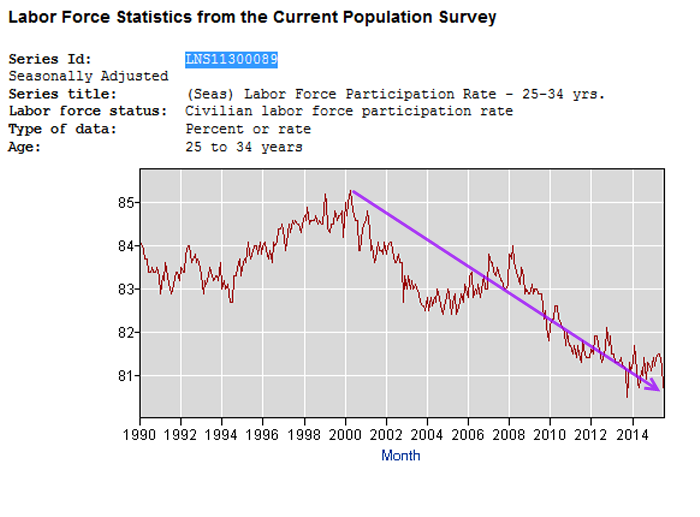

By the way, those "real earnings" numbers assume you believe the government's measure of inflation. Note that the CPI does not reflect home prices or property taxes, and is at best a crude, inefficient, measure of prices. Participation Rate Those aged 18-24 typically do not buy houses and more millennials than ever before are in school. But let's remove school from the equation by looking at the participation rate of those aged 25-34.  Once again we see bad news starting in or around 2000, just as home prices soared. Aging Demographics Until this year, "boomers" were the largest group demographically speaking. Boomers are aging. Many are in poor health, cannot take care of themselves, and cannot afford or do not want to be placed in a nursing home. This need forces many millennials to move in with their parents, simply to take care of them. Silver Lining? Goldman's David Mericle and Karen Reichgot see a "silver lining" based on the idea children will one day leave their parents' basements, and that household formation will prove to be a huge boost to a subpar housing recovery. I take the opposite view based on changing attitudes, real earnings, and a certain inevitability. The inevitability is death. As boomers die off many will simply choose to stay where they are living. This especially holds true where homes are not fully paid off. And there is no reason to believe the trend in real earnings is about to change. So how are the "young and not-so restless" supposed to suddenly get restless unless real earnings take a sharp rise higher? Finally, neither Bloomberg nor Goldman discussed points seven and eight regarding attitudes. Changing Attitudes The Fed has been perplexed as to why its policies have not worked.The explanation is pretty easy. I have been writing about it ever since the housing bust. Kids see their parents and grandparents arguing over debt and ability to pay bills. Many lost their houses to foreclosure. Divorce, suicides, and clinical depressions over the loss of jobs or homes are widespread. And the once widely-held notion that one's home is a retirement nest-egg has been smashed on the hard rocks of reality. Millennials (at least those hit hard in the crisis) don't want to be like their parents, chasing the suburban dream, ill-equipped to take on debt when they have poor-paying jobs and a mountain of student debt on top of it. Pendulums Attitudes are like pendulums in that they move from one extreme to the other before reversing. Unlike pendulums, attitudes take a very long time to go from one end to the other. It took multiple generations for people to fully forget the great depression. Many who were wiped out in the stock market crash of 1929 never got back in. In contrast, boomers had no recollection of the crash. Instead they have recollection of the Fed bailing them out time, after time, after time. Those 18-34 have no recollection of being bailed out of anything. They see the problems that debt caused their parents, and a significant number do not want any part of chasing the boomer's dreams. Eventually the boomers will die and the number of millennials living with their parents will start to reverse. Just don't expect an economic boom from it any time soon. Attitudes towards debt have changed. There is no economic nor demographic reason that suggests the attitude pendulum is close to a reversal. Mike "Mish" Shedlock |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis. To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment