Mish's Global Economic Trend Analysis |

- Interest Rates and Bond Yields: Where are They Headed? September Hike Ideal? Is the Bond Bull Market Over?

- Beige Book Highlights: Will They or Won't They? Still Undecided?

- Canada in Recession with Two Consecutive Quarters of Negative Growth

| Posted: 02 Sep 2015 11:13 PM PDT With all the chatter about whether the Fed will hike on September 17 or not, let's do an interest rate and bond yield recap of where various rates are, where they have been, and where they are likely headed. Effective Federal Funds Rate  As of yesterday, the effective federal funds rate was a mere 8 basis points. Since April, it has been swinging from a low of 6-8 basis points to a high of 14-15 basis points. I suspect the odds of a hike are close to 50-50. The CME Fed Watch has the hike odds at 27% as of September 2. However, the CME does not consider a move to 0.25% a hike. I do, because it clearly is. The current Fed stance is 0.00% to 0.25%. With the effective Fed Funds rate hovering between 8 and 15 basis points, a move to a firm 0.25% would be about an eighth of a point hike. Why nearly everyone expects a quarter point hike is a pure mystery to me. If the Fed delays until December, we may see such a move (if the economy stays reasonably firm), but even then, I believe the Fed will baby-step this in a Market May I approach, quite similar to the childhood "Mother May I" game. Yellen vs. Greenspan

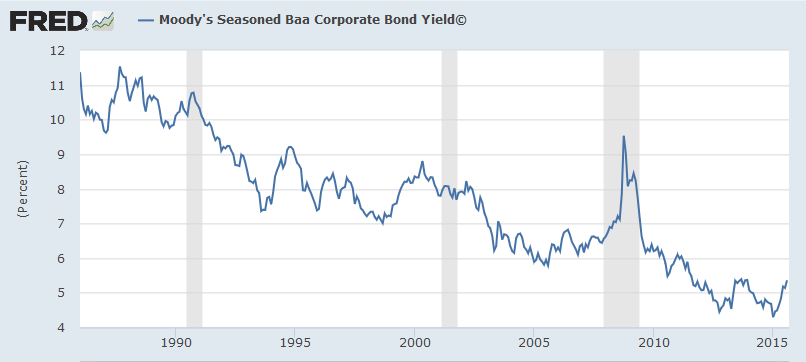

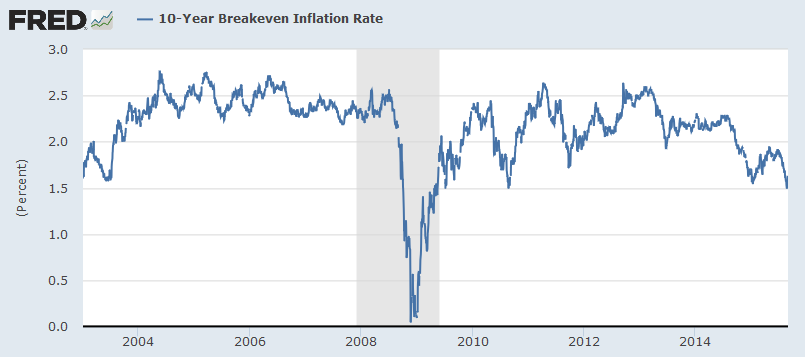

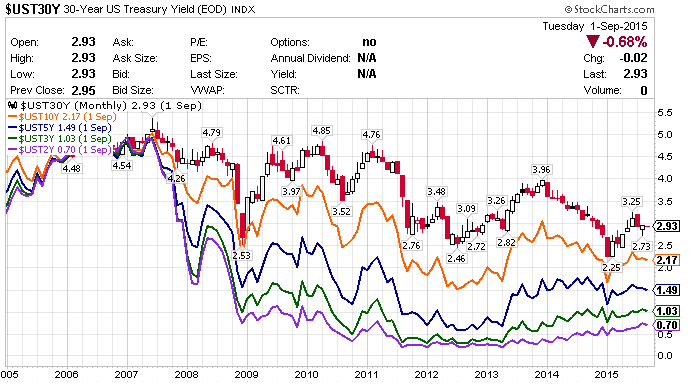

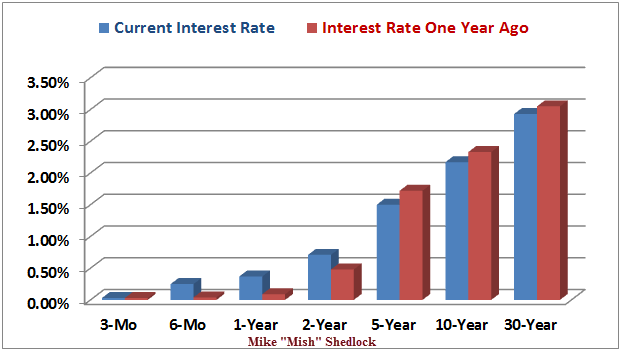

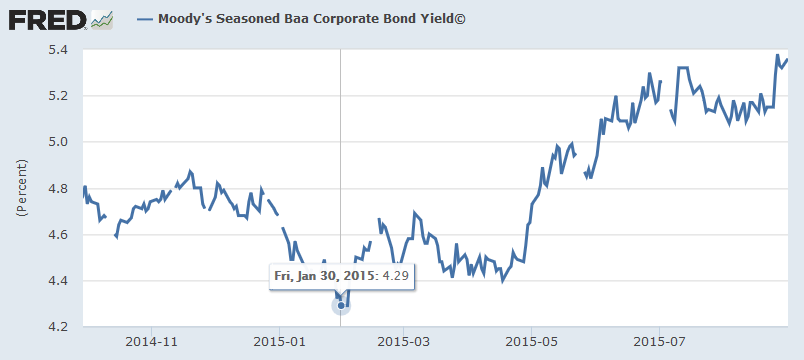

Moody's Seasoned Baa Bond Yield Detail  Baa is Moody's lowest investment grade bond (one step above junk). It is a measure of risk taking appetite. The rise in yield from January is an effective tightening of rates, albeit from a low level. The following long term chart adds perspective. Moody's Seasoned Baa Bond Yield  BB High Yield Bond Yield  BB is the top junk bond rating. Is the yield bottom in? 10-Year Breakeven Rate  Financial Times provides this Definition of Breakeven Rate. The Break-even rate refers to the difference between the yield on a nominal fixed-rate bond and the real yield on an inflation-linked bond (such as a Treasury inflation-protected security, or Tips) of similar maturity and credit quality. If inflation averages more than the break-even rate, the inflation-linked investment will outperform the fixed-rate bond. If inflation averages below the break-even rate, the fixed-rate bond will outperform the inflation-linked bond.The 10-year breakeven rate is about 1.63% as of August 31, 2015. Clearly the market is not expecting serious consumer price inflation for quite a long time. Yield Curve as of 2015-09-01  I created the above chart in StockCharts. The chart shows US treasury yields from 2 years to 30 years. 2- and 3-year yields have been rising very slowly since the beginning of 2013 in anticipation of Fed rate hikes. At the long end of the curve (30-year in red, 10-year in orange) rates made recent highs in late 2013 but are well below those highs now. Let's compare rates across the entire curve now compared to a year ago. US Treasury Yields Now vs. Year Ago  Thanks to Doug Short at Advisor Perspectives for help with the above chart. Note that between 6-months and 2-years, treasury yields are higher than they were a year ago. Meanwhile, from 5-years and out, rates are lower than they were a year ago. September Hike Ideal? Bloomberg has a curious article out today: One Reason Market Turmoil Might Actually Make September the Ideal Time to Hike Interest Rates. Torsten Slok, Deutsche Bank's chief U.S. economist, sees a silver lining in this market turmoil that he figures actually makes a September liftoff look more attractive.The Bloomberg article also mentions the "savings glut" thesis, a preposterous idea that I will rebut, in detail, later, in a separate post. Mish Rebuttal of Slok's View Other than general agreement over the unlikelihood of the long end spiking, Slok's reasoning seems flat out wrong. The flattening of the curve is generally not good for bank profits and also reflects increasing recession possibilities. A key reason the yield curve cannot invert now is the low end is at zero. Price in a couple hikes and portions of the yield curve could invert. That's what happened in Canada earlier this year following a surprise cut in rates by the Royal Bank of Canada. Canada Recession On January 31, Based on an inversion in parts of the yield curve, I correctly proclaimed Canada in Recession. Just yesterday, Canadian stats confirmed the recession. It remains to be seen if the US follows, but a flattening of the yield curve is not a good sign for growth. For further discussion, please see Canada in Recession with Two Consecutive Quarters of Negative Growth. How Big a Hike? The debate still rages "will they, won't they". The correct answer is "It won't matter at all". If the US does follow into recession, rest assured it will not be because of hike. With the global economy slowing rapidly, and with US equities and corporate bonds in huge bubbles, one hell of a payback is coming for the inane QE policies of this Fed. Bubbles of Increasing Amplitude Some defend the Fed, but I don't. As noted in Fed Apologist Ritholtz Interviews Fed Apologist McCulley, Fed policy is precisely what's behind destabilizing bubbles of increasing amplitude over time. Fed policy is also behind rising income inequality that Fed Chair Janet Yellen constantly whines about. Is the Bond Bull Market Over? Here's the question that's been on nearly everyone's mind for at least a decade: Is the Bond Bull Market Over. I have two answers: Yes, and Perhaps Not. Those answers are not contradictory. There are many bond bull markets to consider. Let's start with corporate bonds. Near-Junk Corporate Bull Market Over? Using Moody's Baa seasoned bonds as a good proxy for near-junk (the lowest investment grade bonds), let's take an even closer look at recent happenings.  The Moody's Baa seasoned bond yield hit an all-time low of 4.29% on January 30, 2015. It is now 5.36%. That's over a 100 basis point tightening (one full percentage point) in a mere seven months. I am willing to state that the bull market in near-junk bonds is finished.

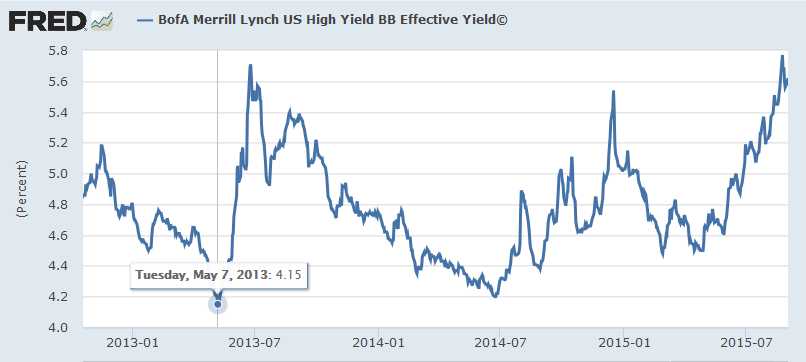

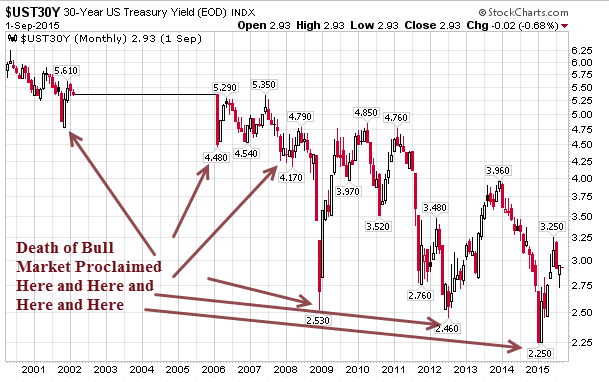

That "some point" appears to be now. The only question is how fast the air comes out of the enormous junk balloon. We have yet seen a slow release of air from a bubble. Will this be a first? Junk Bond Bull Market Over? Let's hone in on BB bonds, the top-tier on non-investment grade (junk) bonds.  In April of 2013, the BofA Merrill Lynch US High Yield BB Effective Yield© hit an all-time low yield of 4.31%. The effective yield is now 5.62%. That is a rise of 131 basis points (1.31 percentage points). And for the same reasons noted in the above Baa discussion, I declare the end of the junk bond bull market. Is the US Treasury Bull Market Over? This question is amusing. Here is a pair of charts that shows why. US 30-Year Bond Yield Monthly Chart  The "death" of the US treasury bull market has been proclaimed so many times it's difficult to show them all. Let's hone in further. US 30-Year Bond Yield Daily Chart  Where others saw massive price inflation coming (with the CPI as the determining measure), I called for deflation (as measured by credit marked to market and asset prices). In other words I expected monetary inflation to manifest itself in asset prices not consumer prices. I stick with that call. For all of those who think consumer price inflation is just around the corner, I have some questions. Questions for Inflationistas

Bonus question: With the long end of the curve just 70 basis points away from a record low, and with a global growth slowing, is it inconceivable for another record low at the long end of the curve? Is the Bond Bull Market Over?

By the way, junk bond bull markets and equity bull markets tend to go hand-in-hand. So do junk bond bear markets and equity bear markets. Feelin' Lucky? Link if video does not play: Dirty Harry. Question for the Fed: Do you have another bullet left in your gun if things head south, or not? "Well Do Ya Punk?" Mike "Mish" Shedlock |

| Beige Book Highlights: Will They or Won't They? Still Undecided? Posted: 02 Sep 2015 03:45 PM PDT The Fed's Beige Book is a summary and analysis of economic activity and conditions, issued roughly two weeks prior to monetary policy meetings of the Fed. "Book" is an adequate expression. This month, the Beige Book is 50 pages long. It's prepared with the aid of reports from the district Federal Reserve Banks. Don't bother reading the book. It's not worth the slog. Beige Book Highlights Bloomberg offers these Beige Book Highlights. The Beige Book, prepared for the September 17 FOMC meeting, is not underscoring any urgency for a rate hike. Eleven of 12 districts report only moderate to modest growth with the Cleveland district reporting only slight growth. This compares with 10 districts in the July Beige Book which reported moderate to modest growth. Most districts describe labor demand as no more than modest to moderate and most describe actual job growth as no better than slight or modest. But there are isolated areas of labor shortages and four districts report a rise in wages for specific industries. Inflation is described as stable with only slight upward pressure across districts.Will They or Won't They? It matters not whether the Fed hikes or not. Either way, bubbles have formed in equities and junk bonds. Tiny hikes will not cause a recession, and the bubbles are destined to pop anyway. In honor of the question, however, here's a musical tribute from the '40s, with thanks to reader Charles. Link if video does not play: Your "Undecided" Now What are You Going to Do? Mike "Mish" Shedlock |

| Canada in Recession with Two Consecutive Quarters of Negative Growth Posted: 02 Sep 2015 12:10 PM PDT Yesterday, Yahoo!News reported Canada Officially Enters Recession. Reeling from low oil prices, Canada fell into a recession in the first half of the year, government data confirmed Tuesday, putting Conservative Prime Minister Stephen Harper on the defensive in the run-up to October elections.Canada Recession Call Easy Unlike the US, where the Fed pegged short-term interest rates so low that the yield curve cannot invert, calling the Canadian recession was easy. On January 21, 2015 I wrote Canadian Recession Coming Up: Yield Curve Inverts Following Unexpected Rate Cut; Loonie at Six-Year Low. "Coming Up" happened quickly. On January 31, I wrote Canada in Recession, US Will Follow in 2015. Following the rate cut, the yield curve in Canada inverted out to three years. Inversion means near-term interest rates are higher than long-term rates.US Recession Call More Difficult With constantly huge GDP revisions in the US, and with a yield curve that cannot invert, it's much tougher calling US recessions. It remains to be seen if a US recession starts this year or not. Spectacular auto sales and modest home building have kept the economy trudging along. However, the US is not going to decouple from a slowing global economy forever. The idea is as silly as the 2008 notion that China would decouple from the US economy. Mike "Mish" Shedlock |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 1600 Amphitheatre Parkway, Mountain View, CA 94043, United States | |

No comments:

Post a Comment