Mish's Global Economic Trend Analysis |

- Ukraine Aftermath: Hunt for Yanukovich, Russia Denounces Interim Leaders, Documents Reveal Plans to Use Army on Civilians

- Germany at Heart of Europe's Political Predicament; Squaring the Circle; When is the Breaking Point?

- Monetarism, Abenomics, QE, and Minimum Wage Proposals: One Bad Idea Leads to Another, and Another

| Posted: 24 Feb 2014 04:30 PM PST Let's tie up some loose ends on Ukraine, even as much uncertainty remains. Documents Reveal Plans to Use Army on Civilians Financial Times: Papers reveal Yanukovich plans to turn army against protesters The Yanukovich regime had drawn up plans for a massive crackdown on protesters in Kiev using thousands of police and troops – and the chief of Ukraine's armed forces on Thursday last week ordered 2,500 army troops into the capital for an "antiterrorist" operation.Hunt for Yanukovich Financial Times: On the trail of Ukraine's missing Viktor Yanukovich Viktor Yanukovich's whereabouts remained unknown for a third day on Monday, as rumours swirled that Ukraine's deposed president was hiding out in Crimea, a pro-Moscow stronghold with easy water access to Russia via the Black Sea.Russia Denounces Interim Leaders Financial Times: Moscow takes aim at Ukraine's interim leaders and the west Russia denounced Ukraine's interim leaders as dictators on Monday and blasted the western governments that it said helped bring them to power, in a sign that the toppling of President Viktor Yanukovich is triggering a regional stand-off.Open House Financial Times: Open house at Yanukovich's fabled palace Ukrainians expressed shock and disgust as the full extent of Viktor Yanukovich's opulent lifestyle was revealed at the weekend.House Fit for a Tyrant Mail Online: House fit for a tyrant: Protestors storm the sprawling, luxury estate of Ukraine's fugitive president which has its own private zoo, golf course and is half the size of Monaco Mail Online has a series of images and videos. Here are a few images.     Many more pictures and videos on the site. It's amazing there was no destruction or looting. Cheers and best wishes to the citizens of Ukraine. Unfortunately, many problems linger. Election uncertainty and chants of "Russia, Russia" in Sevastopol could easily lead to further violence. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

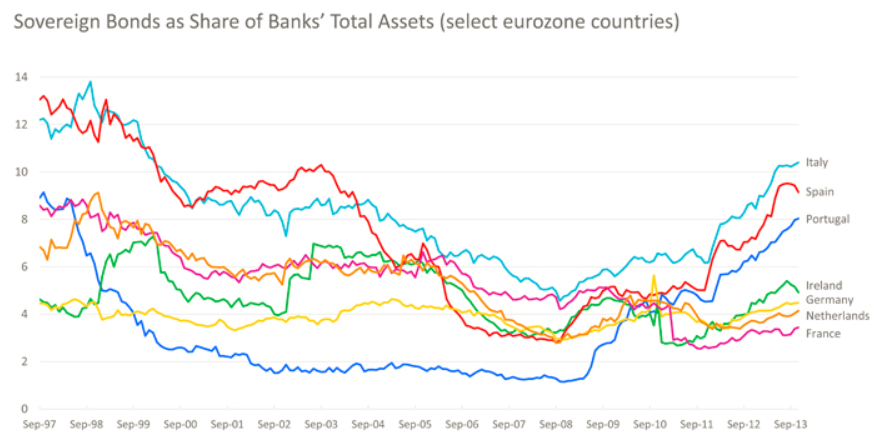

| Germany at Heart of Europe's Political Predicament; Squaring the Circle; When is the Breaking Point? Posted: 24 Feb 2014 12:20 PM PST Germany is at the heart of Europe's political predicament. Although the status quo cannot and will not work, there is no incentive to change. Germany's Constitutional Court has strengthened the Eurosceptics and eliminates further moves by Germany towards debt mutualization. Some think debt mutualization, eurobonds, and combined fiscal budgets are a good idea. Others, like myself, don't. Regardless, and as noted in Rethinking "Paper Tiger", those options remain off the table. What remains on the table are policies that fuel high unemployment and undermine living standards says Brigitte Granville in Poking the Eurozone Bear. Some take the sanguine view that the current "lie still" approach is adequate to ensure that the eurozone economy does more than avoid decline. From their perspective, Germany's decision over the last three years to permit actual and prospective transfers just large enough to prevent financial meltdown will somehow be enough to enable the eurozone finally to begin to recover from a half-decade of recession and stagnation.Germany's Pyrrhic Victory Also on Project Syndicate, please consider Germany's Pyrrhic Victory by Marcel Fratzscher. The German Constitutional Court has ruled against the European Central Bank's pledge to buy potentially unlimited quantities of distressed eurozone countries' government bonds, and has called on the European Court of Justice (ECJ) to confirm its decision. Until that happens, the "outright monetary transactions" (OMT) scheme is effectively dead, weakening the ECB's ability to act as an effective and credible financial-market backstop at a time when European governments remain unwilling to fill the void.When is the Breaking Point? Notice the silliness of Fratzscher's last statement. He begs for a viable and effective banking union, when it should be perfectly clear the German constitution court won't allow for one. Eventually something is going to break, and most likely at the worst possible time. Yet no one can say when. Meanwhile the imbalances continue to grow as complacency rules. Spain 10-Year Government Bond Yield  That decline in yield looks like a good thing. But it comes with a huge risk. Spain's banks have plowed more and more into its own bonds. When yields rise, those banks are going to be in a huge amount of pain. Here are some charts from Squaring the Circle. Sovereign Bonds Held by Domestic Banks  Sovereign Bonds Held by Domestic Banks as Percentage of Assets  As long as yields decline, there are no problems. The crisis will be even bigger than before if and when yields rise. When that happens is anyone's guess. That it will happen is a near certainty. One way or another Germany is going to pay a huge price. Theoretically, there are two solutions.

If Germany will not allow option number one, the only viable choice is option number two. It would behoove Germany and the eurozone to have this discussion. Instead, Merkel has her head in the sand. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Monetarism, Abenomics, QE, and Minimum Wage Proposals: One Bad Idea Leads to Another, and Another Posted: 24 Feb 2014 01:15 AM PST Telegraph writer Ambrose Evans-Pritchard is back at it. In arguably his worst article ever, Pritchard complains France is Looking Straight Down the Barrel of a Deflation Shock. Pritchard bemoans the horrors of falling prices and says "There is a technical solution to this. It is called QE. The European Central Bank can lift the entire EMU system off the reefs by launching a monetary blitz to meet its own M3 growth target of 4.5pc." Pritchard ignores the fact that equity prices are back in bubble land. He ignores the fact that QE did not bring inflation to Japan. He ignores the fact that consumers desperately need falling prices. He ignores the fact that falling consumer prices do not stop consumers from buying anything. Pritchard complains "French President François Hollande must now pay the price for kowtowing to the contraction polices of the eurozone." Pritchard knows full well France is bound by eurozone policies. The only way France cannot "kowtow to the contraction polices of the eurozone" is if France leaves the eurozone. But Pritchard never mentions that. Instead he whines about falling prices. One Centrally Bad Idea Pritchard clings to the centrally bad idea that falling consumer prices will cause consumers to perpetually delay purchases. In the real world, people have to eat. They have to buy gasoline for their cars. They have to buy clothes when they wear out. They have to heat their homes. Those are relatively inelastic demands. But there is also no evidence consumers will hold off for long on discretionary spending either. Every Christmas, shoppers line up for bargains. People continue to upgrade TVs, computers, monitors as they wear out, or simply because prices are lower and quality is up since they last bought. In other words, people buy when bargains are many and stop buying when bargains are few. Living Wages Pritchard's solution is the same as that of many charlatans before him: Force prices up. The Fed succeeded. As a result, people now bitch and moan about "living wages". Of course "living wages" are a moving target. Force prices higher and the more it takes to keep up with them. People want $15 an hour for standing behind a cash register and handing you a sack of the worst food money can buy. It's ridiculous. Hardly anyone ever points out the fact that wages have not kept up with inflation precisely because the Fed has done exactly what Pritchard wants. People do not blame the Fed, nor do they blame economic illiterates like Pritchard. Instead they blame allegedly evil corporations like McDonalds and Walmart. Actually, the world needs more Walmarts. I hope Walmart enters the health-care business in a big way. Costs would come down overnight. It would also be great if Walmart could directly compete with banks on financial services. Costs Rising Faster than Wages The problem is not that wages are too low, but rather costs rise faster than wages. Why does that happen? Because of the very central bank polices espoused by Monetarists like Pritchard. Pritchard and others will note that falling home prices will slow bank lending and consumer credit. That is correct. OK, but what's the real problem? The real problem is monetary inflation artificially jacked up the prices of assets (homes, cars, equities) upon which unsustainable loans were made. Rather than admitting that simple and obvious fact, Monetarists propose the solution is still more monetary printing which will do nothing but create even bigger asset bubbles. Brief History

Because of one idiotic notion, that "falling prices are a bad thing", the Fed has generally managed to keep the CPI rising, with some things going up much faster than others. In response to uneven price inflation, we have seen numerous "affordable housing" programs, massive student aid programs, bank bailouts at taxpayer expense, Obamacare to make medical insurance affordable, cash for clunkers, Abenomics in Japan, and countless other economic idiocies. People propose bad idea after bad idea simply to fix problems caused by the previous bad idea. This is corollary six to the Law of Bad Ideas. Law of Bad Ideas Corollary Six: Bad ideas lead to more bad ideas to fix problems caused by previous bad ideas. Pritchard, like many before him and countless others yet to come, want higher inflation rates. Here is a table I put together that shows the silliness of it all. Effect of Inflation Over Time

The above table shows what the price of something that costs $100 in year one will cost 49 years later at various inflation rates. None of these inflation charlatans discuss what happens if wages do not keep up. Nor do they discuss the incentives businesses have to outsource jobs or automate because of high wages. Amazingly, many people in academic wonderland are not satisfied with 2% annual inflation. They want 4% inflation or higher. For example, Laurence Ball at John Hopkins University claims to make a Case for Four Percent Inflation. Ball is "grateful for suggestions from Olivier Blanchard, Daniel Leigh, Gregory Mankiw, and Richard Miller. This paper is prepared for the Central Bank Review, published by the Central Bank of the Republic of Turkey." His paper was written in April 2013. How is the Turkish Lira doing since that paper came out? Let's take a look.  Hmm. Once inflation steps in it seems difficult to turn it off. Ball cited Gregory Mankiw, an economic professor at Harvard, who had an even more inane idea of drawing a number out of the hat every year and making currency ending in that digit worthless. The effect would be 10% price inflation and lord only knows what asset price inflation would occur were Makniw to get his way. Mankiw claims expiring currency would be a benefit. I responded Time For Mankiw To Resign These charlatans sit in their academic ivory towers void of common sense and real world economics. Of course economically asinine proposals from those in academic wonderland is expected behavior by corollary number four. For the sake of completeness, here is a complete recap. Law of Bad Ideas: Bad ideas don't go away until they have been tried and failed multiple times, and generally not even then. Corollary One: Left alone, bad ideas get worse over time. Corollary Two: The overwhelming desire to implement bad ideas leads to compromises guaranteed to make things worse. Corollary Three: Those in positions of political power not only have the worst ideas, they also have the means to see those ideas are implemented. Corollary Four: The worse the idea, the more likely it is to be embraced by academia and political opportunists. Corollary Five: No politically acceptable idea is so bad it cannot be made worse. Corollary Six: Bad ideas lead to more bad ideas to fix problems caused by previous bad ideas. Although there is strong evidence that consumers will hold off making asset purchases (homes, stocks, bonds), when asset prices fall, there is not a shred of evidence of a meaningful reduction in consumer purchases due to falling consumer prices. The irony is that QE tends to foster asset bubbles that ultimately crash, not a price rise in general goods. Central banks in general, and the Fed in particular, are excellent examples of those in power, hell bent on implementing various bad ideas. For further discussion please see Deflation Theory Reality Check. Also see Bubblicious Questions: What Causes Economic Bubbles? When Do Bubbles Burst? Can the Fed Prevent Bubbles? In yet another irony in this madness, monetarist polices benefit those with first access to money, namely the banks and the already wealthy. Yet the same academics screaming for higher inflation are typically the same ones screaming about income inequality. The amount of damage caused by one central thesis "falling prices are a bad thing" is staggering. And to fix problems inherent in that central thesis, countless other bad ideas are sure to follow. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment