| Is Chicago Mayor Rahm Emanuel a Friend of Taxpayers or Businesses? Or is Chicago Like France? Posted: 18 Feb 2014 07:13 PM PST Inquiring minds just may be wondering " Is Chicago Mayor Rahm Emanuel a Friend of Taxpayers or Businesses?" In case you are wondering, please consider what Illinois Policy Institute writer Jacob Huebert says via email. Chicago Mayor Rahm Emanuel recently proposed an ordinance that would regulate popular ride-sharing services such as Uber and Lyft in Chicago.

Emanuel often claims that he wants Chicago to be friendly to new businesses, innovation and technology. Unfortunately, his proposal is anything but friendly to these "transportation network" services, and would force them to either severely change the way they operate or leave the city entirely.

Where other cities have changed their laws to accommodate these new services, Chicago appears determined to continue using the law to protect established taxi companies from competition at everyone else's expense.

Here are seven of the proposal's worst anticompetitive features.

1. Ride-share companies can't own vehicles – or help drivers buy them

One provision of the ordinance says that the operator of a ride-share service cannot "own, provide financing for the obtaining, leasing, or ownership of, or have a beneficial interest in transportation network vehicles."

As it stands, neither Uber nor Lyft actually owns any cars or employs any drivers – they just bring drivers and passengers together. But who's to say some future entrepreneur won't find a way to make it economical for the "network" to also own vehicles or help its drivers buy them? And how does preemptively banning this help the public? In fact, it doesn't do anything for the public; it's just a way to stop ride-sharing companies from finding new ways to outcompete established taxicab companies.

2. No taxis allowed

Currently you can use Uber to summon three types of vehicles: black luxury cars, taxis and budget "UberX" cars. The taxis you can hail with Uber are normal, licensed Chicago cabs, and drivers have signed up to participate; it's no different from calling for a cab by telephone or flagging one down on the street, except that it's much more convenient.

The proposed ordinance would eliminate the taxi option for Uber customers by prohibiting taxis from participating in licensed transportation networks. How that could possibly benefit the public is a mystery. If the city adopts this rule, it will be destroying something that makes everyone's lives easier for no good reason.

3. No advertising

Under the ordinance, advertisements wouldn't be allowed on the inside or outside of vehicles. In the short term, that might not matter because, as things stand, Uber black cars, UberX cars and Lyft cars don't have any ads in them or on them; only taxis have ads.

But maybe Uber, Lyft or a future service will want its cars to have ads. And maybe some customers wouldn't mind seeing ads, especially if it meant cheaper fares.

Apparently the city wants to give taxis a monopoly on the vehicle-advertising business. That not only doesn't serve a legitimate governmental purpose; but it also violates the First Amendment.

4. No airport drop-offs

Uber and Lyft cars already aren't allowed to make airport pickups. Under the new ordinance, they wouldn't be allowed to drop off passengers, either. This, of course, serves no purpose except to protect taxi companies from competition.

5. No time-and-distance pricing

Perhaps the proposal's worst feature is that it would prohibit Uber and Lyft cars from charging passengers based on "a combination of distance travelled and time elapsed during service," which is how they charge customers now. Instead, the cars would have to charge a prearranged flat fee or charge customers based on either time or distance – but not both.

That's nonsensical. It's only rational to charge customers based both on time and distance, because both affect the driver's costs, and there's no way to account for traffic conditions in advance. That's why taxis charge based on both time and distance – and it's why taxi companies don't want Uber and Lyft to be able to use this method for charging customers.

6. Mandatory emblems

The ordinance would also require all cars in a given network to have an "emblem" on the outside of their car to identify which network they're in. Lyft already does this with its cars' pink mustaches. Uber, however, doesn't – and its black cars' logo-free appearance is part of what gives Uber cars their distinct cool, classy vibe.

Forcing Uber to add a logo serves no legitimate purpose. Customers don't need a logo to identify their Uber car for several obvious reasons: (1) the Uber app shows them their driver's name and picture, along with the car's license plate number; (2) the Uber app lets the customer see where the car is on a map when it's on its way and when it arrives; and (3) Uber drivers identify themselves upon arrival and confirm that they have the correct passenger.

So the only purpose of this requirement is to make Uber cars a little less special – that is, once again, to hamper competition for the taxi companies' benefit.

7. Big Brother-style GPS tracking

The ordinance would also require the networks to allow the city to monitor all of their vehicles at all times by GPS. But the city has no legitimate need to know where every Uber or Lyft driver is at all times – let alone where their passengers go. If the city needs particular GPS information for a law-enforcement purpose – if, say, a car was implicated in a crime – it can always get a warrant for that data.

Citizens should be disturbed by this invasion of privacy, which violates the Fourth Amendment's protection against unreasonable searches and seizures.

Citizens should also be disturbed by a city government that's more concerned about pleasing a politically connected special-interest group than in letting consumers choose the services they like best. And they should be disturbed that government officials are more interested in continuing cronyism for as long as possible than in letting Chicago thrive in the 21st century.

Chicagoans should demand that city officials either remove these features from the proposed ordinance or, better yet, scrap it entirely and replace it with one that simply declares that these transportation services are legal and may continue operating as they have been.

Jacob Huebert

Senior Attorney

Liberty Justice Center Is Chicago Like France?Unfortunately, the answer is yes, if not worse. For sake of comparison, please consider the New Law in France: Limos Must Wait 15 Minutes Minimum Before Picking Up RidesTo explicitly answer my lead question, Mayor Rahm Emanuel is no Friend of Taxpayers. Rather Emanuel is a friend of political cronies who undoubtedly contribute to his election campaign. But hey: Chicago is the "City that Works". The question is "For Whom?" Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Have an E Series Savings Bond? If So, It's No Longer Paying Interest; $16 Billion in Bonds No Longer Pay Interest Posted: 18 Feb 2014 06:04 PM PST I am not sure if any Mish readers have savings bonds, but undoubtedly some friends of Mish readers do. For those who do, here is a public service announcement: Nearly 47 Million U.S. Savings Bonds Worth Approximately $16 Billion No Longer Earn Any InterestNearly 47 million U.S. Savings Bonds worth approximately $16 billion have reached final maturity and are no longer earning any interest.

Most paper Series E, EE and I Savings Bonds have a 30-year life. Some Series E bonds, which were issued through November 1965, had a 40-year maturity period. All Series E bonds have reached final maturity and have stopped earning interest.

"It's not unusual for people to forget about bonds that were purchased 20, 30, 40 or more years ago," says Jackie Brahney, Marketing Director for SavingsBonds.com. She adds, "Many bond owners purchased the investment for retirement or education purposes and stored them away, but they don't understand how the bonds work."

Bond investors are often unaware of what their bonds are currently worth, interest rate performance, or when they will stop earning interest. Unfortunately, many believe that bonds will only be worth the amount that is printed on the front of them (aka face value), which is considered the initial maturity date. EE bonds will continue earning interest beyond their initial maturity date until they reach their final maturity. Final maturity is when a bond will no longer earn any interest. If you happen to have savings bonds or know of someone who does, please pass on this announcement. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Hollande Promises Tax Harmonization in Six Years if Foreign Businesses Invest in France Now Posted: 18 Feb 2014 01:15 PM PST French president Francois Hollande is seriously deranged if he expects businesses to take him up on his latest offer to Invest in France Now, See Harmonization in Six Years. Hosting 30 heads of French units of foreign companies at his Elysee Palace, President Francois Hollande pledged to guarantee that taxes on an investment would not rise later - as has happened in the past - and VAT and duty rules for firms would be streamlined this year.

The Socialist president, who last month announced France would phase out 30 billion euros (24 billion pounds) in charges on companies by 2017 to reverse its slide in trade competitiveness, also said French business taxes would be harmonised with those of its neighbours, especially Germany, by 2020.

"A business, whether French or foreign, that wants to invest will have a commitment from the administration that the tax rules will remain the same, and that will be a guarantee." Skepticism Runs HighSkepticism runs high according to a survey by pollster Opinionway of heads of 253 companies whose revenue grew more than 15 percent in the past three years. - Nine out of 10 chief executives of firms exhibiting strong growth did not believe the government could boost economic output or help their companies become more competitive.

- Eighty-nine percent did not consider Hollande able to reduce public spending.

The article notes that Hollande's promise came the same day as a new law was introduced in parliament to impose tough fines on firms that shut operations still deemed economically viable.

The law was prompted by Hollande's 2012 campaign promise to steelworkers at ArcelorMittal's Florange blast furnaces in northern France that he would pass legislation to protect their jobs in case of a shutdown. Despite a government threat to nationalise them, the furnaces were later closed.

Hollande did not give businesses any reason he could be trusted. Nor did he say how he would meet his "guarantee". Please note there is no legal basis for his promise. He wants 6 more years just to get to the break-even point in competitiveness, but he will be gone by 2020 anyway. This man is completely clueless about two things - What needs to be done

- When it needs to happen

Here's a hint Mr. President: 2020 is not even in the ballpark. Besides, no one believes you can even do that! Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

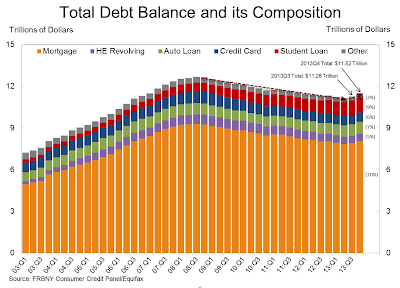

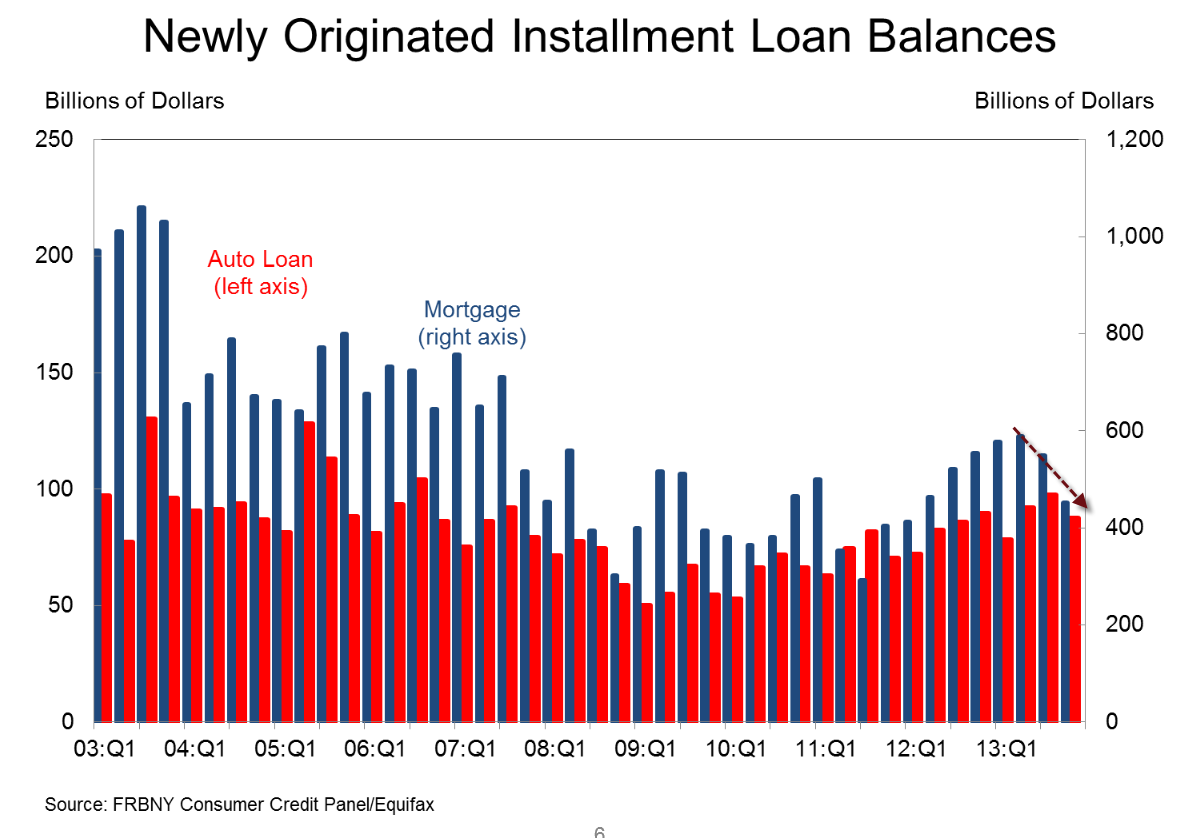

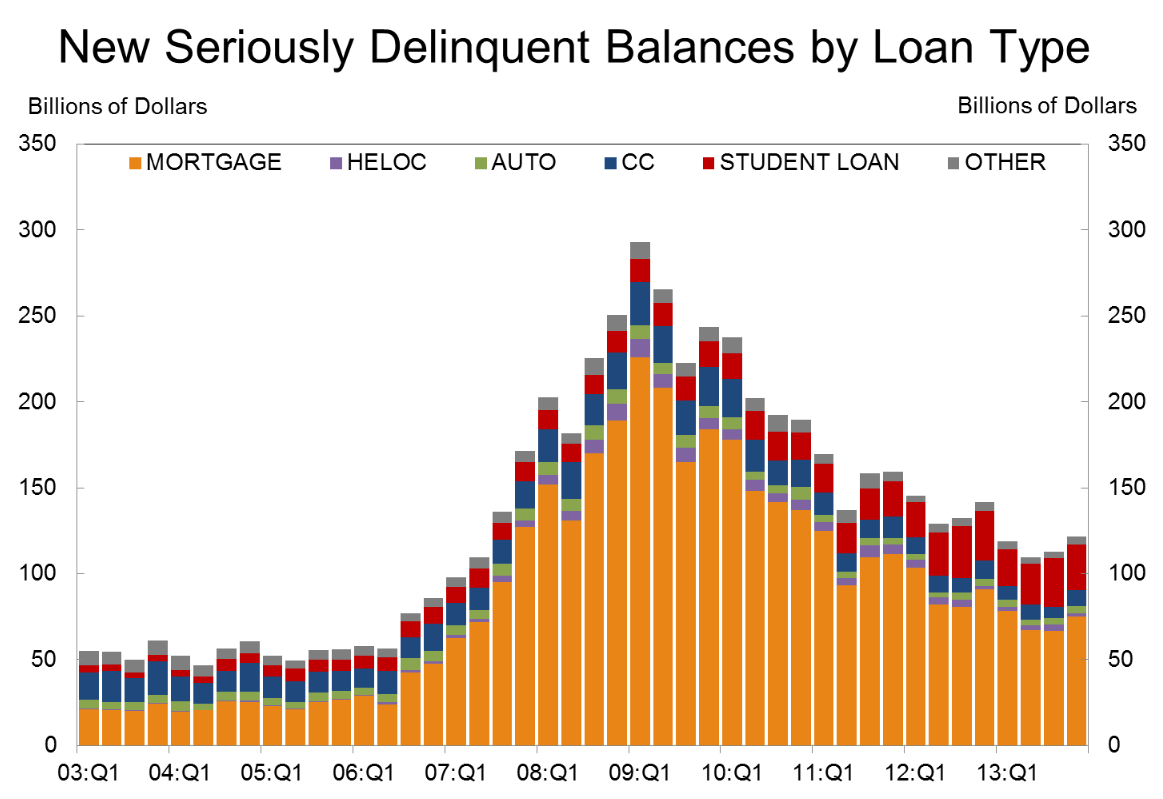

| US Household Debt Climbs by Most Since 2007, Mortgage Debt Leads the Way; Annually Student Debt and Autos Lead the Way Posted: 18 Feb 2014 11:31 AM PST Given stagnant wages and higher taxes, the only way households can increase spending is to go further into debt. The New York Fed quarterly report on Household Debt and Credit shows that is what happened. Aggregate consumer debt increased in the fourth quarter by $241 billion, the largest quarter to quarter increase seen since the third quarter of 2007. As of December 31, 2013, total consumer indebtedness was $11. 52 trillion, up by 2.1% from its level in the third quarter of 2013. The four quarters ending on December 31, 2013 were the first since late 2008 to register an increase ($180 billion or 1.6%) in total debt outstanding. Nonetheless, overall consumer debt remains 9.1 % below its 2008Q3 peak of $12.68 trillion.

Mortgages, the largest component of household debt, increased 1.9% during the fourth quarter of 2013. Mortgage balances shown on consumer credit reports stand at $8.05 trillion, up by $152 billion from their level in the third quarter. Furthermore, calendar year 2013 saw a net increase of $16 billion in mortgage balances, ending the four year streak of year over year declines. Balances on home equity lines of credit (HELOC) dropped by $6 billion (1.1%) and now stand at $529 billion. Non-housing debt balances increased by 3.3 %, with gains of $ 18 billion in auto loan balances, $53 billion in student loan balances, and $11 billion in credit card balances.

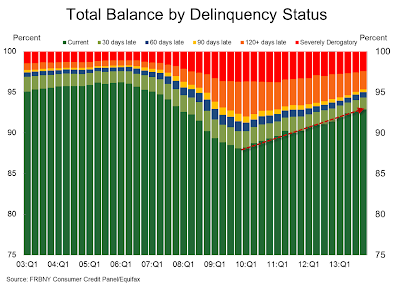

Delinquency rates improved for most loan types in 2013 Q4. As of December 31, 7.1% of outstanding debt was in some stage of delinquency, compared with 7.4% in 2013 Q3. About $820 billion of debt is delinquent, with $580 billion seriously delinquent (at least 90 days late or "severely derogatory"). Housing Debt - Originations, which we measure as appearances of new mortgage balances on consumer credit reports, dropped again, to $452 billion.

- About 157,000 individuals had a new foreclosure notation added to their credit reports between October 1 and December 31.

- Foreclosures have been on a declining trend since the second quarter of 2009 and are now at the lowest levels seen since the end of 2005.

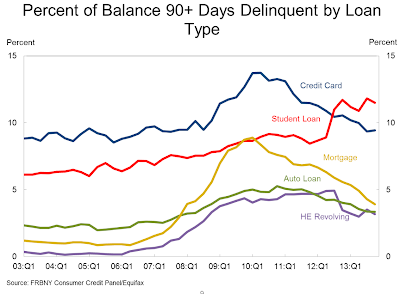

- Mortgage delinquency rates have seen consistent improvements; 3.9% of mortgage balances were 90+ days delinquent during 2013Q4, compared to 4.3% in the previous quarter.

- Serious delinquency rates on Home Equity Lines of Credit decreased to 3.2%, down from 3.5% in 2013Q3.

Student Loans and Credit Cards - Outstanding student loan balances reported on credit reports increased to $1.08 trillion (+$53 billion) as of December 31, 2013, representing a $114 billion increase for 2013.

- About 11.5% of student loan balances are 90+ days delinquent or in default.

- Balances on credit cards accounts increased by $11 billion.

- The 90+ day delinquency rate on credit card balances increased slightly to 9.5%.

Auto Loans and Inquiries - Auto loan originations decreased in the fourth quarter of 2013 to $88 billion.

- The percentage of auto loan debt that is 90 + days delinquent remains unchanged at 3.4%.

- The number of credit inquiries within six months – an indicator of consumer credit demand – remained virtually unchanged from the previous quarter at 169 million.

Total Debt Quarterly and Annual Changes Quarterly and Annual Changes  Annual Changes Annual Changes- Student loans accounted for $114 billion, 63.33% of the overall increase

- Auto loans accounted for $80 billion, 44.44% of the overall increase

- Combined, student loans and auto debt account for $191 billion, 107.78% of the overall increase

Quarterly Changes - Mortgage debt accounted for $152 billion, 63.07% of the overall increase

- Student loans accounted for $53 billion, 21.99% of the overall increase

- Combined, mortgage debt and student loans account for $205 billion, 85.06% of the overall increase

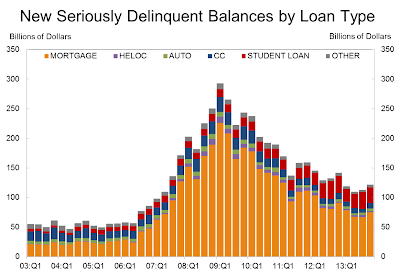

Clearly fourth quarter of 2013 was a big quarter for housing, but can it last? Auto loans had an average quarter, likely downhill from here. Trends in student debt are ominous. Newly Originated Installment Loan Balances Growth in auto loans and home installment loans appears to have peaked. Delinquency Status Percent of Delinquencies by Type Percent of Delinquencies by Type New Delinquent Balances by Loan Type New Delinquent Balances by Loan Type Seriously Delinquent Balances by Loan Type Seriously Delinquent Balances by Loan Type There are 31 pages and many other charts in the report. Inquiring minds may wish to take a look. Some big cracks beginning to appear? Sure looks like it. Unless job growth and wage growth pick up, especially wage growth for the bottom half, these trends may be as good as they get given the noticeable cracks and ominous trends in student loan debt. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| China Fooled the World (But It Cannot Last) Posted: 17 Feb 2014 11:16 PM PST Steen Jakobsen, chief economist at Saxo Bank emailed a pair of interesting links on the explosion of investment and debt in China. First consider the BBC report How China Fooled the World by Robert Peston. Robert Peston travels to China to investigate how this mighty economic giant could actually be in serious trouble. China is now the second largest economy in the world and for the last 30 years China's economy has been growing at an astonishing rate. While Britain has been in the grip of the worst recession in a generation, China's economic miracle has wowed the world.

Now, for BBC Two's award-winning strand This World, Peston reveals what has actually happened inside China since the economic collapse in the west in 2008. It is a story of spending and investment on a scale never seen before in human history - 30 new airports, 26,000 miles of motorways and a new skyscraper every five days have been built in China in the last five years. But, in a situation eerily reminiscent of what has happened in the west, the vast majority of it has been built on credit. This has now left the Chinese economy with huge debts and questions over whether much of the money can ever be paid back.

Interviewing key players including the former American treasury secretary Henry Paulson, Lord Adair Turner, former chairman of the FSA, and Charlene Chu, a leading Chinese banking analyst, Robert Peston reveals how China's extraordinary spending has left the country with levels of debt that many believe can only end in an economic crash with untold consequences for us all. Will China Shake the World Again?In part two of the series by Peston (both links are promos for the BBC video that will play Tuesday), please consider Will China Shake the World Again?Perhaps the big point of the film I have made, to be screened on Tuesday (How China Fooled the World, BBC2, 9pm) is that the economic slowdown evident in China, coupled with recent manifestations of tension in its financial markets, can be seen as the third wave of the global financial crisis which began in 2007-08 (the first wave was the Wall Street and City debacle of 2007-08; the second was the eurozone crisis).

Why do I say that?

Well in the autumn of 2008, after the collapse of Lehman, there was a sudden and dramatic shrinkage of world trade. And that was catastrophic for China, whose growth was largely generated by exporting to the rich West all that stuff we craved. When our economies went bust, we stopped buying - and almost overnight, factories turned off the power, all over China.

I visited China at the time and witnessed mobs of poor migrant workers packing all their possessions, including infants, on their backs and heading back to their villages. It was alarming for the government, and threatened to smash the implicit contract between the ruling Communist Party and Chinese people - namely, that they give up their democratic rights in order to become richer.

So with encouragement from the US government (we interviewed the then US Treasury Secretary, Hank Paulson), the Chinese government unleashed a stimulus programme of mammoth scale: £400bn of direct government spending, and an instruction to the state-owned banks to "open their wallets" and lend as if there were no tomorrow.

Which, in one sense, worked. While the economies of much of the rich West and Japan stagnated, boom times returned to China - growth accelerated back to the remarkable 10% annual rate that the country had enjoyed for 30 years.

But the sources of growth changed in an important way, and would always have a limited life.

Toxic investment

There are two ways of seeing this.

First, even before the great stimulus, China was investing at a faster rate than almost any big country in history.

Before the crash, investment was the equivalent of about 40% of GDP, around three times the rate in most developed countries and significantly greater even than what Japan invested during its development phase - which preceded its bust of the early 1990s.

After the crash, thanks to the stimulus and the unleashing of all that construction, investment surged to an unprecedented 50% of GDP, where it has more or less stayed.

Here is the thing: when a big economy is investing at that pace to generate wealth and jobs, it is a racing certainty that much of it will never generate an economic return, that the investment is way beyond what rational decision-making would have produced.

But what makes much of the spending and investment toxic is the way it was financed: there has been an explosion of lending. China's debts as a share of GDP have been rising at a very rapid rate of around 15% of GDP, or national output, annually and have increased since 2008 from around 125% of GDP to 200%.

"Most people are aware we've had a credit boom in China but they don't know the scale. At the beginning of all of this in 2008, the Chinese banking sector was roughly $10 trillion in size. Right now it's in the order of $24 to $25 trillion.

"That incremental increase of $14 to $15 trillion is the equivalent of the entire size of the US commercial banking sector, which took more than a century to build. So that means China will have replicated the entire US system in the span of half a decade."

There are no exceptions to the lessons of financial history: lending at that rate leads to debtors unable to meet their obligations, and to large losses for creditors; the question is not whether this will happen but when, and on what scale. Wine Country Conference IIWant to hear a live discussion of what Steen Jakobsen thinks about Europe and China? Then come to the second annual Wine Country Conference which will be held May 1st & 2nd, 2014. We have an exciting lineup of speakers for this year's conference. - John Hussman: Founder of Hussman Funds, Director of the John P. Hussman Foundation which is dedicated to providing life-changing assistance through medical research

- Steen Jakobsen: Chief Economist of Saxo Bank

- Stephanie Pomboy: Founder of MacroMavens macroeconomic research

- David Stockman: Ronald Reagan's budget director, best-selling author, former Managing Director of The Blackstone Group

- Mebane Faber: Co-founder and the Chief Investment Officer of Cambria Investment Management

- Jim Bruce: Producer, Director, and Writer of Money For Nothing: Inside the Federal Reserve

- Chris Martenson: Reknown speaker and founder of Peak Prosperity

- Mike "Mish" Shedlock: Investment advisor for Sitka Pacific and Founder of Mish's Global Economic Trend Analysis

In addition, we expect confirmation from a number of other highly respected fund managers and speakers. This year's event is two days and will include additional "break-out" groups. For speaker bios, please check out Wine Country Conference Speakers. This Year's Cause: Autism$100,000 of the money raised last year came from a generous matching grant from the John P. Hussman Foundation. Some of us in the industry who have done well are making an effort to help others. John Hussman is at the very top of that list. One of John's kids has severe autism. This year, all net proceeds will go to support autism programs. Conference DetailsFor further details about the 2014 conference, please see Wine Country Conference May 1st & 2nd, 2014Nothing Like It!This event is not just another "come and hear someone talk" kind of thing. Attendees and their significant others can expect an educational, fun, and relaxed time. Last conference, we arranged wine tours. They were a big hit. We will do so again. One of the wine estates we visited had a Bocce Ball court. On a couple of miracle shots, I won both games I played. Stay an extra day and golf or travel. I did. The conference hotel is a fun place in and of itself. Unlike many other conferences, you will have easy access to speakers. Want to chat with me, Steen, John, or anyone else at the conference? You will have an easy chance. Not only do we have an excellent lineup of speakers, you will have an opportunity to meet with them, have intimate discussions on important investment topics, with a lot of fun on the side, including wine tours and great wine. There's nothing like it in the investment business. And your money goes to a great cause! What can be better?  Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

No comments:

Post a Comment