Mish's Global Economic Trend Analysis |

- Fiscal Crisis in Chicago: Pensions 31% Funded, Moody's Downgrades Debt 3 Notches, Pension Liability is $61,000 Per Household; Mish's Proposed Solutions

- Grand Coalition or Grand Discontent, Mistrust and Disrespect? Political Poker Revisited

- M1 Money Supply vs. Real GDP

| Posted: 17 Sep 2013 01:27 PM PDT Move over Detroit. The fiscal crisis in Chicago is far bigger.

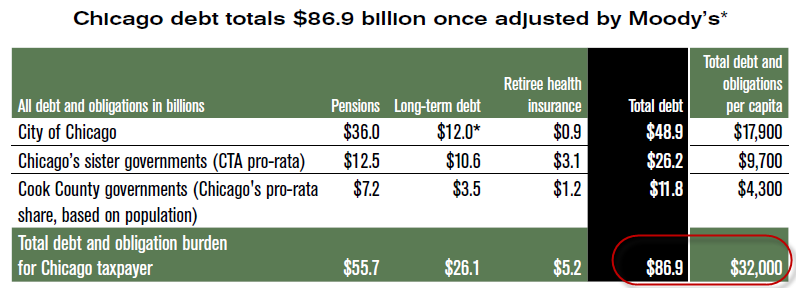

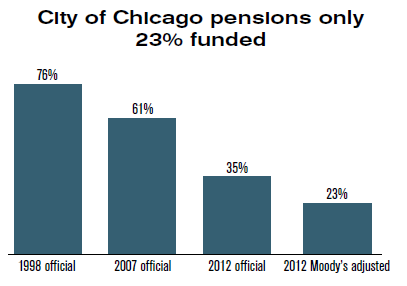

Via email, Ted Dabrowski at the Illinois Policy Center writes ... While all eyes are focused on a solution for Illinois' state-run pension systems, Chicago's own debt crisis is looming.The Hidden Bill You can view the entire report at The hidden bill: Chicago taxpayers and the looming crisis. A closer look at the "Hidden Bill" shows the problem is even worse than stated by Dabrowski above. Pension funds have long assumed unrealistically high investment returns, which make the funds look healthier than they actually are. Moody's Investors Service now calculates unfunded pension liabilities using more appropriate discount rates.If you adjust pension obligations for a more realistic rate of return, the problem looks like this. Chicago Obligations  Chicago Pension Funding  Four Long Term Solutions

The above long-term solutions will stop the problem from growing as well as ensure labor costs are market-priced, not union-priced. I wish that was enough but it isn't. Those things will slow the rate of growth of the problem, but cannot address 77% pension underfunding. Two Short Term Solution

Pension and benefit cuts are necessary, but how best to do it? I propose the burden of pension cuts spread out in an equitable manner with those receiving the highest benefits taking the biggest percentage cuts. All pension income above a certain cap could be taxed at a very high rate. This would protect the smaller pensioners from massive haircuts. The alternative, as we saw in Central Falls, Rhode Island Bankruptcy, was an across the board 50% pension haircut. Someone with a $200,000 pension had it cut to $100,000. Someone with a $25,000 pension had it cut to $12,500. My proposal would cap the top-end rather than applying uniform haircuts. If one picks the cap carefully, a majority of union members would fare better under my plan than bankruptcy. The Union Choice Public unions can scream all they want, but the entire defined benefit pension system is insolvent. There is no choice other than pension haircuts. There is a choice as to how:

Bankruptcy Here We Come Unfortunately, unions are highly unlikely to accept my common sense proposal. Ultimately, Chicago will play around with superficial remedies just like Central Falls, Detroit, and several cities in California (all of which succumbed to the inevitable). In the meantime, Chicago will probably follow some other major cities into bankruptcy, such as Oakland and Los Angeles. Investors better pick their municipal bonds carefully, because some major hits are on the way. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Grand Coalition or Grand Discontent, Mistrust and Disrespect? Political Poker Revisited Posted: 17 Sep 2013 11:44 AM PDT After saying "nein" to a grand black-red CDU/CSU + SPD coalition led by CDU (Angela Merkel), SPD party candidate Peer Steinbrück changed his mind and said he was willing to form such a coalition. Political Poker Revisited I discussed the reasons for the switch in Political Poker in Germany. Was Steinbrück lying then, or now? Or both? Is this a game to win votes? Or a real change of heart? Or no change of heart, just a lie the entire time?Grand Coalition or Grand Opposition? Today, Der Spiegel discussed the power play in Possible SPD coalition with Merkel: Gabriel's power issue. The translation is particularly difficult, but this is what I have. Here Steinbrück, There Steinbrück, Everywhere SteinbrückGrand Coalition or Grand Discontent, Mistrust and Disrespect? Reader Bernd, who sent me the above link wrote... Hello Mish,Grand Coalition More Complicated Than It Looks Everything is more complicated than it looks. If a "Grand Coalition" is in the works, don't expect it to be very stable. And this is why CDU/CSU hopes to attain a majority without depending on any alliances. If AfD and FDP do not make the 5% threshold, CDU/CSU can get an outright majority. But if AfD totals 7% or more it is going to be very difficult if not impossible. CDU/CSU will then have to form a coalition with someone. What poison will it be? Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

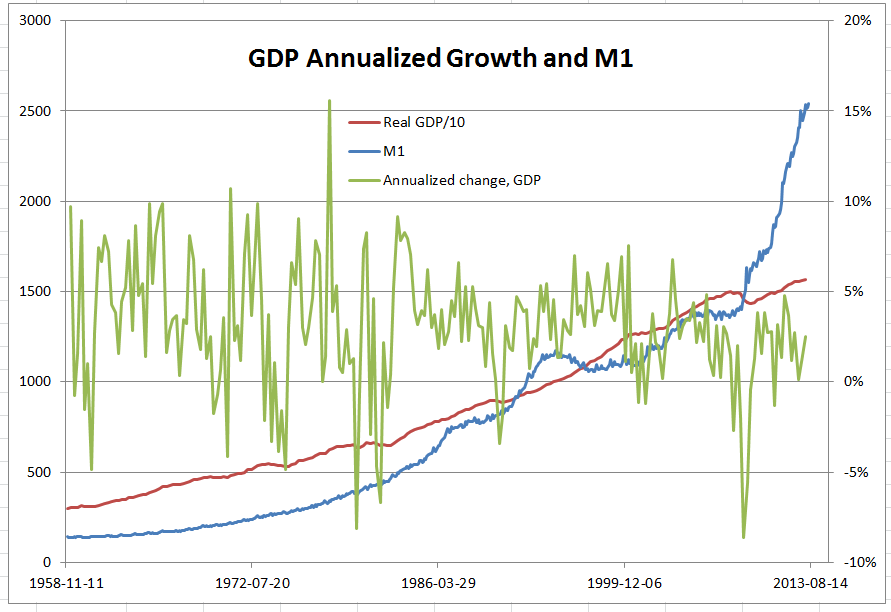

| Posted: 17 Sep 2013 02:13 AM PDT Here are a few interesting charts of M1 money supply vs. Real GDP/10 from reader WendyBG. Data M1 consists of: (1) currency outside the U.S. Treasury, Federal reserve Banks, and the vaults of depository institutions; (2) traveler's checks of nonbank issuers; (3) demand deposits; and (4) other checkable deposits (OCDs), which consist primarily of negotiable order of withdrawal (NOW) accounts at depository institutions and credit union share draft accounts. Click on any chart to see a sharper image. M1 vs. Real GDP/10 1959-Present  M1 vs. Real GDP/10 2000-Present  M1 vs. Annualized Change in Real GDP  The third chart shows annualized change in GDP vs. M1. Increases in M1 no longer have the same effect on growth or jobs. M1 as Percentage of GDP  M1 money supply has increased under Bernanke at a faster pace than ever before relative to GDP. I will take a look at GDP vs. other money supply measures later this week. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment