Mish's Global Economic Trend Analysis |

- France Private Sector Implosion Continues

- Another Warning Call for Depositors! Bank of Spain Says Spanish Banks Need €10bn More Loan Loss Provisions; Mish Asks €10bn or €100bn?

- Christine Lagarde, Head of IMF, In Court Facing Questions on Embezzlement and Fraud

- Japanese Bond Rout Continues; BoJ Vows to Curb Bond Turbulence; Curbing Turbulence is Theoretically Easy

- Nikkei Plunges 1,143 Points (7.32%); Global Equities Hammered; Start of Reflation Bubble Bust?

| France Private Sector Implosion Continues Posted: 23 May 2013 10:36 PM PDT Here's some news that caught my eye earlier today when I was on the road: The Markit Flash France PMI® shows French private sector output continues to fall at marked rate in May. Key points:Mish Comments Scores below 50 designate contraction, and scores in the 44-range designate substantial contraction, so those 9-month highs just go to show how awful conditions are. With French president Francois Hollande at the helm of France, and the nannycrats in Brussels in control elsewhere, don't expect conditions to get much better any time soon. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Posted: 23 May 2013 12:34 PM PDT Here's an optimistic headline on the Financial Times that could easily be off by a factor of 10 or more: Spain's banks need €10bn more provisions. Spanish banks will need to put aside extra provisions of up to €10bn to cover loans that borrowers will struggle to repay, according to an internal estimate by the Bank of Spain.€10bn or €100bn? Banks rolled over €200bn of loans because they could not pay debt on time, pretending the loans were current, and the Bank of Spain estimates the risk at a mere €10bn. Who do they think they are they fooling? Will 70% of those loans be paid back? 50%? 20%? I don't know but I strongly suggest it sure will not be 95%. Given the perpetual over-optimism on Spanish bank losses, I estimate there is a 0% chance the losses on this disclosure will be as little as €10bn. That said, I do not know what the existing loan loss provisions are, but if they are high enough (extremely doubtful), then there is some chance the losses will be on the order of €30bn or so (on the general principle things are typically 300% worse than the optimistic scenario). This does not factor in losses on Spanish government bonds when Spain eventually seeks a massive bailout. Realistically, Spanish banks are insolvent. Another Warning Call! By the way, this is yet another warning call "If you have money in Spanish banks, move it somewhere else immediately!" Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Christine Lagarde, Head of IMF, In Court Facing Questions on Embezzlement and Fraud Posted: 23 May 2013 10:47 AM PDT Christine Lagarde, head of the IMF, is in court today addressing her role in a $366 million payout to Bernard Tapie, a close friend of former president Nicolas Sarkozy who was also Lagarde's boss at the time. Lagarde was Sarkozy's finance minister. Reuters reports IMF's Lagarde in court for French arbitration case. IMF chief Christine Lagarde was questioned in court by French magistrates on Thursday over her role in a 285-million-euro ($366 million) arbitration payment made to a supporter of former president Nicolas Sarkozy.If Lagarde is formally charged with embezzlement or fraud, she may be asked to resign as head of IMF whether she is convicted or not. It's difficult to say how much of this is political maneuvering by current French president Francois Hollande, but it's equally difficult to dismiss the charges outright. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

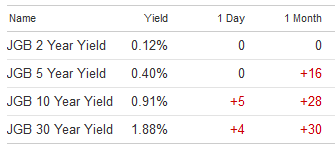

| Posted: 23 May 2013 08:42 AM PDT Curve Watchers Anonymous has been watching a major selloff in Japanese bonds. Here are a couple charts to consider. 10-Year Japanese Government Bond Yield  5-Year Japanese Government Bond Yield  Since March 4, the 5-year yield has gone from 0.1% to 0.43%. Although a mere .33 percentage points, the move represents a 330% percent rise in in yield. One Month Changes  Charts courtesy of Bloomberg Note: Those charts were snapshots taken last evening. This morning, yields have settled down, for now. Bank of Japan Vows to Curb Bond Turbulence NewsDay reports Bank of Japan vows market steps to curb bond turbulence The Bank of Japan vowed yesterday to take necessary steps to reduce volatility in bond markets that has threatened to jeopardise the government's fight to end deflation and revive growth.No Impact "Yet" In absolute terms there is not much impact, yet. However, I put an emphasis on the word "yet", a word Kuroda conveniently left out. Curbing Turbulence is Theoretically Easy It's theoritically easy to curb turbulence. Central banks can in fact control any single economic variable they want such as interest rates, money supply, or even the price of gold. To control bond turbulence, all the Bank of Japan has to do is corner the market. To do so would be quite similar to the Swiss National Bank putting a cap on the value of the Swiss Franc or the Bank of China controlling the exchange rate of the Yuan vs. the US dollar. To set a price, the Bank of Japan would have to be willing to buy every single bond offered at that price. It could pick any price it wanted, but the lower the interest rate, the more bonds it would have to buy. At a low enough price, it would have to buy every security. Damn the Consequences The problem with controlling interest rate turbulence (or any other factor) is the consequences. If the Bank of Japan does buy every Japanese government bond, it will have no control over things like the value of the Yen, the CPI, various asset bubbles that may form, or in the extreme case - Japanese hyperinflation. Practical Ridiculousness If you reflect on what's theoretically possible for more than a second, you will see the practical ridiculousness of the Bank of Japan's statement on curbing turbulence. And what applies to Japan applies even more so the Fed's dual mandate of "low inflation and job growth". Simply put, it is impossible for a central bank to control more than one variable at a time, and the consequences of controlling even a single variable are rather extreme when the market refuses to play along. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

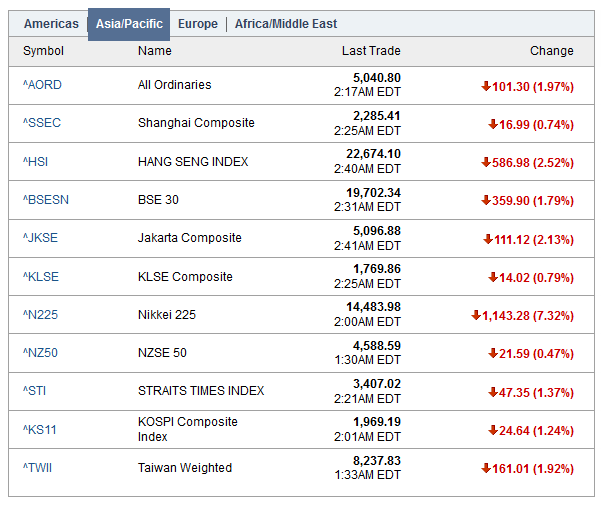

| Nikkei Plunges 1,143 Points (7.32%); Global Equities Hammered; Start of Reflation Bubble Bust? Posted: 22 May 2013 11:49 PM PDT The Nikkei plunged a whopping 1,143 points as the following chart shows.  Global Equities Hammered It's not just the Nikkei that's being hammered. Asia-Pacific is in a rout as well.  click on chart for sharper image Start of Reflation Bubble Bust? Is this the start of the great reflation unwind? I don't know, but we should all hope so. The bigger the bubble the bigger the crash, and this Fed (central bank in general) sponsored equity and corporate bond bubble is enormous. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| You are subscribed to email updates from Mish's Global Economic Trend Analysis To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment