| Australia Manufacturing Collapses as Commodity Supercycle Stalls; Labor and Unions Wrecked Australia Posted: 02 May 2013 02:26 PM PDT Australia fundamentals deteriorate rapidly as evidenced by a collapse in the PMI Manufacturing Index in April. Key Findings

- Manufacturing activity contracted significantly in April as conditions weakened amid a strong Australian dollar, intense import competition, high energy costs and weak local confidence.

- The Australian Industry Group Australian Performance of Manufacturing Index (Australian PMI®) fell 7.7 points to 36.7 on a seasonally adjusted basis. (Readings below 50 indicate a contraction in activity with the distance from 50 indicative of the strength of the decrease.)

- This is the lowest level the Australian PMI® has recorded since May 2009, with many of the key sub-indexes also dropping to levels not seen since 2009. The three-month moving average in April fell to 42.2 points from 43.4 points in March.

- Contractions in activity were recorded in seven out of the eight manufacturing sub-sectors. Significant contractions were recorded in food, beverage & tobacco products; printing & recorded media; non-metallic mineral products; metal products; and machinery & equipment.

- Sharp declines in production, new orders and employment were recorded in April, while finished stocks and deliveries declined as well, albeit at a more moderate pace.

- Capacity utilization in the manufacturing sector fell 2.4 points to 68.6 (the lowest level since June 2009), consistent with the overall drop in activity in the sector.

- Exports continued to contract for the ninth consecutive month, as the exports sub-index fell to 24.5 in April. This was the lowest reading in the history of this sub-index (commencing in 2004).

- Significant contractions in manufacturing activity were recorded across most States, especially in Victoria where the record of activity fell 8.4 points to 29.1 in April, the lowest level on record.

New Orders

The new orders sub-index decreased by 7.0 points to 32.4 points in April (seasonally adjusted). This was the lowest level recorded for this sub-index since May 2009.

Employment

The seasonally adjusted employment sub-index decreased by 9.4 points to 39.3 in April, the lowest level since May 2009.

Inventories

Manufacturing inventories contracted again in April, with the sub-index falling 4.8 points to 46.4 (seasonally adjusted). The deliveries sub-index declined 7.3 points to 41.1, indicating that deliveries have been contracting since March 2012. Australia PMI at a Glance | Series Data | Apr Index | Mar Index | Percentage Point Change | Direction | Rate of Change | Trend (Months) |

|---|

| PMI™ | 44.4 | 36.7 | -7.7 | Contracting | Faster | 22 | | Production | 41.7 | 33.1 | -8.6 | Contracting | Faster | 13 | | Employment | 48.7 | 39.3 | -9.4 | Contracting | Faster | 18 | | New Orders | 39.4 | 32.4 | -7.0 | Contracting | Faster | 8 | | Inventories | 51.2 | 46.4 | -4.8 | Contracting | From Expanding | 1 | | Supplier Deliveries | 48.4 | 41.1 | -7.3 | Contracting | Faster | 14 | | Input Prices | 65.5 | 57.0 | -8.5 | Expanding | Slower | 131 | | Exports | 27.4 | 24.5 | -2.9 | Contracting | Faster | 9 | | Selling Prices | 43.0 | 40.3 | -2.7 | Contracting | Faster | 25 | | Average Wages | 57.7 | 57.0 | -0.7 | Expanding | Slower | 48 | | Capacity Utilization | 71.0 | 68.6 | -2.4 | Decrease |

|

| Macro Alert From Steen Jakobsen Via email, Steen Jakobsen at Saxo Bank sent these comments ... Macro Alert: Australia is seeing significant slow-down.

- Australia's benefit from the Super Cycle in commodities is petering out in 2013. Mining investment to GDP will peak at 8%. This concept is supported by the RBA.

- There are significant reductions in pipeline projects due to lower general level of commodity prices and cancellations.

- The non-mining economy is weaker and getting weaker

- China slow-down hits Australia

Massive Imbalances Please note the massive imbalances in the PMI report. Input prices have been expanding for 131 straight months. Wages have been expanding for 48 months. Selling prices have been contracting for 25 months. New orders and exports tell the story. Wages are too high. Margin pressures mount. Employment must drop and it did. The employment index was down a monstrous 9.4 points. Labor and Unions Wrecked Australia The labor party and unions wrecked Australia. This was invisible for years because a housing boom and China-fueled commodity boom masked the untenable nature of wage and property bubble growth. Now, it's payback time. On September 14, prime minister Julia Gillard, leader of the Australian Labor Party will be thrown out of office in a landslide. Unfortunately, it will take years for Australia to recover from the damage caused by Labor. Addendum - Comments from Steve Keen Steve Keen blames both parties. Via email, Keen says " The damage began under Labor with Hawke and Keating, was turbocharged by the Liberals under Howard, and simply maintained by Rudd/Gillard Labor. And unions have lost significant power all the way through--they've been bystanders, not active participants. It's instead been a series of distortions caused by a neoliberal philosophy that is shared by both parties." Hmm. Parties talk differently but act the same. Where have we seen that before? In the US, it's on war, bailouts, and spending that always goes up. Romneycare and Obamacare were the same. For political purposes people pretend differences exist when they don't, except on some social issues. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

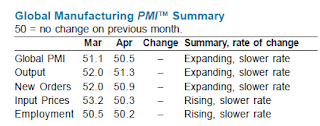

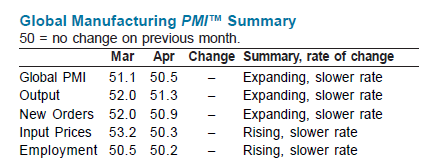

| Global Manufacturing Stagnates; Global Recession Will Follow Posted: 02 May 2013 10:49 AM PDT The JPMorgan Global Manufacturing PMI shows Global manufacturing growth slows to near-stagnation. At 50.5 in April, the JPMorgan Global Manufacturing PMI™ – a composite index* produced by JPMorgan and Markit in association with ISM and IFPSM – signalled expansion for the fourth straight month. The rate of expansion decelerated slightly during April, meaning that growth so far in 2013 has remained, at best, only marginal.

Japan, South Korea, Indonesia and Vietnam were the only nations to report a faster rate of improvement in operating conditions during April. Europe remained the main drag on the global aggregate, with the euro area contracting at the sharpest pace in the year-to-date and the UK stagnating.

The US PMI fell sharply to signal the slowest growth for six months. There was further stagnation in neighbouring Canada, while Mexico expanded at the weakest pace in 20 months in Mexico. Growth of manufacturing also slowed to near-stagnation in China, Russia, India and Brazil. Global PMI April vs. March  Every facet of global manufacturing is slowing and global growth will follow. A global recession is certainly baked in the cake, if indeed a recession is not already in progress. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

| Shock and Awe: ECB Prepared to "Cope With Consequences of Negative Deposit Rates"; Dancing in the Dark Experiment Posted: 02 May 2013 09:09 AM PDT As expected the ECB, cut its lending rate 25 basis points to 0.50%. Yesterday, I suggested the ECB may try a " shock and awe" move. They did, just not the move anyone expected. Instead, Mario Draghi said the ECB was Prepared to " Cope With Consequences of Negative Deposit Rates". Shock and Awe Bloomberg reports Euro Falls as Draghi Open to Negative Rates; Dollar Strengthens The euro fell for the first time in five days against the dollar after European Central Bank President Mario Draghi said policy makers may take the unprecedented step of charging banks to hold excess reserves.

"The euro was quite upbeat until Draghi made his comment that the ECB would be able to cope with any consequences of negative deposit rates," said Daragh Maher, a currency strategist at HSBC Holdings Plc in London. "Previously, the language of the ECB on this front has characterized it as uncharted waters. Today, it seems the ECB is more open to the idea. The euro was clearly spooked by the mere concept of negative deposit rates in the euro zone." For an analysis of what this means, with a tip of the hat to Steen Jakobsen at Saxo Bank for the link, let's flashback to a decision to cut the deposit rate to zero in July of 2012. Dancing in the Dark Experiment The Financial Times says ECB Dances in the Dark It's clear the ECB has gone into experimental mode.

A positive deposit rate was the last thing anchoring money market rates to zero — or vague profitability. This is because banks could arbitrage the difference between the rates they received at the ECB and the rates money market funds were able to invest at.

By cutting the deposit rate, the ECB is killing this arbitrage. There will not be any profit associated with taking money from non-banks and parking it at the ECB for a small profit. Non-banks won't even be able to get zero.

This will leave real-rates exposed to further deterioration.

The ECB, of course, is hoping that non-banks will choose to channel that money into risky assets instead. Death of Banking FT Alphaville makes the case Negative rates as a precursor to the death of banking. What we believe is that rather than stimulating the lending market — and the economy along with it — such a rate policy could have a disastrous impact on collateral markets and money market funds, not to mention the net interest income of lending institutions. All of which could unleash a protracted deflationary spiral.

The move could also presage the death of banks and lending institutions completely. FT Alphaville cites Morgan Stanley Research as follows: Our rates team expects short end German yields to follow financing rates into negative territory and some investors to extend along duration and credit curves to achieve positive yields to maturity.

But we do not think negative ECB deposit rates would drive any increase in cross-border interbank lending. Rather, we see a risk of greater Balkanisation of European banking markets from funding pressures.

Today, a fall in rates would hit NII and reduce banks confidence in their earnings build and capital plan – making them wish to delever more not less, although time should heal. Market liquidity is likely to fall; Bank and insurers earnings under further pressure.

In Japan, JGB trading volumes fell by 2/3 over the coming 12 years as ZIRP was adopted, particularly at the short end – one reason why the Japan Central Bank does not want front end rates to be negative. Negative rates would likely be a negative for earnings and could thus impact solvency of banks and insurers.

The greatest risk our rates colleagues see would be for negative rates 2-3 years down the curve, in which case banks would need to re-price credit further.

Morgan Stanley European Insurance analyst Jon Hocking writes: "Earnings and solvency margins for European insurers are already under severe pressure from very low long-term bond yields." Deposit Rate of Zero Did Not Work It's clear that cutting the deposit rate to zero did not work. So why will cutting them to less than zero work? A negative deposit rate will not stimulate lending because it does not fix any structural problems, it does not fix any liquidity issues, and it makes solvency problems worse by turning guaranteed arbitrage gains into guaranteed losses on excess reserves. Should this actually succeed in stimulating lending, expect it to also succeed at stimulating losses on that lending. Mike "Mish" Shedlock http://globaleconomicanalysis.blogspot.com |

No comments:

Post a Comment